Key takeaways

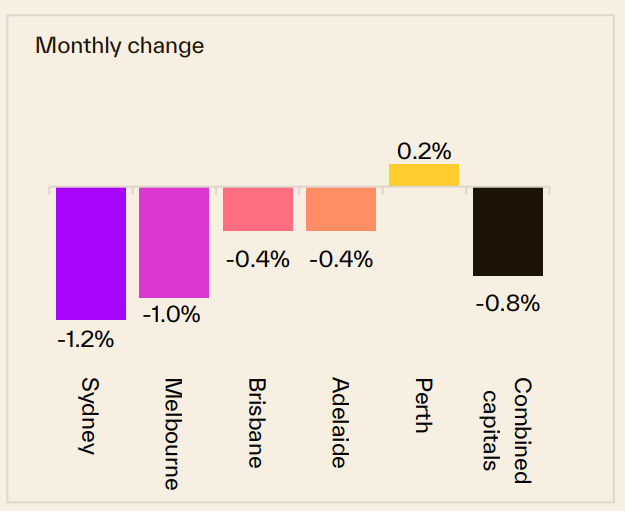

Australia’s property markets have moved into a cooling phase, with capital city dwelling values falling 0.8% over the past month while remaining 4.8% higher than a year ago.

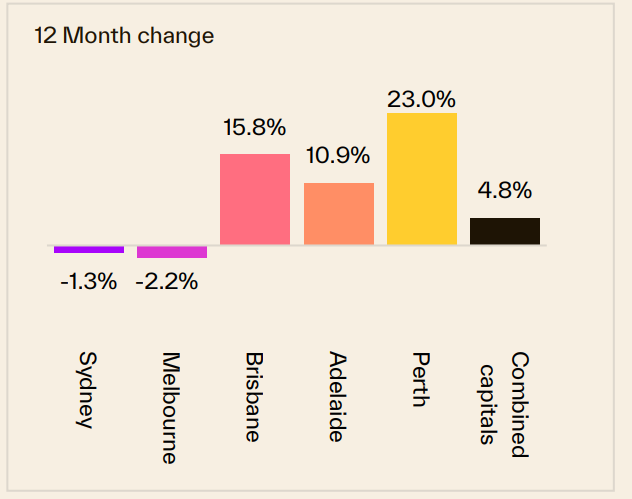

Sydney and Melbourne are leading the downturn, with values now lower than 12 months ago, while Brisbane, Adelaide and Perth continue to record strong annual growth despite losing momentum.

Auction clearance rates remain in the low 50% range, indicating that buyers have become more cautious and vendors must adjust their expectations if they genuinely want to sell.

The labour market remains surprisingly resilient, with 76,300 jobs created in June. This strength, combined with persistent inflation, leaves the door open for another interest rate rise.

Property asking prices are softening across many capital cities, while buyers generally have more choice and negotiating power than they did earlier in the cycle.

Rental conditions remain tight, with national rents rising 5.9% over the past year and vacancy rates remaining exceptionally low. This continues to support investor incomes despite weaker capital growth.

The widening gap between cities, suburbs and individual properties confirms that investors can no longer rely on the general market to lift every asset. Property selection, cash flow management and a long-term strategy matter more than ever.

Sydney just had its worst auction weekend since April 2020, and if you've been wondering when this slowdown would start showing some real teeth, that's your answer.

