Australia’s housing market started the new year on a high with lending rates and building approvals seeing strong gains.

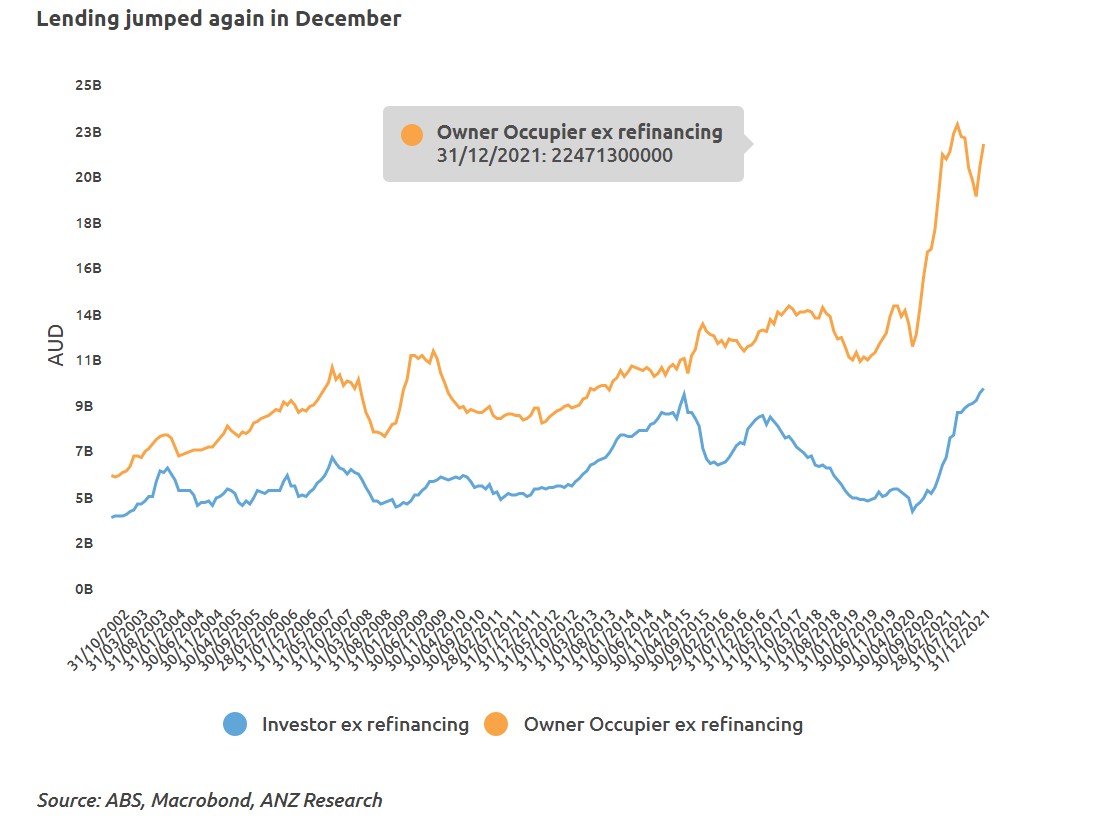

Australia’s housing lending jumped again in December (+4.4 per cent month-on-month).

In a recent ANZ Blue Note, senior economist Adelaide Turnbull explained that there is a growing risk the resurgence of lending could continue in the first half of 2022 as low rates of unemployment and likely stronger savings rates during Omicron support borrowing.

And if lending continues at this pace, the Australian Prudential Regulatory Authority (APRA) may consider more measures to slow it.

Here are some reasons why this may occur

- Owner occupier lending shot up 5.3 per cent month-on-month in December and is now only 4.1 per cent lower than its extraordinary peak in May 2021.”

- Investor lending increased 2.4 per cent month-on-month and has been growing steadily since late 2020.

