Evergrande, China’s second-largest property developer, is in peril.

After a decade of massive growth, including investing in “Fairyland” theme parks, an electric car company, and a professional football team (Guangzhou FC), it is now struggling to service debts exceeding US$300 billion.

So far it has avoided the fate of dozens of its unfinished apartment towers — demolished in spectacular fashion in recent weeks — by selling off assets to make its payments.

But this is not a sustainable strategy.

Credit rating agency Fitch has in the past week downgraded Evergrande to a “C”, indicating exceptionally high risk, with the default “imminent or inevitable, or the issuer is at standstill”.

Without intervention by the Chinese government, the company will collapse. Here are three key ways in which that could affect Australia.

1. Lower demand for iron ore

Evergrande’s collapse will reverberate throughout China’s real estate market. Investors and lenders will be more cautious, potentially resulting in a credit crunch.

This could severely dampen property development, and thereby demand construction materials including steel, made using mostly imported iron ore.

China is by far the world’s biggest steel producer and accounts for nearly 70% of global iron ore imports.

About 60% of that iron ore has been imported from Australia.

This trade has made iron ore Australia’s most valuable export commodity, worth an estimated AU$149 billion in the 2020-2021 financial year.

About 75% went to China.

Any drop in Chinese demand will therefore affect the Australian economy.

China has already been seeking to cut back steel production, a high-energy process, to reduce carbon emissions.

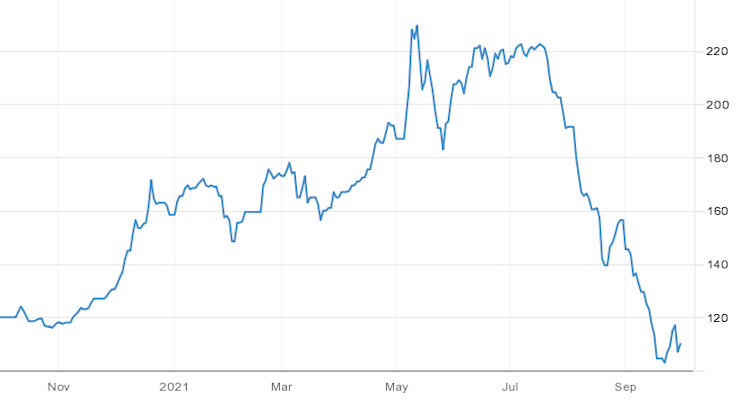

The iron ore price has halved since July.

Plummeting demand for iron ore

tradingeconomics.com/

Further falls in demand and thus prices will affect the Australian businesses and 45,600 jobs employed directly by the industry, as well as the thousands of jobs sustained through their wages, and government revenues from mining-related royalties and taxes.

2. Overall weakening of China’s economy

Beyond the direct effects, problems in China’s real estate and financial sectors could ripple across China’s economy, hurting Chinese demand for other goods and services in which Australia is a major provider.

- Also read:10 questions to ask before buying your next investment property

- Also read:Brisbane housing market update | July 2024

- Also read:Perth housing market update | July 2024

- Also read:Australian housing market update [CoreLogic’s video] | July 2024

- Also read:Unemployment Uptick: What It Means for Interest Rates and the Housing Markets | Property Insiders

To put trade with China in context, Australia’s exports to China are about three times those of our second-most valuable market, Japan. Even with iron-ore exports removed from the equation, China is still our biggest export market.

The effect of China buying less from Australia has been a matter of considerable debate.

Some have argued Australia can compensate by diversifying into other markets.

But such things take time.

Economists Rod Tyers and Yixiao Zhou, who have simulated the effects of the Australia-China trade being shut down, have argued short-term effects could be severe.

3. Global contagion

Evergrande’s debt crisis has echoes of the case of Lehman Brothers, the US investment bank whose bankruptcy in 2008 played a big part in precipitating the Global Financial Crisis.

Although most of Evergrande’s debt is localised in China, in financial and real estate sectors there is always a risk of investors and banks in other markets getting spooked, leading to a credit crunch throughout global markets.

Australian share markets have already fallen off their highs over the past few weeks, certainly in part over concerns about China’s economy.

The mining sector has experienced real carnage, but there are indicators of general unease in falls across all sectors.

Will the Chinese government intervene?

Without external help, Evergrande has a very high likelihood of failure.

All the signs are there. It is averting bankruptcy by servicing the interest payments on its massive debt by selling assets at unfavourable prices.

All eyes are now on the Chinese government as a potential saviour through some form of debt restructure or guarantees.

So far it has not committed itself, and it has taken a strong stance against high debt by developers.

But it may consider Evergrande “too big to fail” — its collapse having potentially disastrous local and global implications.

So some form of intervention to stabilise the situation seems more likely than not.

Australians, and the rest of the world, will need to wait to see exactly what hand the Chinese government will play.![]()

Robert Powell, Professor, Edith Cowan University

This article is republished from The Conversation under a Creative Commons license. Read the original article.