Key takeaways

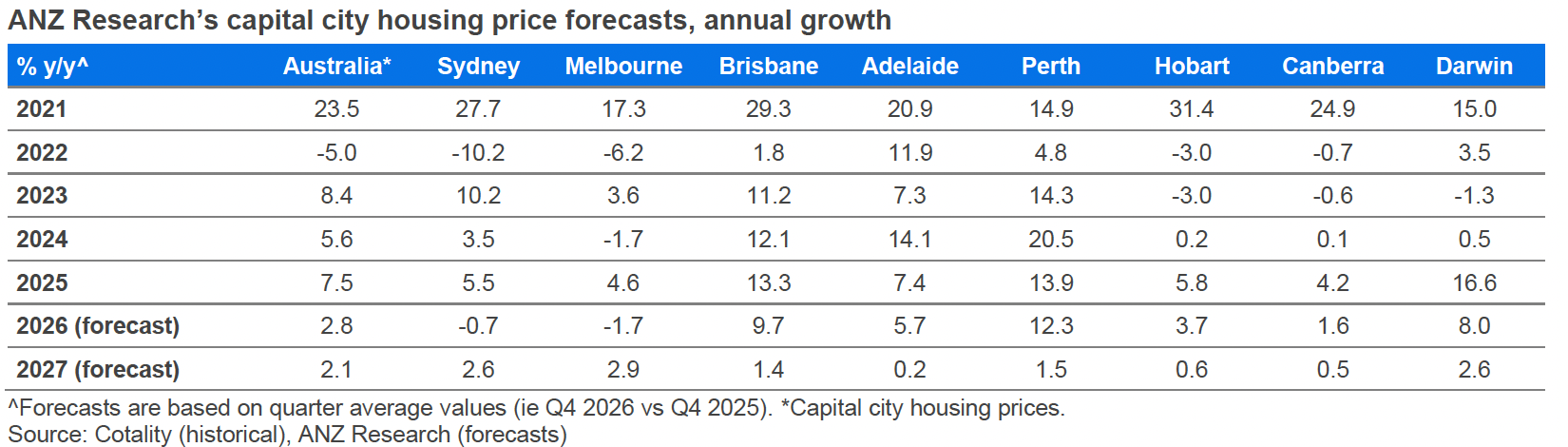

ANZ Research forecasts Sydney house prices to fall 0.7% in 2026, with a recovery to 2.6% growth pencilled in for 2027, though Domain's separate FY27 forecast takes a more cautious view.

Sydney's lower quartile values have been rising while the upper quartile has fallen for five consecutive months, a genuine two-speed pattern within the city that's worth understanding before drawing any broad conclusions.

The structural case for Sydney remains intact. Chronic undersupply, a rental vacancy rate of 1.7%, and a population growing by more than 100,000 residents a year haven't gone anywhere, even while short-term sentiment has cooled.

The RBA lifted the cash rate to 4.35% in May, completing three hikes for the year, then held steady in June, and most economists don't expect the first cut until around the middle of 2027.

Affordability constraints are shaping buyer behaviour more than they're destroying demand, which is why well-located, mid-market properties are currently holding their ground better than premium stock.

Investment-grade properties in inner and middle-ring suburbs with strong owner-occupier appeal continue to hold up better than the broader market and remain the focus for strategic investors.

Thinking of investing in Sydney property?

You're not alone, but that doesn't mean it's straightforward right now.

"Sydney's too expensive," "you've missed the boat," "now's not the time to invest," these are the lines doing the rounds at dinner tables and on social media, and none of them tell you much about what's actually happening on the ground.

Here's the more useful truth... every market cycle throws up opportunities if you know where to look, and Sydney remains one of the most resilient property markets in the world, even through a softer patch like the one it's in now.

Sydney's property market has cooled through 2026, following the RBA's decision to lift rates three times this year in response to re-accelerating inflation and global uncertainty.

That's taken real heat out of buyer sentiment, with ANZ forecasting a modest 0.7% fall for Sydney across the year.

There's no single Sydney property market though, and some segments are clearly holding up better than others.

If you've watched this market for more than one cycle, you'll recognise the pattern of what tends to follow a period of softness in a structurally undersupplied city, even if the timing of any turn is genuinely uncertain this time around.

ANZ's own forecast has Sydney bouncing back to 2.6% growth in 2027, while Brisbane and Perth are expected to slow after several strong years.

Domain's separately released FY27 forecast takes a considerably more cautious view of the same period, which I'll walk you through properly in the next section.

Note: By the way, if you think Sydney already feels full, it's going to get more crowded over the next decade.

NSW is forecast to add close to a million more people by 2034, with more than 650,000 of them living in Sydney, and that will only add to the pressure on an already undersupplied market.

Here is the latest data on the median property prices for Sydney.

| Property | Median price | Δ MoM | Δ QoQ | Δ Annual |

|---|---|---|---|---|

| All Capital city dwellings | $1,244,617 | -1.4% | -4.0% | -2.0% |

| Capital city houses | $1,529,308 | -1.7% | -4.6% | -2.5% |

| Capital city units | $889,617 | -0.8% | -2.5% | -0.6% |

| Regional dwellings | $836,911 | -0.4% | -0.9% | 6.8% |

Source: Cotality, 1st August 2026

Sydney median price has risen a substantial 27.7% since the onset of Covid, and that longer-term gain is real, but the more recent trend has turned negative.

