Key takeaways

Westpac now forecasts dwelling price growth to finish flat across the major capital cities for 2026.

The budget's negative gearing and CGT changes are expected to drive a 34% fall in new investor activity and a 20% decline in total market turnover

Existing investors are grandfathered - your current properties retain their negative gearing and CGT discount entitlements, giving you a strong reason to hold rather than sell

New builds are now the most tax-advantaged option for investors entering the market, with negative gearing and the choice of either the 50% CGT discount or inflation indexation still available, however, these often are inferior investments.

The RBA has already raised rates three times this year and Westpac expects two more increases before year end, adding further pressure on top of the tax changes

The legislation hasn't passed yet - it still needs Senate support, so some uncertainty remains around the final shape of the reforms

Over the medium term, rental yields are expected to gradually firm and new dwelling construction is expected to lift as investor demand shifts toward newly built stock

The Federal budget on May 12 changed the rules for property investors in ways that most people are still working through, and Westpac's economics team has now put some concrete numbers around the likely market impact.

If you've been wondering how to think about the combination of the tax changes and rising interest rates, I'll explain the details of the latest Westpac Housing Forecast.

What Westpac is now forecasting

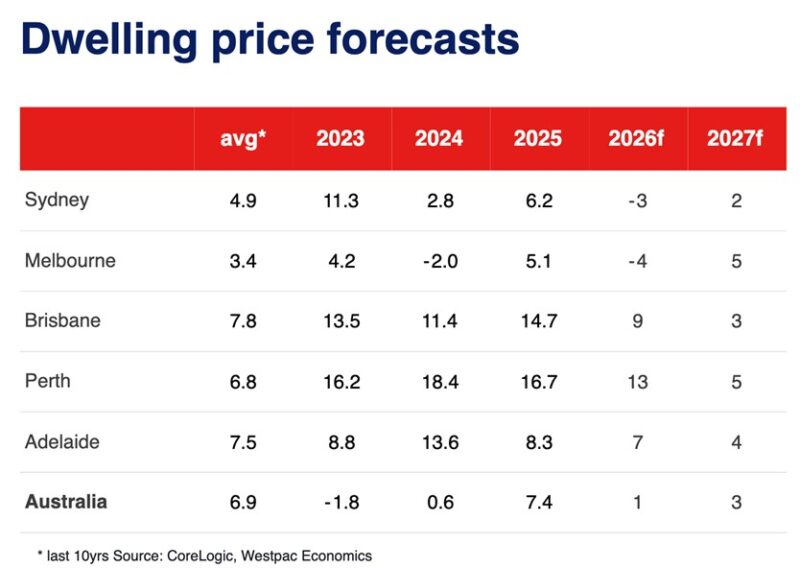

Westpac's economists Matthew Hassan, Luci Ellis and Mantas Vanagas released their updated housing forecast on May 26, concluding that the combination of the budget's tax changes and rising interest rates is expected to produce a 34% fall in new investor activity, a 20% decline in total dwelling turnover, and average dwelling price growth that stalls flat across the major capital cities for 2026.

To put that in plain English - the property market is expected to hit the brakes.

Now remember, our housing market started to slow down earlier this year, even before the Reserve Bank started raising interest rates, before the Middle East war, and before the budget.

And once things settle down, the market will likely keep moving forward as it always has.

As the table above shows, the story is very much a two-speed market - the stronger, tighter-supply cities continuing to grow, while the southern capitals face more pressure for the second half of this year.

The tax changes driving this

The two main changes from the budget are a shift in the capital gains tax discount from the flat 50% rate that has applied since 1999 to a cumulative inflation adjustment from July 2027, with a new minimum tax rate of 30%; and the removal of negative gearing deductions against non-property income for any new residential property investment from budget night onwards.

For investors who have held properties for a long time and generated substantial gains above inflation, the change to CGT is particularly significant.

Westpac notes that where capital gains are less than double the cumulative rise in inflation over the holding period, the indexation treatment is actually slightly more favourable than the previous 50% discount - but large capital gains are treated very differently, with the 50% discount having been a much bigger concession than inflation adjustment in those cases.

The change to negative gearing is arguably the bigger shift for most investors.

What happens to existing investors

One thing that's important to understand is the grandfathering provisions.

Negative gearing will continue to be available for investments made prior to budget night, and capital gains on existing investments up to July 2027 will also continue to receive the 50% discount.

This is meaningful protection for long-term holders, and Westpac makes an interesting observation about what it implies for behaviour.

The grandfathering of changes strongly encourages current holders of leveraged, negatively geared investments to retain those assets for as long as possible, and to maximise tax benefits, potentially by carrying higher levels of debt against the asset.

So if you're already in the market with existing properties, the rules haven't really changed for you, and you now have an even stronger incentive to hold rather than sell.

That's worth keeping in mind when people talk about a wave of investor selling. Westpac doesn't expect that, and I don't either.