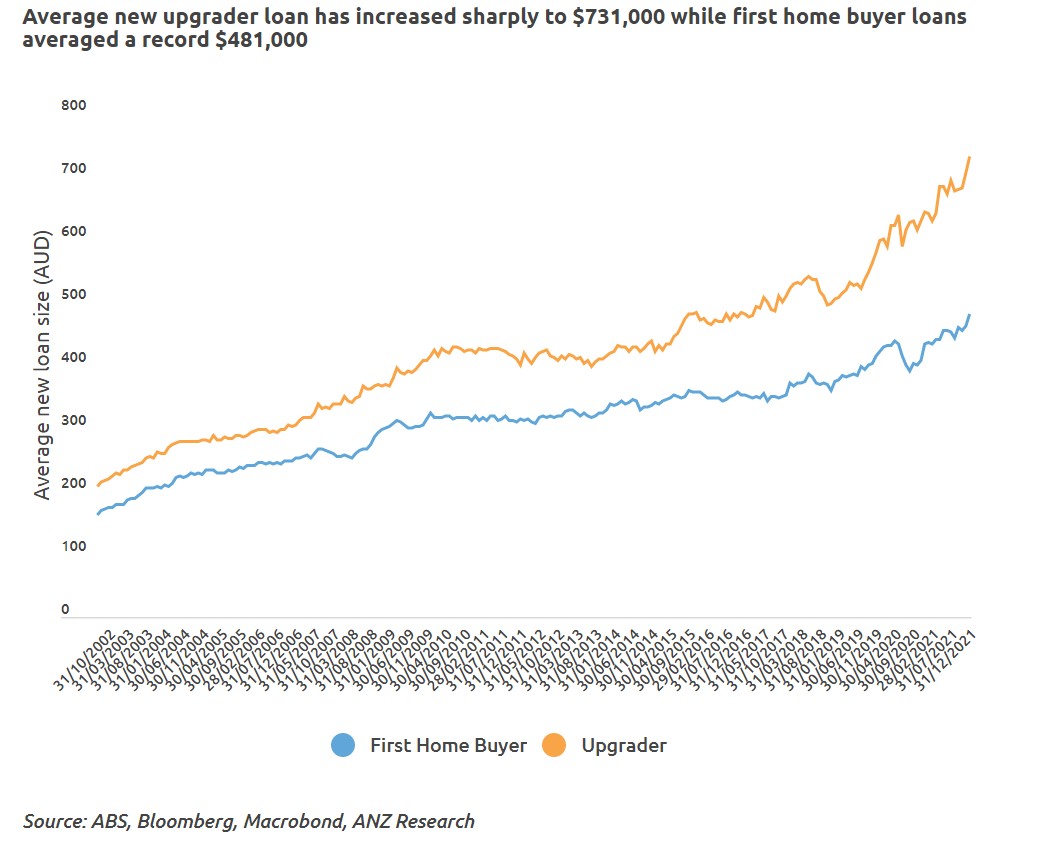

- The average new first home buyer loan size was $A481,000 in December 2021, up 11 per cent year-on-year from $A433,000 in December 2020.

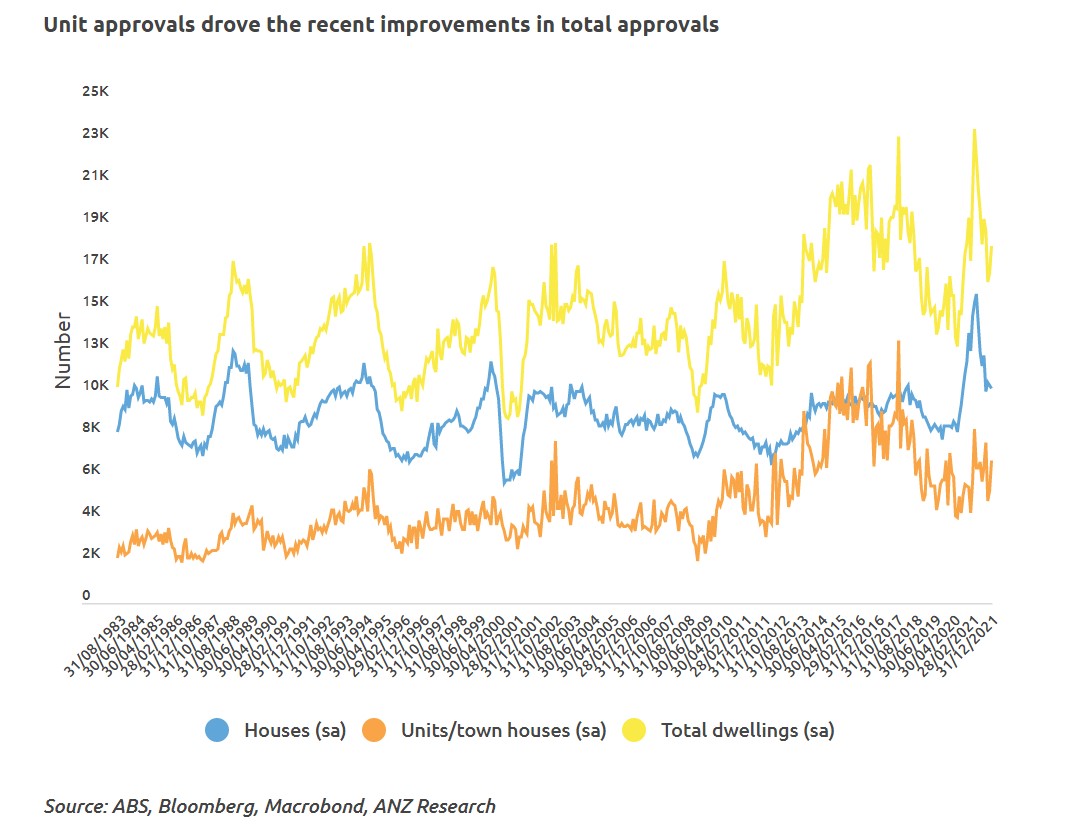

- Residential building approvals also grew rapidly in December (+8.2 per cent month-on-month) due to very strong growth in unit approvals (+27.5 per cent month-on-month), though total approvals in the fourth quarter of 2021 were lower than the third quarter.