Of course, there's no single Sydney housing market, and some areas are performing very differently to others right now.

It's a bit like having one hand in a bucket of hot water and the other in a bucket of cold water and saying that on average you're feeling comfortable.

Here's the forecast for Sydney property prices for the rest of 2026 and 2027

The 2026 forecasts circulating early this year have since been revised by all research houses.

ANZ Research's most recent update has Sydney house prices falling 0.7% across 2026, reflecting higher interest rates and a sharp drop in consumer confidence following the escalation of geopolitical tensions earlier in the year.

The RBA delivered that third rate hike in May, taking the cash rate to 4.35% and fully reversing the cuts made through 2025, before holding steady at its June meeting.

Sydney and Melbourne are the only two capital cities forecast to improve year-on-year growth in 2027.

The expansion of the first homebuyer support will add further fuel to the lower end of the Sydney housing market.

As part of his election promise, Prime Minister Anthony Albanese has allowed virtually all first home buyers to enter the market with just a 5 per cent deposit, via a taxpayer-backed guarantee.

In New South Wales, first-home buyers can use this scheme to buy a property valued at up to $1.5 million. In other words, not just cheap houses in the outer suburbs, but median-priced properties.

As these new buyers enter the market over the next year or two, it will only add further fuel to the flames of an undersupplied housing market, ensuring a government backed property surge.

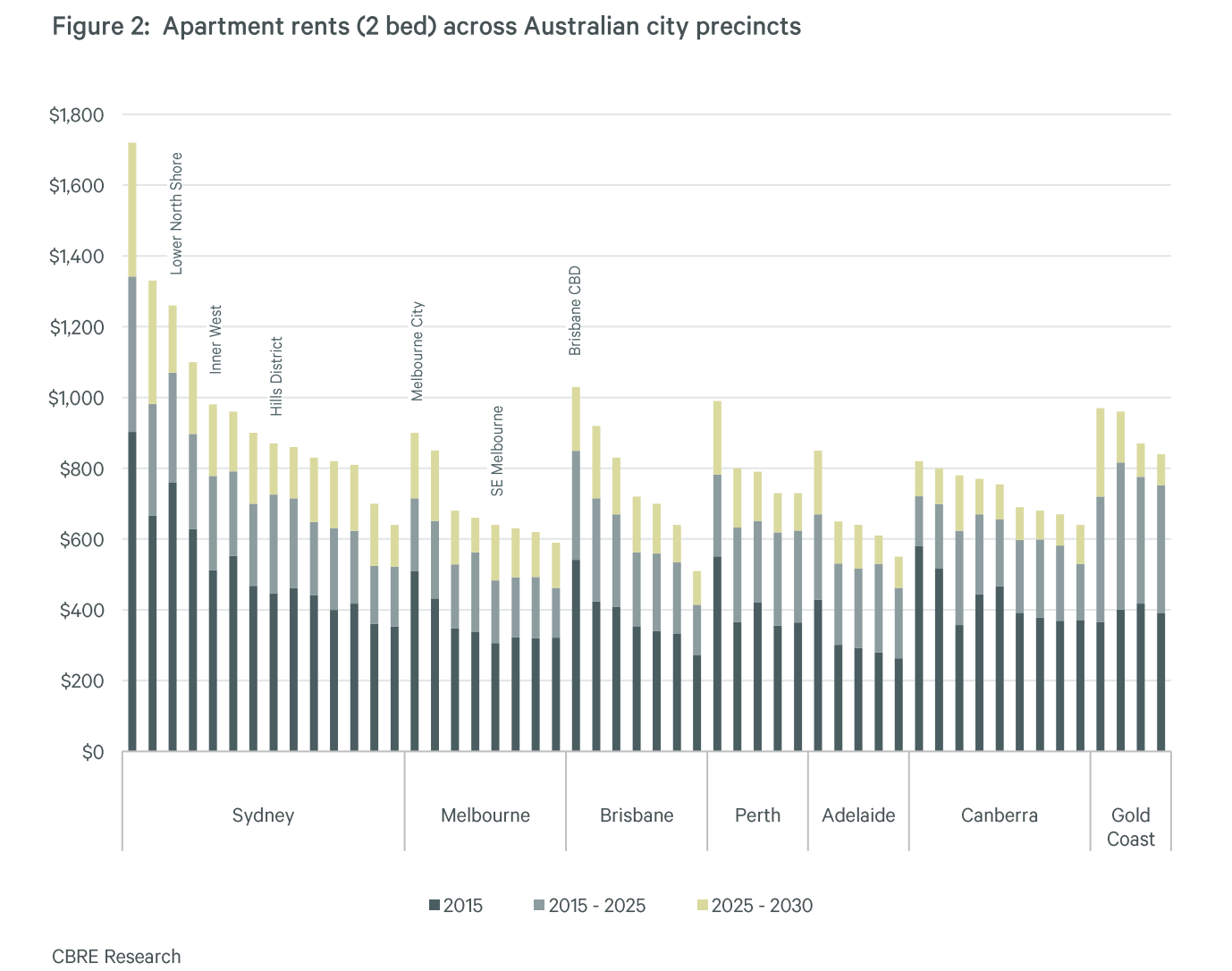

Sydney rents set to surge

Median apartment rents are likely to grow by 24% between 2025 and 2030 across Australian capital cities, according to the latest report by International Property Consultancy, CBRE.

