Key takeaways

Pessimism is a poor investment strategy. Bad news attracts attention, but investors who focus on fear and short-term noise often miss long-term wealth-building opportunities.

Successful investing requires optimism about the future. Property investment is based on the belief that population growth, economic progress, and housing demand will continue to support asset values over time.

Long-term property performance has been remarkably strong. Despite market cycles and temporary setbacks, Australian residential property has delivered substantial wealth creation over the long run, particularly for investors who own quality assets.

Market timing usually does more harm than good. Waiting for the perfect buying opportunity or trying to predict short-term movements often results in missed opportunities and lower returns.

Focus on what you can control. The quality of your properties, financial buffers, borrowing structure, and investment timeframe have a far greater impact on success than predicting the next market move.

Turn on the news or check out social media morning and you'd be forgiven for thinking the property market is on borrowed time.

Interest rates, housing affordability, cost of living pressures, geopolitical tensions and now the budget change - the list of worries seems to grow faster than property values.

Yet, after watching markets move through multiple cycles over the past five decades, I've come to a firm conclusion: the investors who let that noise drive their decisions consistently end up worse off than those who stayed patient and optimistic.

This isn't about wearing rose-coloured glasses.

It's about understanding what actually drives long-term wealth, and recognising that pessimism, as comfortable as it sometimes feels, has a very poor track record as an investment strategy.

AMP's Chief Economist Dr. Shane Oliver recently wrote a piece on why it pays to be an optimist as an investor, and while his focus was on shares, his three core arguments translate almost perfectly to property.

I want to share my own version of them here, because I think they're worth sitting with - especially right now.

Why bad news feels louder than it used to

Before I get to the three reasons, it's worth understanding why so many investors are struggling with pessimism in the first place.

Dr. Oliver points out that our brains are wired to pay more attention to bad news than good. This goes back to basic human survival instincts, where spotting threats quickly was a matter of life and death. The problem is that same hardwiring now works against us as investors.

Bad news is dramatic and immediate ("Millions wiped from the housing market"), while good news tends to be quiet and incremental ("Sydney property values up 0.4% this month").

The dramatic story gets the clicks, the shares, the social media traction and the worry gets amplified far beyond what the underlying data actually supports.

Add to that the explosion in financial commentary across podcasts, social media, YouTube channels and newsletters, and investors today are being hit with more conflicting opinions than any previous generation had to navigate.

Much of it is noise, but it's hard to recognise it as noise when your loss-aversion instincts are nudging you toward every warning signal.

The result is that many investors are more distracted, more jittery and more short-term focused than ever before - at precisely the time when the fundamentals for long-term property investment remain very solid.

Reason 1: Without optimism, there's no real reason to invest at all

This might sound obvious, but it's worth stating plainly.

If you genuinely believe property values will fall permanently, that rents will dry up, that the demand for well-located housing in Australia's major cities will collapse, then there's no logical case for owning investment property.

Investing in any asset requires a foundational belief that the future will be better than the present, or at least that human ingenuity, population growth and economic progress will continue to create demand for scarce, well-located assets over time.

As Benjamin Graham, one of the most respected investors in history, put it: "To be an investor you must be a believer in a better tomorrow."

That's not naivety. It's the logical starting point for putting capital to work.

And for Australian residential property, the fundamentals underpinning that optimism - growing population, chronic undersupply, strong preference for homeownership, and concentrated economic activity in our major cities - remain intact.

As I see it, the two big drivers of housing property price growth will be population growth and demographic trends, as well as our nation's increasing wealth.