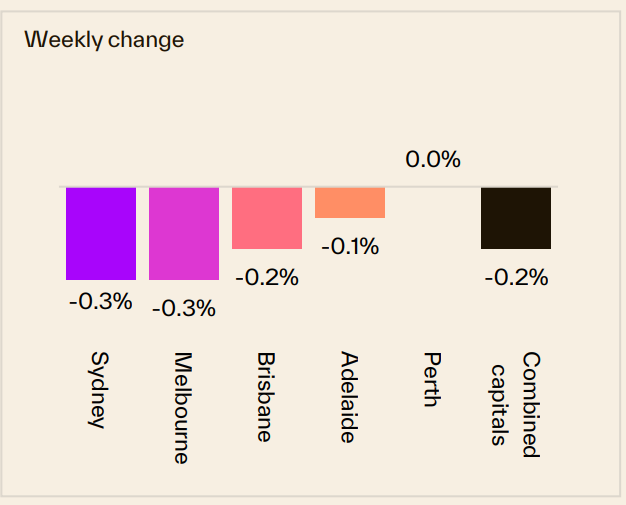

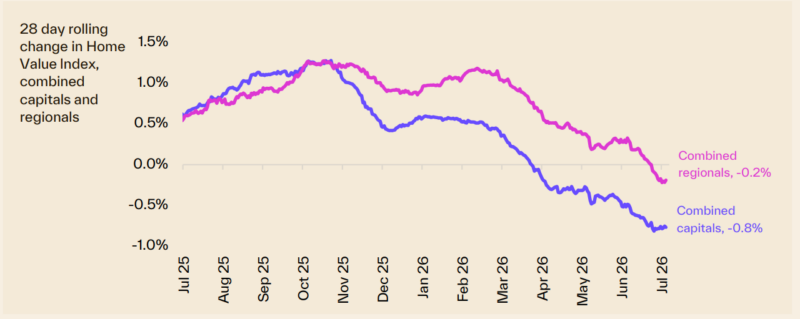

Australia’s property markets have clearly changed direction over the past couple of months, with Cotality's Home Value Index showing values have now fallen around -0.8% over the last month with Sydney and Melbourne down -1.3% and -2.2% respectively from where they sat late last year.

Brisbane, Adelaide and Perth have held up far better through this cycle, but even they are now showing early signs of their own corrections.

At the same time, the Reserve Bank faces a difficult decision when it meets again in August.

The cash rate remains at 4.35% after three increases earlier this year, and the RBA has made it clear that another rise remains possible if inflation fails to ease. Its task has been complicated by the latest employment figures, which showed the economy created 76,300 jobs in June, so everyone will be eagerly watching the CPI figures that come out later this week.

The big four banks are mostly tipping another hold through the rest of the year, while Westpac continues to forecast one more rate rise, with August seen as the most likely timing.

The rental market continues to provide a very different picture. National rents have increased 5.9% over the past year, rental listings remain well below last year’s levels, and vacancy rates are still extraordinarily tight in most capital cities.

This combination of softer property prices and rising rents is gradually improving rental yields, although higher financing and holding costs continue to squeeze many investors.

To my mind, this is exactly what a normal correction looks like after three rate rises and a stretch of policy uncertainty around the coming negative gearing changes.

It's a difficult market if you need to sell right now, but it isn't the kind of structural unwind that should concern long-term investors holding well-located, investment-grade property.

On the auction front this week... clearance rates reach an eleven-week high as auction volumes decline

The preliminary clearance rate across the combined capitals rose to 55.1% last week, the highest in eleven weeks, after a low of 47.4% for the week ending 21 June.

Despite this improvement, clearance rates remain well below the decade average of 68%.

See Cotality's full auction report below.

This week, Cotality also reports that:

- Sydney property prices declined -0.3% over the last week, also declined -1.4% over the last month, and are -2.5% lower than they were 12 months ago.

- Melbourne property prices declined -0.2% over the last week, also declined -1.1% over the last month, are -3.3% lower compared to 12 months ago.

- Brisbane property prices remained flat over the last week, a declined -0.4% over the last month and are 14.5% higher than they were 12 months ago.

Overall, Australian capital dwelling prices declined -0.9% over the last month and are now 3.5% higher than they were 12 months ago.

Clearly, the property cycle is moving on but our markets are very fragmented.

Source: Cotality July 27th 2026

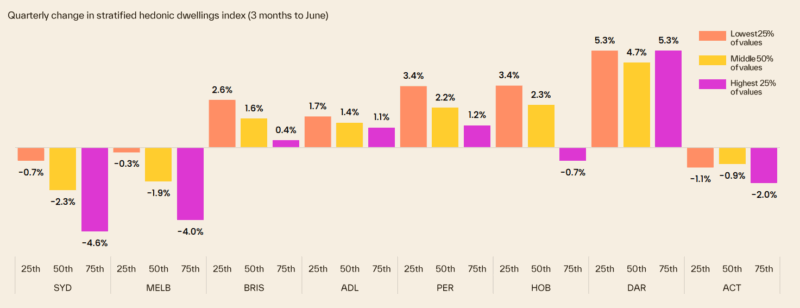

Of course, these are "overall" figures - there is not one Sydney or Melbourne or Brisbane property market.

And various segments of each market are performing differently.

At the beginning of this cycle the upper quartile of the market lead the upswing but last year the lower quartile across every capital city recorded a stronger outcome for housing values relative to its upper quartile counterpart.

