Key takeaways

According to Westpac Bank, 60% of people plan to buy a property in the next five years, yet the heartbreaking battle facing first home buyers is getting harder.

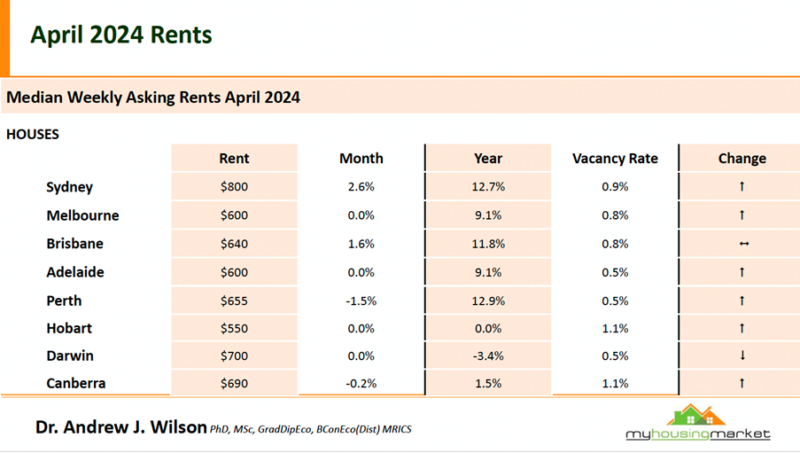

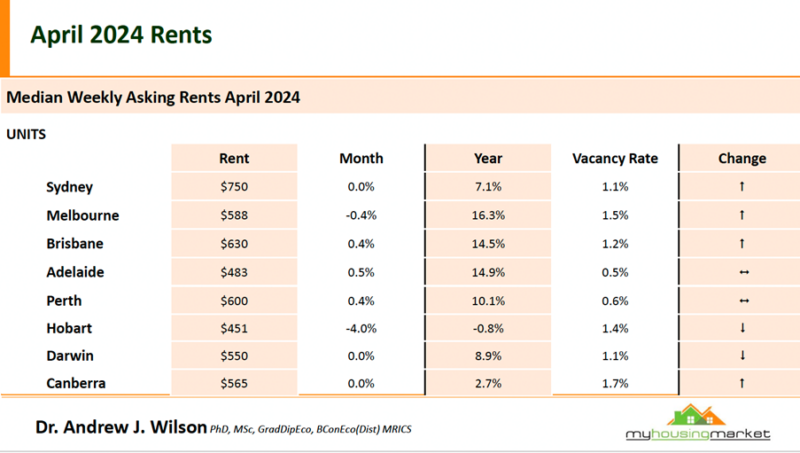

The latest My Housing Rental Report showed mixed results over April, with vacancy rates easing in most capitals, although generally remaining very low and continuing to favour landlords. Any sustained relief for tenants will prove to be short-lived.

Affordability constraints mean many tenants are now looking at renting apartments, but demand for rental accommodation remains high, with strong net overseas migration creating significant demand for rental accommodation in our capital cities.