CBRE estimates apartment delivery in Sydney will average 11,700 p.a. over 2025-30, well below 30,000 p.a. demand for total housing stock and this means vacancy rates are set to fall from 2.0% to 1.2% and rents will rise by 24% .

You can always beat the averages.

While it’s likely that Sydney property price growth will be sluggish for a while, the good news is that you can always beat it by investing in the right property in the right location.

Now by that, I don’t mean look for the next hotspot. I mean buying quality properties in locations that will outperform in the long term such as gentrifying suburbs.

You see...property offers countless opportunities to improve your results through your own time, skills and knowledge – so you don’t need to settle for average.

And there’s more to it than just location. You can add value through refurbishment or redevelopment.

Good. I have enough context. Importantly, the Sydney picture is actually different from Melbourne's - the current data shows it's Sydney's more affordable segments outperforming the blue-chip end right now, not the other way around. I'll write this honestly and in a way that still serves your investment philosophy. The section mirrors the Melbourne one structurally but reflects the Sydney reality accurately.

Some parts of Sydney are holding up better than others

The Sydney median tells you very little about what's actually happening inside the market, and that's worth understanding before you draw any conclusions about where to invest.

Cotality data shows Sydney's lower quartile values rising while the upper quartile has declined for five consecutive months.

In a city where affordability constraints are acute and borrowing capacity has been squeezed by higher rates, that's not entirely surprising. When buyers can borrow less, they concentrate their competition at lower price points, and that's where the momentum sits right now.

But I wouldn't read too much into that short-term dynamic if you're thinking about the next decade.

The enduring case for Sydney's inner suburbs, eastern beaches, lower north shore, and established family corridors hasn't changed.

These locations have a permanent scarcity of land, a concentration of high-income households whose purchasing power is far less sensitive to rate movements, and a lifestyle appeal that simply can't be replicated further out.

Premium suburbs like Mosman, Randwick, Cremorne, and Balmain consistently attract buyers who are motivated by where they want to live, not just what they can borrow this month.

The agents working these markets are reporting that well-presented, move-in ready homes in tightly held streets are still attracting genuine competition, while properties that need work or are in less desirable positions are sitting longer and selling at a discount.

This bifurcation within the market is actually useful information for investors. It tells you that quality is still being rewarded, scarcity is still doing its job, and the softness is concentrated in the segments most exposed to rate sensitivity and discretionary demand.

For those with a five to ten year horizon, the current period of flat-to-soft conditions in Sydney's premium suburbs represents the kind of entry point that looks obvious in hindsight and uncomfortable in the moment.

Won't rising interest rates stall the Sydney property market?

It's old news that the RBA lifted interest rates at its February and March meetings.

The reality is that interest rates will remain higher for longer than most investors would like, and that has consequences for the housing market.

ANZ now expects another hike in May 2026, bringing the cash rate to 4.35% and fully reversing the gains of last year's cutting cycle.

Consumer confidence, as measured by the ANZ-Roy Morgan index, is now near a record low - its weakest reading in more than 50 years.

Sydney tends to be more sensitive to rate movements than other capitals, which is why it is feeling this more sharply than Brisbane or Perth right now.

But that same rate sensitivity cuts both ways - when the RBA eventually pivots back to cutting, Sydney historically leads the recovery. The ANZ 2027 forecast of 2.6% growth is a reflection of exactly that dynamic.

And here’s the key point many commentators miss...

Look back to the middle of last year, when interest rates were around these levels. Property markets performed remarkably well.

Because fundamentals still matter more than sentiment.

We have strong population growth, high employment, and a chronic shortage of new housing construction.

Add to that first home buyer schemes that are allowing tens of thousands of buyers to enter the market with just a 5% deposit, and you can see why demand hasn’t collapsed.

Note: The latest cash rate hikes are likely to act as a speed bump rather than a full-blown brake on house prices, with some pockets barely tapping the brakes at all.

Now, let’s talk numbers.

The average new mortgage is close to $700,000. A full pass-through of each 0.25% rate rise adds roughly $110 a month to repayments on a typical 30-year loan.

At the same time, borrowing capacity does take a hit. A median-income household will lose around $18,000 from its maximum borrowing power.

And that has flow-on effects. It pushes more buyers away from mid-tier homes and towards lower-priced properties – apartments, townhouses, villa units, and houses further from city centres.

Meanwhile, construction costs, labour shortages, and developer feasibility issues are still choking off new supply. And interest rates don’t fix that problem.

With listings well below long-term averages, and supply-demand pressures firmly in place, a single rate hike is unlikely to materially change the overall market balance.

What it does create is uncertainty. And uncertainty temporarily sidelines some buyers.

That’s why I see this period as a genuine opportunity for those who are prepared.

If you’re finance-ready, fewer competitors can mean better negotiations, better selection, and better long-term outcomes.