The following chart shows how various segments of each capital city market are performing differently, with median-priced properties performing well.

To help keep you up-to-date with all that's happening in property, here is my updated weekly analysis of data and charts as of 27th July 2026, provided by SQM Research, Cotality, and realestate.com.au.

Current property asking prices

Property asking prices are a useful leading indicator for housing markets - giving a good indication of what's ahead.

Here is the latest data available:

Sydney

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 2,057.920 | 5.070 | -1.4% | -0.3% |

| All Units | 887.373 | -2.373 | -2.8% | 2.7% |

| Combined | 1,579.162 | 2.026 | -1.8% | 0.3% |

Source: SQM Research

Melbourne

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,307.199 | -3.872 | -1.0% | 0.7% |

| All Units | 677.626 | 0.088 | -1.0% | 7.9% |

| Combined | 1,08.003 | -2.619 | -1.0% | 1.9% |

Source: SQM Research

Brisbane

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,384.952 | -5.852 | -0.6% | 10.6% |

| All Units | 859.686 | -3.086 | -2.4% | 16.8% |

| Combined | 1,251.811 | -5.151 | -0.9% | 11.5% |

Source: SQM Research

Perth

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,285.052 | -12.752 | -0.7% | 11.9% |

| All Units | 775.032 | -2.412 | -1.2% | 19.4% |

| Combined | 1,150.921 | -10.033 | -0.8 | 13.1% |

Source: SQM Research

Adelaide

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,130.065 | -7.232 | 0.0% | 8.0% |

| All Units | 631.357 | 1.443 | 1.1% | 13.1% |

| Combined | 1,040.112 | -5.667 | 0.1% | 8.5% |

Source: SQM Research

Canberra

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,255.174 | -12.187 | -1.8% | 2.8% |

| All Units | 602.653 | -3.778 | -1.8% | 1.2% |

| Combined | 1,006.537 | -8.983 | -1.8% | 2.0% |

Source: SQM Research

Darwin

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 837.965 | 7.835 | -1.3% | 5.3% |

| All Units | 490.799 | 4.451 | 4.4% | 16.7% |

| Combined | 701.399 | 6.504 | 0.2% | 8.2% |

Source: SQM Research

Hobart

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 923.855 | -5.219 | -1.4% | 9.7% |

| All Units | 540.765 | -2.965 | -3.0% | 8.2% |

| Combined | 865.125 | -4.873 | -1.5% | 9.5% |

Source: SQM Research

National

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,071.032 | -3.387 | -0.1% | 6.6% |

| All Units | 655.465 | 1.295 | -0.2% | 11.2% |

| Combined | 980.466 | -2.367 | -0.1% | 7.2% |

Source: SQM Research

Cap City Average

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,528.972 | -2.334 | -0.9% | 2.8% |

| All Units | 790.359 | -0.171 | -1.5% | 6.2% |

| Combined | 1,307.286 | -1.685 | -1.1% | 3.2% |

Source: SQM Research

The value of property asking prices as a leading indicator for housing markets is quite significant.

In fact it's more valuable than median prices which can be quite misleading.

Let's delve into why this is the case and how it impacts the real estate market.

- Early Market Sentiment Indicator: Asking prices often reflect the current sentiment of sellers in the real estate market.

If sellers are confident, they might set higher asking prices, anticipating strong demand.

Conversely, if sellers are uncertain or perceive a market downturn, they might lower their asking prices to attract buyers.

This makes asking prices a real-time indicator of market sentiment, often preceding changes in actual sales prices. - Predictive of Future Price Trends: Trends in asking prices can be predictive of where the actual property prices are headed.

For example, a consistent rise in asking prices over a period can signal an upcoming rise in transaction prices. - Impact of Economic Factors: Economic factors such as interest rates, employment rates, and broader economic health influence asking prices.

For instance, changes in the Reserve Bank of Australia's policies or shifts in the job market can quickly reflect in the asking prices, providing insights into how these factors are influencing the housing market. - Regional Variations: In a diverse market like Australia's, asking prices can also provide insights into regional disparities.

For instance, the property markets in Melbourne and Sydney might behave differently from those in Brisbane or Perth. Asking prices can give early indications of these regional trends. - Influence of Supply and Demand: Asking prices are also a response to the balance of supply and demand in the market.

In areas with limited supply and high demand, asking prices tend to be higher and vice versa.