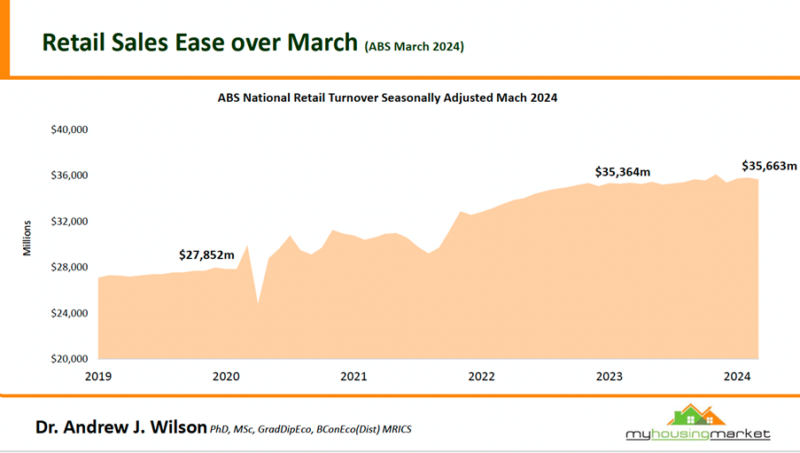

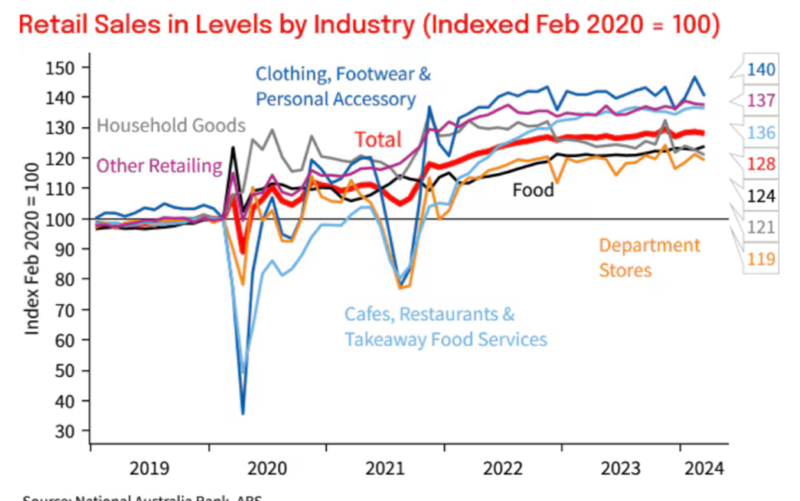

The latest retail sales figures show that retail sales fell 0.4% over the last month, with higher spending on food offsetting the fall in household goods spending.

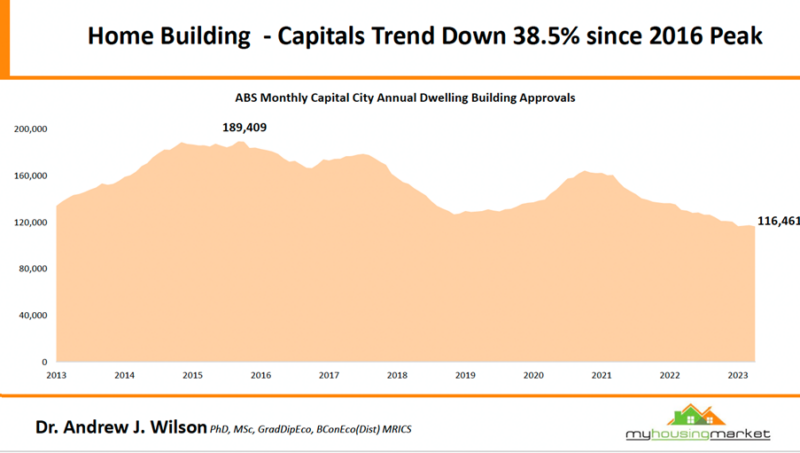

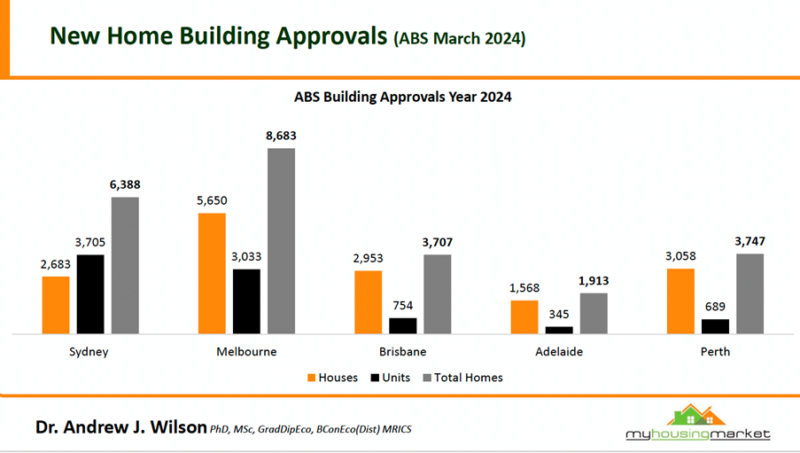

Home building approvals have risen 3.7% over March, but the annual levels of building approvals are chronically depressed, with the quarterly trend falling. Despite the will of governments to get home-building activity moving, there are still too many obstacles in our way.

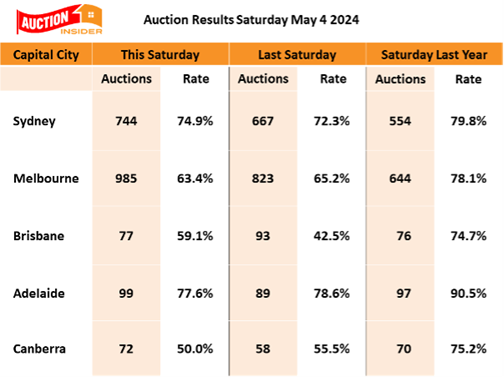

The auction markets in the capital cities have reported stable results to begin May, with Adelaide having the strongest auction clearance rate of 77.6%. The national weekend auction market reported a clearance rate of 65.0%, which was higher than the previous weekend but still well below last year.