Tip: As Warren Buffett famously said: be fearful when others are greedy, and greedy when others are fearful.

Why Sydney Still Offers Stellar Investor Value (Even at a $1.5M Median)

You might be wondering whether there's still genuine investment value at current Sydney prices, given everything we've just covered about the softer conditions this year.

Here's why I still believe there is, provided you're realistic about the near-term path rather than expecting an immediate turnaround.

- Rent pressures and tight vacancy mean genuine yield support.

Despite the softer purchase price environment, Sydney's rental market remains rock-solid, with vacancy rates still sitting well below what's needed for a balanced market. That tight rental environment continues to boost cash flow and helps offset the higher entry prices that come with buying in Sydney. - The two-speed market creates selective upside. There's no single Sydney property market; it's genuinely fragmented. A-grade family homes in lifestyle-rich suburbs across the inner west, eastern suburbs and Northern Beaches continue to draw real competition, while oversupplied high-density precincts in parts of Parramatta, Homebush and Zetland are best avoided.

- Boutique, lifestyle-oriented apartments are trading under replacement cost. Well-located, small-scale apartments with genuine character and family appeal are currently priced below what it would cost to build them today, and backed by strong lifestyle demand; that combination tends to deliver resilience over time.

- Outer-west growth corridors still offer real upside. Affordable suburbs in Western Sydney, including St Marys, Fairfield and Liverpool, continue to see solid growth on the back of infrastructure investment, particularly the Western Sydney Airport, and consistent owner-occupier demand.

- The 2027 picture is genuinely mixed, and worth understanding properly. ANZ Research's April 2026 forecast has Sydney falling 0.7% in 2026 before recovering to 2.6% growth in 2027. For investors with a genuine five to ten year horizon, the entry conditions this softer period creates matter more than which of the many forecasts proves right.

- Investor equity provides a real buffer. Many Sydney property owners, particularly those who've held for several years, carry substantial equity that cushions them through a softer patch like this one. That equity position means many are in no rush to sell, which helps explain why listings remain constrained even during a period of weaker buyer demand.

Sydney’s population engine will keep driving property values

When you think about what really underpins property values in Sydney, it always comes back to one thing – people.

Every extra person needs a place to live, and when you put a growing population into a market where supply is already constrained, you create an environment where property values are naturally supported.

That’s exactly what’s playing out in Sydney right now.