However, it's important to note that while asking prices are a valuable indicator, they should not be used in isolation.

Other factors like actual sales prices, time on the market, auction clearance rates, and economic conditions also play crucial roles in understanding the property market dynamics.

READ MORE: The latest median property prices in Australia’s major cities

Last weekend's auction report

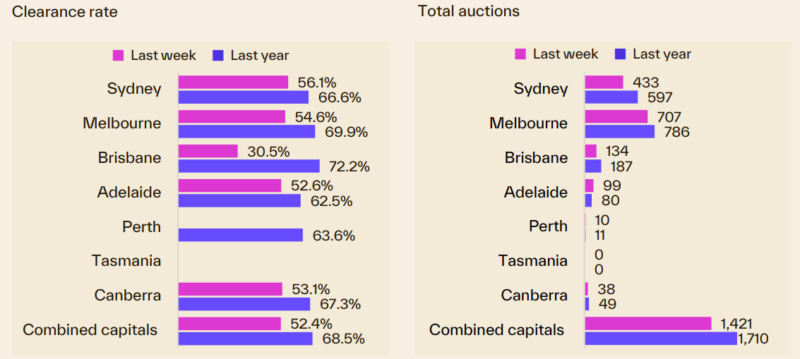

Capital city clearance rates hold in the low 50% despite a lift in auction volumes

Auction volumes have increased modestly over the past two weeks, rising by 4.0% last week following a 4.8% lift two weeks ago to reach 1,421 events.

That said, these increases came off a relatively low base, and auction volumes have remained consistently below levels recorded a year ago, with volumes last week 16.9% lower than the same period in 2025.

The preliminary clearance rate has remained in the low 50% range over the past three weeks, edging up to 52.4% last week.

This was an increase of 2.4 percentage points from the previous week's 50.0% and 5.0 points above the recent low of 47.4% for the week ending June 21.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:53 years of valid reasons not to invest

An improvement in the withdrawal rate helps explain the lift in clearance rates.

Withdrawn auctions had risen to 24% of all scheduled auctions over the week ending June 21 but reduced back to 17.4% last week.

The withdrawal rate remained elevated relative to 2025, when on average 11.8% of auctions were being withdrawn.

Melbourne held 707 auctions last week, up 18% from the previous week but 10.1% lower than the same week last year.

The preliminary clearance rate declined by 1.9 percentage points to 54.6%.

After reaching a low of 50.2% for the week ending June 28, the rate has remained in the mid-50% range over the past four weeks.

433 auctions were held in Sydney last week, a 2.3% week-on-week reduction and 27.5% lower than at the same time last year.

The preliminary clearance rate rose to 56.1%, a solid bounce from the 47.4% recorded the previous week. That rise came despite 29.8% of scheduled auctions being withdrawn from the market.

Of the successful Sydney auctions, 63.4% sold before the property went under the hammer.

In Brisbane, 134 homes were auctioned last week, representing an 18.3% decrease from the previous week and a 28.3% decline compared with the same period last year.

The preliminary clearance rate fell to 30.5%, a decrease of 5.4 percentage points and the second lowest preliminary result recorded this year.

Adelaide was one of the few markets busier than a year ago, with its 99 auctions almost 24% above the same time in 2025, though down 10% on the previous week.

The preliminary clearance rate dipped to 52.6%, down 2.3 percentage points and the third lowest preliminary result so far this year.

At 53.1%, the ACT reported its strongest preliminary rate in nine weeks.

The territory held 38 auctions last week, 9.5% fewer than the previous week and 22% fewer than the same time last year.

Perth held 10 auctions last week, with only 25% reporting a positive result, and no auctions were held in Tasmania.

The number of auctions is expected to increase this week, with approximately 1,570 homes currently scheduled for auction.