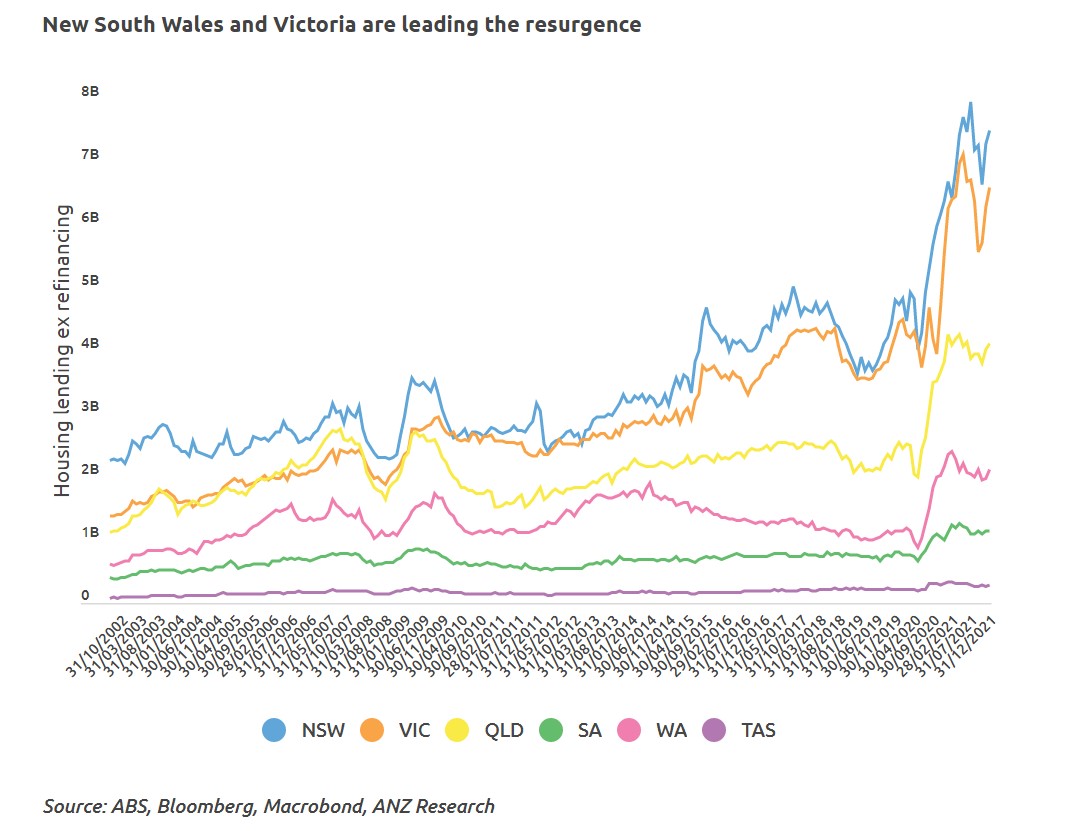

New South Wales units increased 121 per cent in December and were the main driver of strength.

Unit approvals also rose in Queensland (+8.4 per cent month-on-month) and South Australia (+26.8 per cent month-on-month) but fell in other states.

House approvals fell across New South Wales, Victoria, Queensland, South Australia and Western Australia (seasonally adjusted data not provided for Tasmania, Northern Territory or Australian Capital Territory).

- Also read:Sydney housing market update | July 2024

- Also read:10 questions to ask before buying your next investment property

- Also read:Perth housing market update | July 2024

- Also read:Australian housing market update [CoreLogic’s video] | July 2024

- Also read:Latest Asking Prices State by State | Winter Lull takes Affect with Huge falls in Home Listings

The popularity of working from home and low rates are supporting building approvals.

What about interest rates?

A cash rate hike, expected by ANZ Bank in September 2022, will reduce borrowing capacity and could slow activity, though even after one or more increases in the cash rate, the borrowing environment remains broadly supportive.

ANZ Research expects the cash rate to increase to 0.75 per cent by the end of the year and 2 per cent by the end of 2023.

Source: Adelaide Timbrell, Senior Economist at ANZ

ALSO READ: 8 Property trends we can expect in 2022