Where we are today

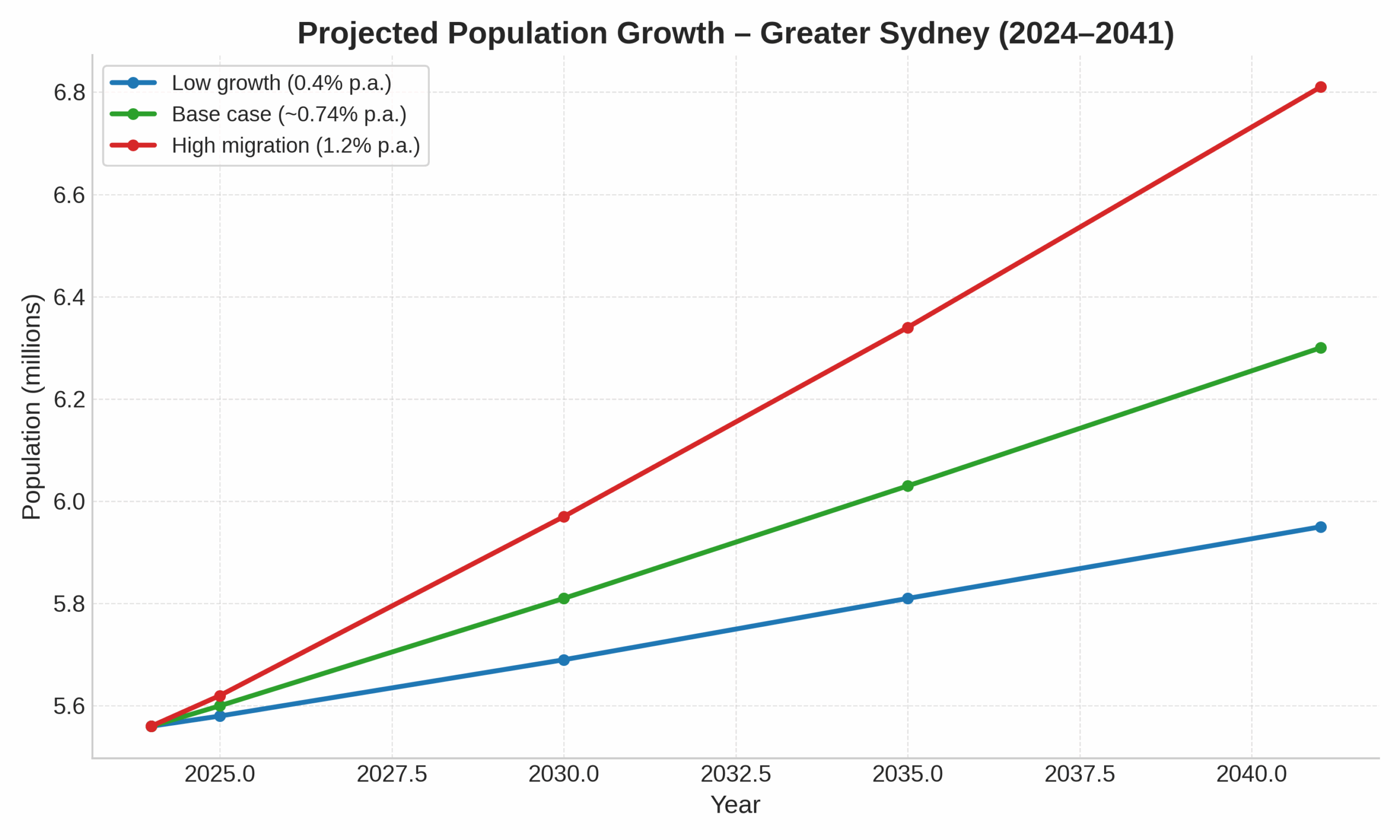

Sydney’s population has just hit 5.56 million people as at June 2024, after growing by around 107,500 residents in a single year. That’s roughly 2 percent annual growth, which is massive for a mature city of this scale.

Importantly, most of that increase is being driven by overseas migration – in fact, net overseas migration added over 120,000 people to Sydney in the past year alone.

Even though Sydney continues to lose people to interstate migration (with about 41,000 more leaving than arriving from other parts of Australia), the overseas inflows more than offset this. Sydney remains Australia’s global city and continues to attract students, skilled migrants, and professionals from around the world.

The city’s demographic profile is also skewed younger than the rest of NSW, with nearly 40 percent of residents aged 20–44. This means a larger share of working-age households, creating sustained rental and buying demand across the property spectrum.

Looking ahead – the next decade and beyond

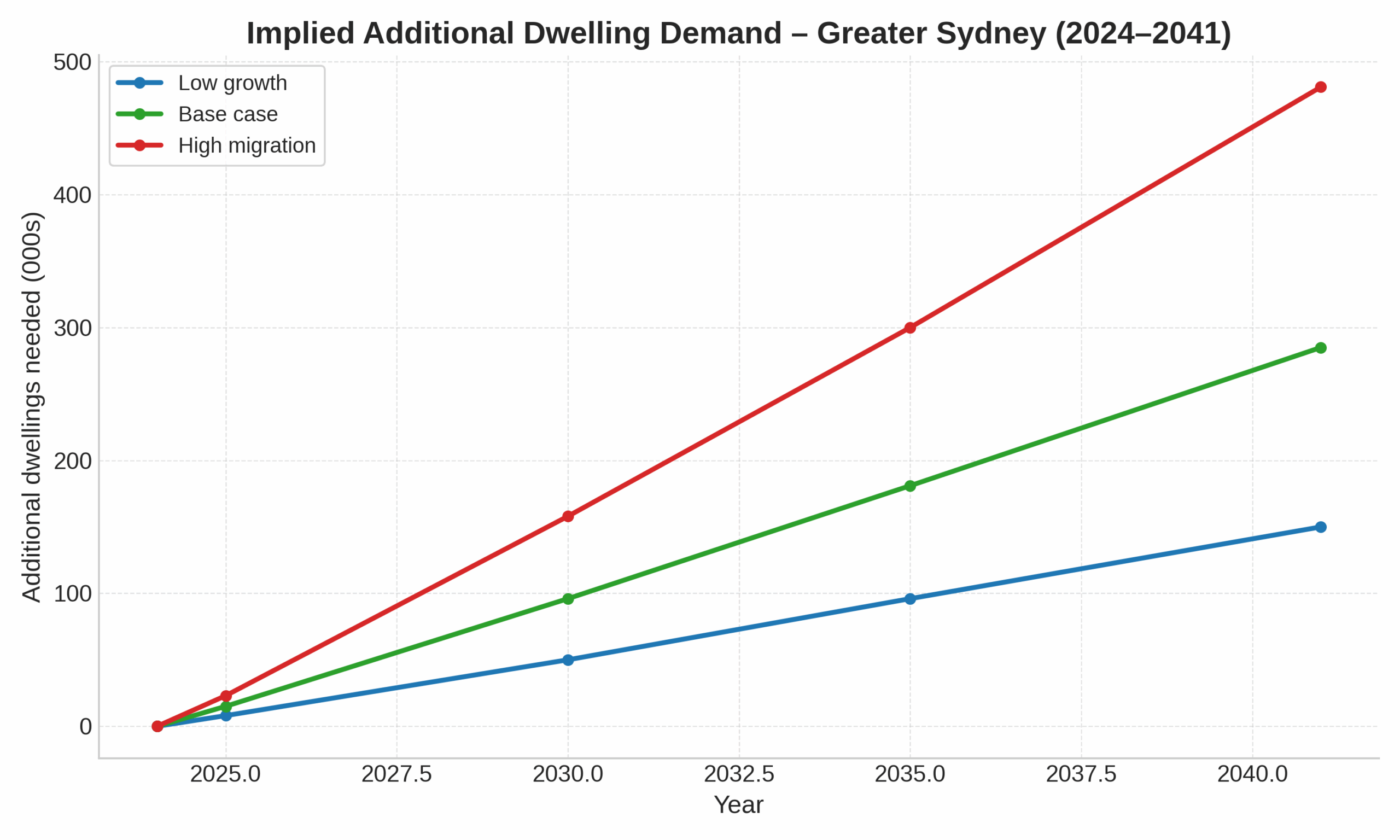

Official NSW planning projections show Greater Sydney heading to around 6.3 million people by 2041 – an increase of roughly 750,000 residents from today’s base.