Our rental markets

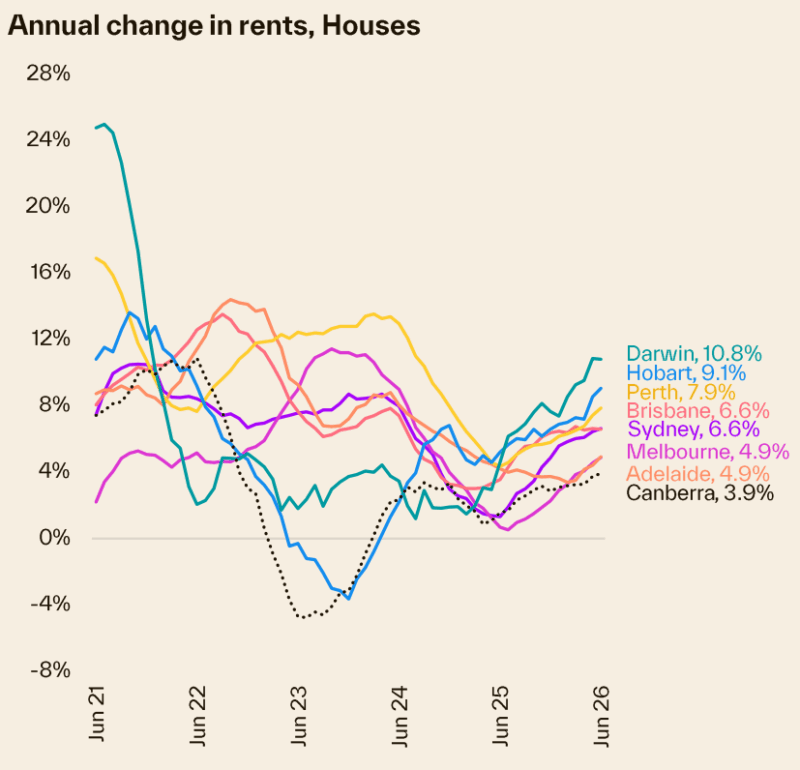

Cotality’s national rental index rose half a per cent in seasonally adjusted terms (0.4% unadjusted) in June, on par with the 0.5% recorded in May, but slightly lower than the recent high point of 0.6% growth recorded in January.

Annual rental growth held at 5.9% nationally over the financial year, adding approximately $40/week to the median rent.

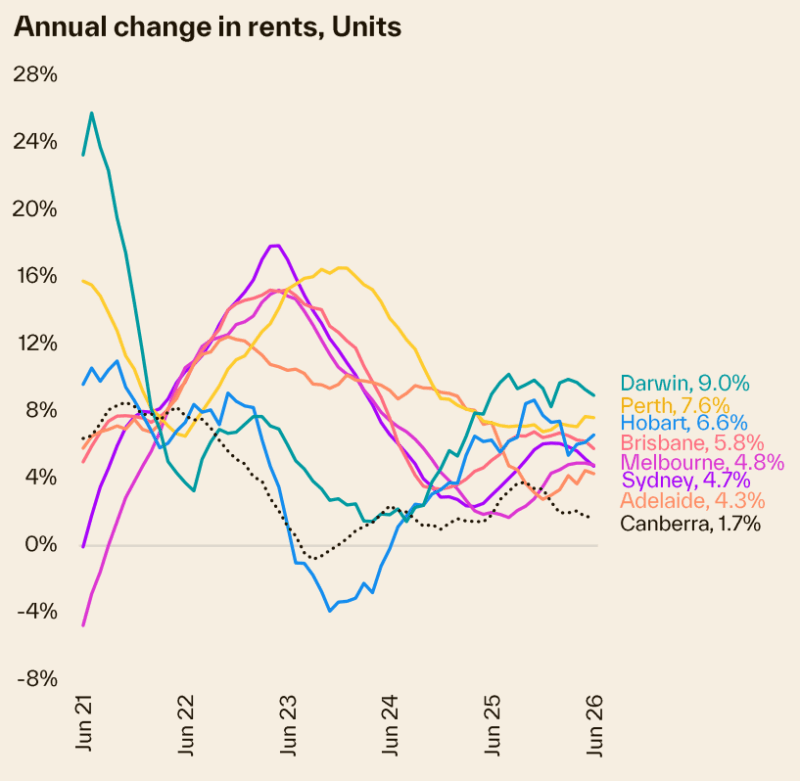

Across the broad regions of Australia, annual rental growth ranged from 10.1% in Darwin and regional Tasmania to 3.2% in the ACT and regional NT.

Capital city rents have risen by 41.7%, or $217 a week, over the past five years.

Sydney continues to record the most expensive rental rates, with a median of $883 a week for houses and $783 a week for units.