The new build opportunity

Here's where it gets interesting for investors thinking about what comes next.

New investments in newly built dwellings will still be able to be negatively geared and will have an option for capital gains to be discounted by either 50% or cumulative inflation - whichever is more favourable.

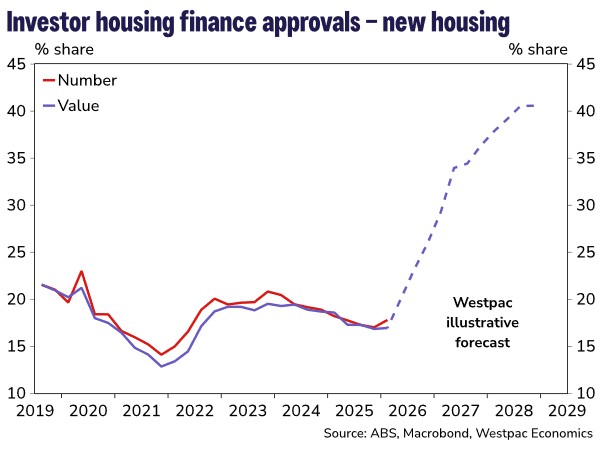

Currently around 18% of new investor finance approvals are for newly built dwellings, but Westpac expects this share to potentially rise towards 40-50% of new investor loans as the relative attractiveness of new stock compared to existing property shifts significantly.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:53 years of valid reasons not to invest

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

If this occurs as suggested by Westpac's forecast in the chart above, it will mean that a whole wave of new investors will be buying off-the-plan apartments and house-and-land packages in the outer suburbs, both of which have consistently underperformed over the long term.

The interest rate backdrop

Of course, the tax changes don't sit in isolation - they land on top of a tightening interest rate environment.

The RBA has already raised rates three times, taking official rates back to the restrictive levels that prevailed through 2023-24, and Westpac expects two further 25 basis point increases in the coming months.

That's a significant headwind on top of the tax changes, and it explains why Westpac's near-term forecasts have become more cautious.

Having said that, most other major banks only expect one interest rate increase moving forward.

The risk of a short-term air pocket

Westpac flags one near-term risk that investors should be aware of.

Lower turnover combined with uncertainty about the impacts of the tax policy changes could see sharper price movements, particularly with the RBA also expected to raise interest rates further in the second half of the year - though this risk is mitigated somewhat by grandfathering provisions and the fact that initial post-budget surveys suggest price expectations remain well-anchored.

I think that's a fair assessment. Markets don't like uncertainty, and we're in a period where the full legislative shape of these changes is still being worked out.

The longer-term picture

Beyond the near-term volatility, Westpac outlines some medium and longer-term shifts that are significant for investors.

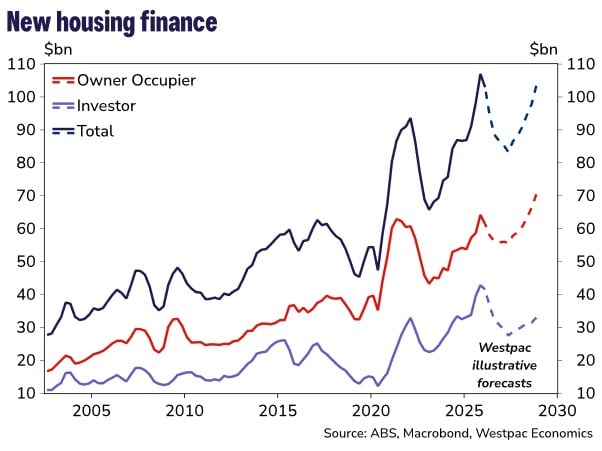

Over the medium term, Westpac expects a gradual firming in rental yields as markets adjust after-tax investment returns, along with a gradual rise in dwelling approvals as more investor activity is directed towards newly built dwellings.

Over longer horizons, they also expect more concentrated "landlordism" - where ownership of rental properties becomes more concentrated among specialists for whom this is their primary business, and more muted price cycles as investor activity generally becomes less cyclical.

What this means if you're an investor

The key point for existing investors is that the case for holding quality assets in the right locations hasn't changed. You're grandfathered, your tax position is protected, and the underlying demand drivers - population growth, tight supply, genuine housing undersupply - haven't gone away.

For investors who haven't yet built their portfolio, the environment has become more complex.

The fundamentals that matter to me - scarcity, demographics, location quality - still apply. The rules around the tax treatment have changed, but that doesn't change which properties will be the ones that outperform over the next decade.

If you're concerned about how potential tax changes could affect your property portfolio, speaking to one of our Metropole Wealth Strategists is a good starting point.

At Metropole, we're much more than another buyer's agency. We help our clients grow, protect, and pass on their wealth through strategic property and wealth advice.

Why not book a complimentary chat with one of our wealth strategists by clicking here? To us, property is the vehicle, but strategy is the driver.