Even under conservative assumptions, that equates to tens of thousands of extra people moving into Sydney each year.

If you run the numbers, that kind of growth translates into a need for around 180,000–190,000 additional homes in the next decade alone.

And if migration remains elevated, the figure could easily blow out to over 300,000 dwellings needed by 2035.

Put simply, even the most cautious population outlook means Sydney must find room for hundreds of thousands of new households.

And here’s something many people forget: the average household size has been trending down nationally, slipping from around 2.9 people living in each household to around 2.5.

That means we need more dwellings for the same number of people, which quietly amplifies housing demand even if population growth slows.

Why this matters for property values

When you have strong, compounding demand and sluggish supply, you don’t need to be an economist to see the result – tighter rental markets and firmer property prices.

Sydney’s constrained geography, long planning timeframes, and infrastructure bottlenecks mean supply simply can’t keep up with the demand implied by these population figures.

That’s why I believe Sydney’s population engine isn’t just a short-term boost – it’s a structural tailwind. As long as people keep arriving, forming households, and competing for limited stock, Sydney property values will remain underpinned by a demographic demand base that’s hard to shake.

Sydney property market update

At Metropole Sydney we’re finding that strategic investors and homebuyers are still actively looking to upgrade, picking the eyes out of the market.

While the high end of the Sydney property market led this new phase of the property cycle in 2023, more recently, cheaper properties are recording stronger price growth.

Buyer sentiment has softened since the RBA's rate hikes, and confidence is likely to remain cautious as another hike appears likely in May.

That said, the Sydney market hasn't collapsed - what we're seeing is a recalibration, not a rout.

At Metropole Sydney we're finding that strategic investors and homebuyers are still actively looking to upgrade, picking the eyes out of the market.

While the high end of the Sydney property market led the previous phase of the cycle, more recently it's been the more affordable segments that have recorded stronger relative performance, consistent with the lower-quartile trend we discussed earlier.

Buyer sentiment softened through the RBA's three rate rises this year, and confidence is likely to remain cautious for a while yet, with most economists now expecting rates to stay on hold until around the middle of 2027 rather than move again in the near term.

That said, the Sydney market hasn't collapsed; what we're seeing is a recalibration rather than a rout.

At Metropole Sydney, well-prepared buyers are finding better conditions than at any point in the past couple of years, with less competition and more willingness from vendors to negotiate.

The best-performing residential investment properties in Sydney for 2026 - 27

It's likely that certain types of properties will outperform others in Sydney in 2026 fuelled by demographic shifts, evolving lifestyle preferences, and economic factors.

Family Homes in Premium Suburbs

The ongoing preference for space, especially among families, means demand for quality houses in established, affluent suburbs will remain high.

While Sydney's median house prices are steep, well-positioned family homes in prestigious areas continue to offer solid long-term capital growth.

Investors should look for 3-4 bedroom houses on sizable blocks in well-established neighbourhoods with access to good schools, amenities, transport links, and green spaces.

Eastern suburbs like Randwick, Coogee, and Maroubr continue to be sought after by families due to their proximity to the CBD, beaches, quality schools, and lifestyle amenities. They offer strong long-term growth and steady rental demand.

In the Lower North Shore investors should consider Willoughby, Lane Cove, and Artarmon. These family-friendly suburbs with excellent schools, green spaces, and easy access to the city are perennial favourites among renters and home buyers alike.

On Sydney’s Northern Beaches the suburbs of Dee Why, Mona Vale, and Freshwater attract families looking for a relaxed lifestyle close to the beach, good schools, and outdoor activities. They offer strong growth potential as more people prioritise lifestyle and work-from-home options.

Townhouses in Middle-Ring Suburbs

Townhouses represent an increasingly popular choice for both investors and owner-occupiers due to their affordability relative to standalone houses and the lifestyle advantages they offer.

With Sydney's shift towards medium-density living, townhouses are expected to remain in demand, especially in middle-ring suburbs experiencing gentrification.

Investors should target 3-4 bedroom modern townhouses in low-density developments with a focus on functional living spaces, private courtyards, and proximity to amenities.

Sydney’s Inner West offers excellent opportunities for townhouse investments. The suburbs of Marrickville, Dulwich Hill, and Petersham offer a vibrant culture, proximity to the CBD, and ongoing gentrification.

These suburbs are popular with young professionals and families looking for a balance between urban living and suburban space.

In the St George area Hurstville, Kogarah, and Carlton have been experiencing significant growth due to infrastructure upgrades and its proximity to Sydney’s CBD and airport. The demand for townhouses in these suburbs is strong, particularly among families and professionals.

Sydney’s North-West growth corridor has become an attractive location for townhouse investments. Rouse Hill, Kellyville, and Castle Hill are areas worth considering, with expanding infrastructure, shopping centres, and schools, these suburbs offer a blend of affordability, accessibility, and lifestyle.