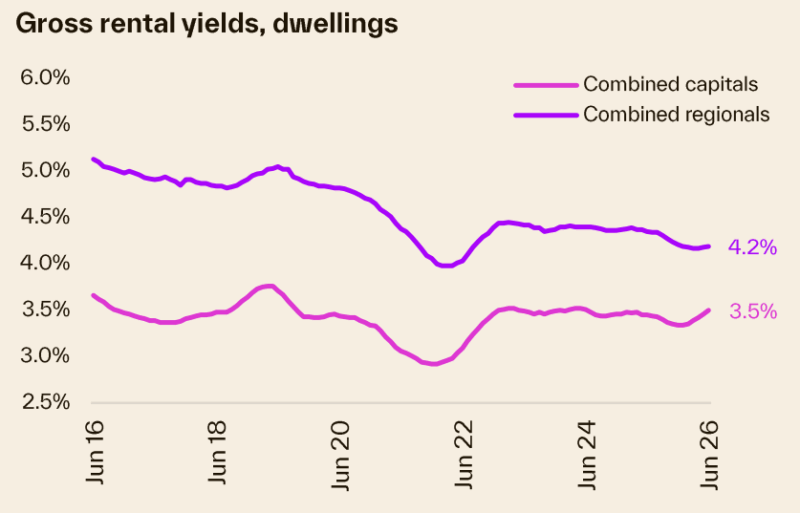

With rents rising faster than home values, we are seeing a gradual but consistent rise in gross rental yields.

Across the combined capitals, the gross rental yield is averaging 3.50%, up from a recent cyclical low of 3.34% in December last year and a record low of 2.92% in January 2022.

Sydney

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $1,147.66 | -3.65 | -1.1% | 7.1% |

| All Units | $758.27 | 0.74 | -0.3% | 7.6% |

| Combined | $916.29 | -1.05 | -0.7% | 7.4% |

Source: SQM Research

Melbourne

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $818.01 | 2.98 | 0.5% | 6.4% |

| All Units | $604.74 | 0.26 | 0.0% | 5.0% |

| Combined | $694.43 | 1.41 | 0.2% | 5.8% |

Source: SQM Research

Brisbane

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $830.70 | -3.70 | 0.1% | 8.7% |

| All Units | $643.62 | 0.38 | -0.1% | 6.3% |

| Combined | $746.39 | -1.86 | 0.0% | 7.7% |

Source: SQM Research

Perth

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $891.29 | 6.71 | -0.8% | 6.8% |

| All Units | $669.93 | -0.93 | -1.0% | 2.1% |

| Combined | $800.07 | 3.56 | -0.9% | 5.2% |

Source: SQM Research

Adelaide

| Property Type | Rent $) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $686.01 | -1.01 | -0.2% | 2.5% |

| All Units | $555.05 | -5.06 | -0.2% | 5.9% |

| Combined | $641.97 | -2.37 | -0.2% | 3.5% |

Source: SQM Research

Canberra

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $841.91 | 1.08 | 1.0% | 9.2% |

| All Units | $603.70 | -2.69 | 0.6% | 2.7% |

| Combined | $710.56 | -1.00 | 0.8% | 5.9% |

Source: SQM Research

Darwin

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $844.77 | 10.24 | 1.9% | 3.9% |

| All Units | $660.04 | 5.96 | 3.7% | 21.8% |

| Combined | $735.79 | 7.71 | 2.8% | 12.7% |

Source: SQM Research

Hobart

| Property Type | Rent 9$) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $616.10 | -11.10 | -1.0% | 8.0% |

| All Units | $578.40 | 1.60 | 0.0% | 17.7% |

| Combined | $601.09 | -6.05 | -0.6% | 11.5% |

Source: SQM Research

National

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $777.00 | 0.00 | -0.1% | 8.1% |

| All Units | $603.00 | -2.00 | -0.2% | 6.5% |

| Combined | $696.51 | -0.92 | -0.1% | 7.5% |

Source: SQM Research

Cap City Average

| Property Type | Rent ($) | Weekly change | Monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $924.00 | 4.00 | -0.3% | 6.7% |

| All Units | $682.00 | 1.00 | -0.3% | 6.1% |

| Combined | $795.57 | 2.41 | -0.3% | 6.5% |

Source: SQM Research

Here's how many properties are for sale at the moment

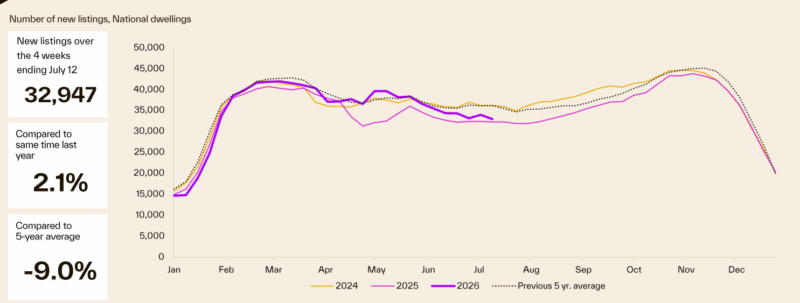

New listings tracked closely with the five - year average through the first half of the year and remained above 2025 levels for most of the year.

