Key takeaways

Median house prices could soar by up to $154k by end of 2026 as buyers pile in for spring

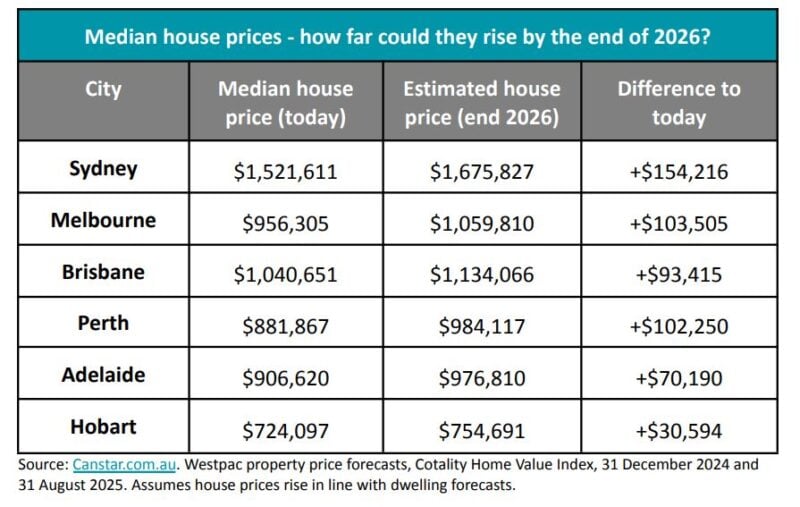

Westpac forecasts suggest Sydney’s median house price could rise by up to $154,000 by the end of 2026, taking it close to $1.68 million.

Melbourne is expected to stage a strong recovery, with forecasts of 10% growth in 2026, pushing the median above $1.05 million.

Of course, these numbers are based on assumptions that could change with economic conditions, RBA policy shifts, or global pressures.

Smart investors should focus on investment-grade properties in high-demand locations, not on chasing short-term forecasts.

Median house prices could soar by up to $154,000 by the end of 2026 as buyers pile in over the next year at a time of limited supply.

Sydney’s median house price could jump by more than $150,000 over the next 15 months.

Melbourne's median house price may climb past the $1 million mark.

Perth, Brisbane, and Adelaide are also tipped to see six-figure gains in house values.

That’s according to Canstar’s analysis of Westpac’s latest property price forecasts.

If these projections hold true, the conversation about housing affordability is about to get even tougher.

Of course, it's not only Westpac that's forecasting a number of strong years of property price growth. All major research houses and banks are forecasting similar levels of growth.

What the forecasts are saying

Westpac expects Sydney house prices to rise 5% this year and another 8% in 2026, which would lift the median to nearly $1.68 million, an extra $154,000 compared to today.

Melbourne, after a few quieter years, is forecast to stage a comeback with a hefty 10% jump next year, pushing its median above $1.05 million.

For first-home buyers, that’s yet another psychological hurdle.

Brisbane, Perth, and Adelaide are also tipped to see gains between $70,000 and $100,000, while Hobart looks set for a more modest $30,000 rise.

A tale of two realities

As Sally Tindall, Canstar’s data insights director, put it:

“Sydney’s median house price could rise by up to $154,000 by the end of next year if house prices rise in line with Westpac’s dwelling price forecast.

For those already in the market, that’s welcome news for their equity.

- Also read:National Weekly Auction Report – April 11th 2026 | Auction Markets Steady After Easter with School Holiday Listings

- Also read:Latest Property Asking Prices State by State | National Listings Rise in March

- Also read:Rents Surge Again as Interest Rates Bite – What Happens Next?| | Property Insiders

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

For those still saving, the deposit hurdle is likely to get a whole lot steeper, not to mention the difficulty in clearing a bank’s serviceability test”

This is the classic divide in our property market.

If you already own a home, your wealth compounds.

But if you’re still saving, it feels like the finish line is moving further away just as you’re about to cross it.

And while falling interest rates might give buyers a little more borrowing power, there’s a risk those gains get swallowed up by higher prices.

Final note

I’m not surprised by these forecasts.

With population growth strong, rental markets tight, and construction costs elevated, the supply-demand imbalance remains ,which naturally fuels higher property prices.

Add to that the 70,000 new first-home buyers that have been forecast to enter the market over the next 12 months with the introduction of the new first-home buyer incentives, and that will only add fuel to the flames of our housing markets.

But forecasts are not strategies.

Successful investors look beyond next year’s numbers and focus on the long term fundamentals; buying well-located, investment-grade properties that deliver long-term growth.

That’s how you build lasting wealth.

Not by chasing forecasts, but by sticking to proven principles, ignoring short-term noise, and playing the long game.