Boutique Apartments in Lifestyle Hubs

I would avoid high-density apartment developments, but boutique “family friendly” apartments in lifestyle hubs have proven resilient over the last few years and are likely to to continue to outperform in the future as currently investors can buy established apartments considerably below replacement cost.

The key is to target smaller, low-rise complexes in vibrant areas where demand from young professionals, students, and downsizers remains high.

Look for spacious, high-quality 1-2 bedroom apartments with balconies, modern finishes, and access to cafes, restaurants, and public transport.

Boutique apartments in Sydney’s eastern suburbs of Bondi, Bronte, and Coogee always attract high demand due to their proximity to the beach, CBD, and a plethora of dining and shopping options.

Quality apartments with ocean views or easy beach access will always outperform.

Investors should also consider apartments in the inner suburbs of Surry Hills, Darlinghurst, and Redfern.

These lifestyle-focused suburbs are popular with young professionals and couples seeking a vibrant, urban lifestyle close to work, dining, and entertainment.

Apartments in well-designed, low-rise developments here continue to offer strong rental yields and capital growth.

What's happening in the Sydney property market?

Sydney buyers are still active, but they're being noticeably more cautious than a year ago, with shallower pockets and meaningfully reduced borrowing capacity following this year's rate rises.

Even so, more investors are re-entering the Sydney market, recognising the current conditions as a genuine window for those thinking several years ahead rather than the next few months.

Sydney auction clearance rates have eased back more than a normal seasonal slowdown would suggest, running below 50% for much of the June quarter, and that's a fair reflection of the softer conditions showing up across the price data.

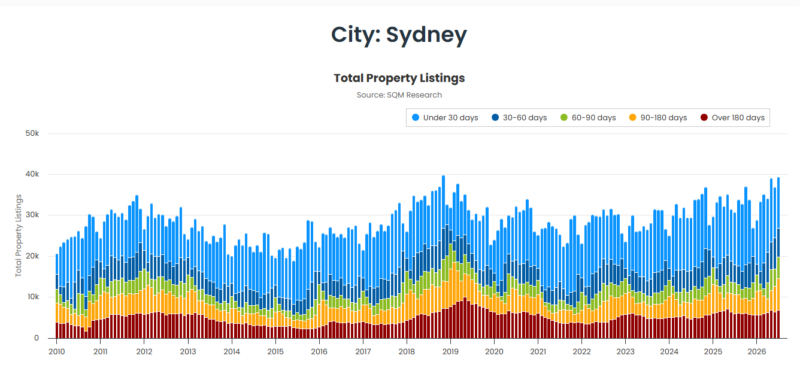

Sellers are gradually returning too, with total property listings running a little above where they sat a year ago, though the stock of genuinely well-presented, tightly held property remains limited, which is keeping overall supply constrained in the segments that matter most.

Source: SQM Research

Sydney's market isn't behaving as one single market right now - there's a clear flight to quality, with A-grade homes and investment-grade properties still attracting genuine competition given limited supply, while B-grade properties are taking longer to sell and informed buyers are steering clear of C-grade stock altogether.

Some of the city's most tightly held suburbs still see remarkably few listings, with homeowners holding on for decades in places where genuine lifestyle appeal outweighs any rate-driven hesitation elsewhere in the market. Lifestyle and coastal suburbs in particular continue to see strong underlying demand from buyers prepared to wait for the right property rather than compromise.

At Metropole Sydney, we're finding strategic investors taking advantage of this window while homebuyers continue looking to upgrade and pick the eyes out of the market.

The overall picture remains fragmented rather than uniformly weak, which is, in a sense, a more normal property market than the one-directional booms and busts we sometimes see.

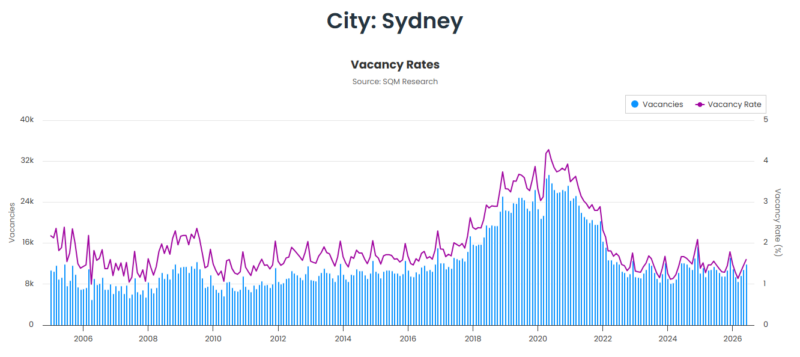

Sydney’s rental markets remain exceptionally tight

Vacancy rates in Sydney’s rental market are traditionally very tight, usually hovering well below the national baseline.

But thanks to soaring demand and severe undersupply in the rental market, the national vacancy rate is exceptionally low today by historical standards.

SQM Research recorded Sydney’s vacancy rate has crept up a little to 1.7%.

By comparison, the vacancy rate which represents a balanced market is around 2.5%.