Listing activity has softened from a peak in early March, trending downwards through winter, closing 2.1% above year ago levels and 9.0% below the five - year average.

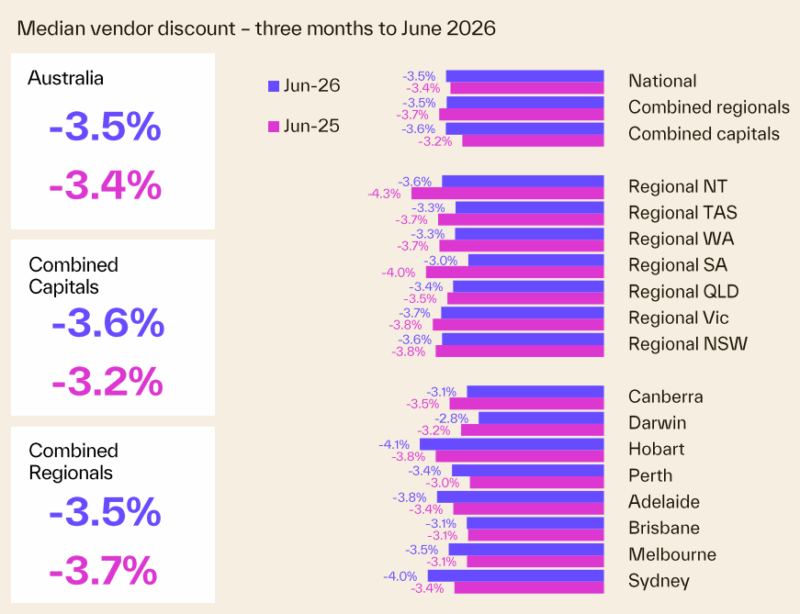

Vendor metrics

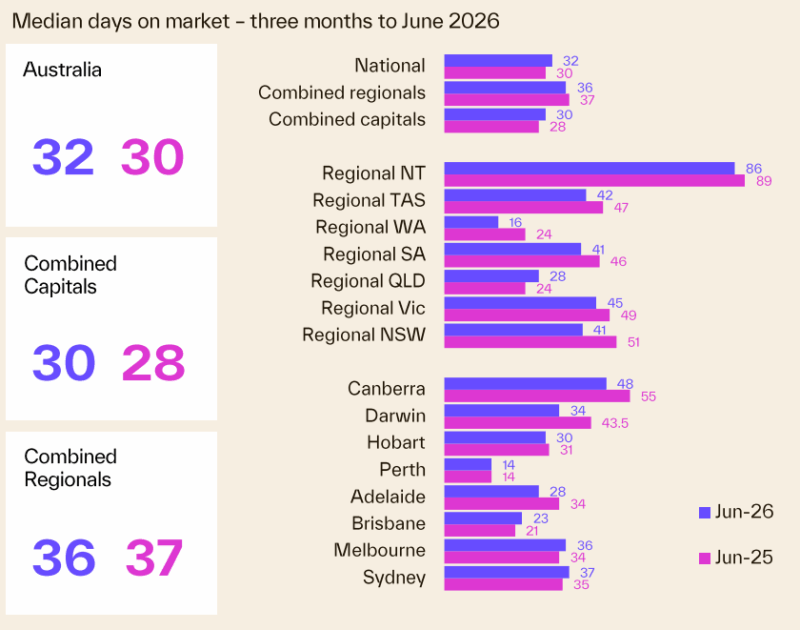

Compared to a year ago, homes are taking slightly longer to sell.

Nationally, homes are taking slightly longer to sell, with the median time on market rising to 32 days.

Since late 2025 selling conditions have softened across both the capital city and regional markets.

The rise in selling times has become more noticeable in recent months, with the median time to sell increasing to 30 days across the capitals and reaching 36 days across the regional markets.

This is a clear sign of cooling conditions and increasing supply.