Australia is a nation obsessed with house prices, and according to a recent survey by Westpac Bank 60% of people are planning to buy a property in the next five years.

Yet the heartbreaking battle facing first home buyers is getting harder with rents skyrocketing, and last week we reported My Housing Market’s end-of-April figures showing that property prices have continued rising around Australia – that’s 16 months in a row now.

In today's Property Insider chat with Dr Andrew Wilson, we discuss the latest My Housing Market Rental Report as well as some of the latest data that gives us a clue to what's ahead for the economy, interest rates and our housing markets.

Still no sustained relief likely for tenants

Watch this week’s Property Insiders chat as Dr Andrew Wilson discusses the latest My Housing Rental Report, which showed mixed results over April, with vacancy rates for both houses and units easing in most capitals, although generally remaining very low and continuing to favour landlords.

While holiday distractions over April may have contributed to lower rental demand over the last month, any sustained relief for tenants will prove to be short-lived.

A vacancy rate of around 2% is considered a balanced market where there is a sufficient supply of rental accommodation to satisfy tenants’ needs, and as you can see from the tables below, we are far from this situation at present, suggesting the rental crisis will continue for some time, with the minimal extra supply on the horizon there is no relief in sight.

Affordability constraints mean many tenants are now looking at renting apartments, but as you can see from the table below, even though there has been minimal rental growth in the disrupted month of April (with Easter and school holidays interrupting the normal markets), rental growth over the last 12 months has been very strong in almost all our capital cities.

Demand for rental accommodation remains high, and even though there seems to be an uplift in group households, according to the ABS this was far outpaced by a rise in lone and two-people households.

At the same time, strong net overseas migration is creating significant demand for rental accommodation in our capital cities.

March retail sales down

Watch this week's Property Insider video as Dr. Andrew Wilson and I discuss the latest retail sales figures that fell 0.4% over the last month.

While sluggish consumption growth will be some comfort to the RBA that they are making progress in reducing excess demand, nominal retail spending is still well above trend, with much of this reflecting higher inflation over the past few years.

Over the last month, falling household goods spending has been offset by higher spending on food.

Home building approvals rise

In this week's Property Insider chat Dr. Andrew Wilson and I discuss how home building approvals have risen 3.7% over March, following a 3.5% fall in February.

As always, building approvals for units are more volatile, but overall, the annual levels of building approval are chronically depressed, with the quarterly trend falling.

Despite the will of governments to get home-building activity moving, there are still too many obstacles in our way.

Chronic tradie shortages, planning and licensing delays, draconian industrial relations changes, material cost inflation, inefficient regulation, unfeasible lending practices and risk allocation are making projects unsustainable.

In simple terms, we're just not building enough accommodation to have Australians meaning there is no indie site to the housing crisis we are experiencing.

As you can see from the following chart, building approvals are significantly down from their peak in 2016.

Stable auction results to begin May

With the April holiday season now concluded, capital city auction markets have continued to report generally stable results to begin May, although higher listings remain a feature of the Autumn market, particularly in Sydney and Melbourne.

Adelaide had the strongest auction clearance rate of 77.6%.

Auction clearance results for the other capitals were:- Melbourne - 63.4%; Brisbane - 59.1%; Sydney - 74.9% and Canberra - 50.0%.

The national weekend auction market reported a clearance rate of 65.0% which was higher than the 62.8% reported over the previous weekend – but again well below the 79.7% recorded over the same weekend last year.

National auction numbers were again higher at the weekend with 1977 listings versus the previous weekend's 1730, and still significantly above the 1441 listed over the same weekend last year.

Weekend auction markets continue to produce relatively steady results although clearance rates are likely to continue to track well below the near boomtime rates recorded over late autumn last year.

- Also read:Renter’s Nightmare: Are Australia’s Rental Markets Spiralling Out of Control? | Property Insiders [Video]

- Also read:Latest Asking Prices State by State | April Total Housing Listings fell by 6.4%

- Also read:This week’s Australian Property Market Update – Latest Data, State by State May 7th 2024

- Also read:Auction clearance results May 4th – Stable Auction Results to Begin May

- Also read:The latest Corelogic Rental Market Report