Source: SQM Research

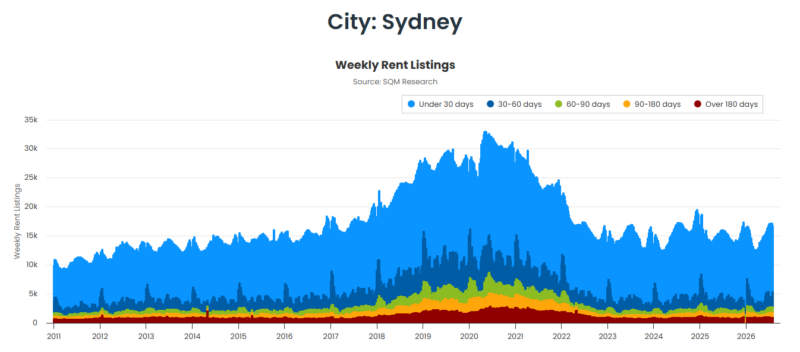

This shows us that, like everywhere else in the country, Sydney’s rental market has plunged into crisis, with record-low vacancy rates, high rent prices, strong demand, and a rising population putting the city’s market into a pressure cooker environment.

And the data for vacancy rates and also weekly rent listings highlights that the distressing state of Sydney’s rental market leads to a bleak outlook for renters.

And at Metropole Property Management our vacancy rate is less than half the industry rate, in part because our clients have chosen investment-grade properties, but we'd like to think it also has a bit to do with our proactive property management policies.

Source: SQM Research

Sydney has been facing a rental housing shortage for several years now.

This has led to increased competition for available homes, driving up rentals and making it increasingly difficult for many Australians to afford a place to live.

One of the aspects of the housing market boom during the pandemic was that it was driven by owner-occupier buyers.

And since Australia’s international borders in early 2022, Sydney has become a major recipient of new residents, both skilled immigrants and overseas students, putting extra pressure on the Sydney property market, particularly the rental markets.

The current metro area population of Sydney in 2024 is 5,185,000, a 1.25% increase from 2023. The metro area population of Sydney in 2023 was 5,121,000, a 1.27% increase from 2022.

If you think Sydney is already full, it's going to get more crowded in the next 10 years.

NSW will have nearly 1 million more people by 2034, with more than 650,000 of them living in Sydney, according to the latest NSW population projections.

And this will only serve to put even more pressure on Sydney’s rental crisis.

We're just not building enough dwellings in Sydney

The latest ABS Building Approvals data, for May 2026, shows NSW dwelling approvals rose 2.2% for the month, with private house approvals up a stronger 7.8%.

That came after a rough patch, dwelling approvals had fallen 9.5% in April, and house approvals dropped 13.8%, so May's bounce is best read as a partial recovery from a weak start to the year rather than a robust upswing.

Zoom out and the bigger picture is clearer - national dwelling approvals actually fell 1.1% in May to 17,019, even while NSW improved, and NSW's own numbers have been especially volatile through 2026, swinging between double-digit monthly rises and falls across the first five months of the year.

That kind of volatility tells you the development pipeline here is still fragile rather than recovering.

This matters because Sydney's chronic undersupply was never a story about any single month's figures; it's about years of approvals running well below what population growth actually requires.

Even with May's improvement, NSW isn't close to the pace of building needed to close that gap, and construction costs, labour shortages and planning delays continue to make new supply, particularly medium and high-density stock, genuinely difficult to deliver at the pace this city needs.

That ongoing shortfall is one of the main reasons I remain confident in Sydney's long-term growth story, regardless of how any single quarter's price data reads.

A market this structurally undersupplied doesn't stay soft indefinitely once demand and finance conditions align again, and every month of weak approvals now is effectively locking in tighter supply two or three years down the track.

Key trends that will shape Sydney’s housing market in 2026 and 2027

Suburbs benefiting from major infrastructure projects, whether new transport links, hospitals or shopping precincts, are likely to keep outperforming, since these investments tend to draw sustained demand and support values even through a softer broader market.

Areas undergoing genuine gentrification, where older housing stock is being renovated, and lifestyle amenities are improving, continue to offer some of the better capital growth opportunities.

Look for the usual early signs, new cafes and restaurants opening, and young families moving in ahead of the crowd.

Suburbs with strong population growth driven by immigration, young professionals or families remain a reliable indicator of where rental and owner-occupier demand will hold up best.

Sydney's growth this year has genuinely stalled in the face of higher rates and reduced affordability, and I think it's more honest to describe it that way than to claim demand has simply pushed through regardless.

What has held up is the underlying structural picture, population growth, limited new supply, and a persistent shortage of quality established stock in the suburbs people actually want to live in.

The market will remain fragmented through the rest of 2026 and into 2027, with more affluent suburbs, where incomes are higher and homeowners carry substantial equity, likely to hold their ground better than suburbs more exposed to the combined pressure of higher rates and cost of living.

That divergence, rather than a uniform recovery or a uniform decline, is the more realistic picture for Sydney over the period ahead.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

Ready to Invest in Sydney?

If you’re looking to grow your wealth safely and strategically, now’s the time to talk to the team at Metropole Sydney.

Our Sydney-based buyer’s agents and property strategists understand this market inside out—and we’re here to help you make the right move.

👉 Click here to schedule your complimentary Wealth Discovery Chat