Reason 2: The long-term numbers are very hard to argue with

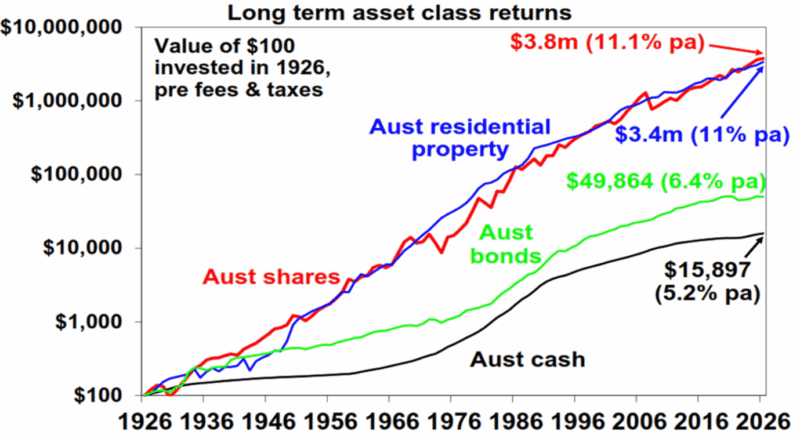

The chart below from Dr. Shane Oliver shows what happened to $100 invested across different Australian asset classes since 1900, with income reinvested along the way.

Source: Dr. Shane Oliver AMP

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – July 2026

Cash is safe, but that $100 has grown to around $16,000 today. Bonds have done better, reaching around $50,000. But residential property and shares have both grown that $100 to multi-million dollar sums - property delivering similar long-term returns to shares over the full period.

Now, that line for property in the chart represents the average. And here's where I think property investors have an advantage over sharemarket investors - because with property, you're not forced to hold the average.

You can research, select and acquire properties in the top tier of the market investment-grade assets in inner and middle-ring suburbs of our major cities, with the demographic and infrastructure drivers that consistently outperform the averages.

The average investor buys average properties and gets average results. The strategic investor focuses on scarcity, owner-occupier appeal and long-term demand, and the compounding effect over 20 or 30 years is genuinely transformative.

And of course, you have the benefit of leverage to compound the returns on your funds.

Sure there have been periods along that 120-plus year chart where property values fell, where growth stalled, where headlines screamed that the property market was finished.

Yet every single time, the long-term trend reasserted itself. I don't see any compelling reason why the next few decades will be different.

Reason 3: Trying to time the market almost always backfires

This is where I see experienced investors come unstuck more than anywhere else.

They see a period of slower growth or falling values and decide to wait for the bottom before buying.

Or they sell good assets during a soft patch to "protect their equity." Or they pause their plans for 12 to 24 months while they see how things play out.

Getting too caught up worrying about the two or three years in every decade when the market is soft means you risk sitting on the sidelines during the seven or eight years when the real wealth building happens.

The investors I've seen build genuine, lasting wealth over the decades are not the ones who perfectly timed every cycle. They're the ones who bought quality properties, held them through the inevitable periods of weakness, kept their financial buffers solid and let time do the heavy lifting.

The real risk isn't a market correction

In my experience, the biggest risk most property investors face isn't a pullback in values or a period of soft rental growth.

It's letting fear and negative sentiment cause them to delay good decisions, exit positions too early or avoid the market altogether during the very periods that, in hindsight, turn out to be the best buying windows.

As Dr. Oliver writes, optimism doesn't mean ignoring risks or jumping into every investment that crosses your desk.

It means maintaining a realistic, evidence-based confidence that quality assets in well-chosen locations will grow in value over time, and that the short-term noise - no matter how loud it gets - rarely alters that long-term trajectory.

The philosopher J.S. Mill observed nearly 200 years ago that the person who despairs when others hope tends to get far more credit for wisdom than the person who maintains a reasonable confidence.

That's still true today. But in investing, as in life, the data comes down firmly on the side of the quiet optimist. In fact, I don't know any rich pessimists.

If you're feeling uncertain about where the property market goes from here, I'd encourage you to focus on what you can control - the quality of the assets you hold, your financial buffers, your borrowing structure, and your investment timeframe.

Those are the levers that matter most, and getting them right is far more valuable than trying to predict the next six months of price movement.

If you're concerned about how the current economic conditions or recently announced tax changes could affect your property portfolio, speaking to one of our Metropole Wealth Strategists is a good starting point.

At Metropole, we're much more than another buyer's agency. We help our clients grow, protect, and pass on their wealth through strategic property and wealth advice.

Why not book a complimentary chat with one of our wealth strategists by clicking here? To us, property is the vehicle, but strategy is the driver.