Key takeaways

Rental affordability has deteriorated significantly, with households now spending a record 33.1% of income on rent after years of sustained increases.

The core issue remains a structural undersupply of rental stock, with listings well below normal levels and vacancy rates sitting near historic lows.

Rent growth has reaccelerated, rising both quarterly and annually.

Tenants are adapting by shifting to more affordable options such as units and regional areas, driving stronger growth in these segments.

Without a meaningful increase in housing supply, rental pressures will persist and continue feeding into inflation and broader economic challenges

Australian renters are spending a record share of their gross median household income on housing costs, as a chronic shortage of rental stock drives rents higher across the country.

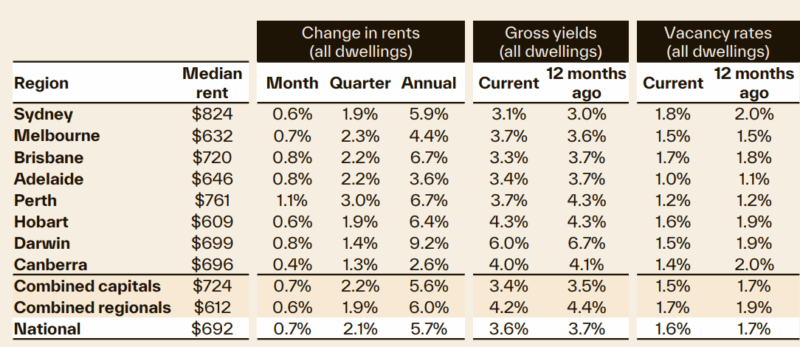

Cotality's Rental Review Q1 2026 shows national dwelling rents increased 2.1% over the three months to March, up from a 1.2% increase in Q4 2025, indicating a pickup in momentum from the cyclical low of 0.9% recorded in Q3 2025.

The reacceleration also extends to annual terms, with national rents 5.7% higher than a year ago, up from 5.2% in Q4 and a mid-2025 trough of 3.4%.

Rental affordability has deteriorated sharply as a result, as households commit a record 33.1% of gross median household income to rent, compared with a recent low of 26.2% recorded in September 2020.

Five years of sustained rental growth had added an estimated $202 per week to the typical Australian household rent commitment.

Rent growth had moderated through much of 2024 and into mid-2025, but there’s been a lack of supply to meet the demand, which is placing immense pressure on the rental market.

Vacancy rates remain very tight nationally and the volume of available rental properties is well below where it needs to be.

Until supply catches up meaningfully with demand, rental growth is likely to stay elevated.

Supply deficit underpins market tightness

Rental listings nationally are around 18% below their five-year average, with the shortage most acute in Sydney and Melbourne, where available stock is 27.4% and 21.0% below long-term levels respectively.

Every capital city recorded a vacancy rate below 2.0% in the March quarter with the national rate of 1.6% half the 3.2% average for the five years to March 2021.

Adelaide and Perth remain the most constrained markets, with vacancy rates of 1.0% and 1.2% respectively.

Low vacancy rates and a shortage of available listings have persisted across most capital cities for several years now, and there is little in the current data to suggest conditions are improving.

When vacancy rates fall to 1.5% or less it leaves renters with very little negotiating power and fewer options.

It means renters have to consider alternate options such as share houses, moving to a new area or back in with family.

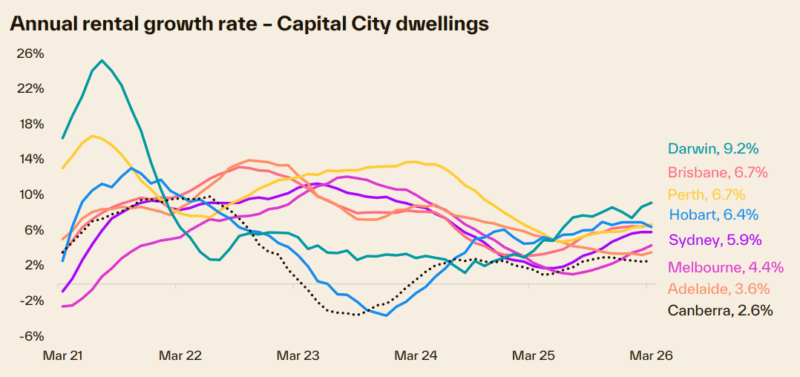

Darwin leads growth as Sydney remains country’s most expensive market

Darwin recorded the largest annual rental growth surge of any capital city, with rents rising 9.2% over the year to March to reach $699 per week.

Perth and Brisbane followed, each recording growth of 6.7% over the same period.

- Also read:Australia’s jobs boom raises the risk of another interest rate rise | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:National Weekly Auction Report – July 25th 2026 | Chilly July Auction Market Concludes with Some Resilient Signs

- Also read:Perth housing market update | July 2026

Sydney remained the most expensive rental market nationally, with the median rent up 5.9% over the year to $824 per week in March 2026.

Melbourne recorded the slowest growth of the mainland capitals, at 4.4% annually, with the median dwelling rent of $632 per week the lowest of any mainland capital, only marginally ahead of Hobart at $609 per week.

Affordability pushes regional markets and units up

Rental growth in regional markets was marginally stronger than the combined capitals over the year to March, at 6.0% versus 5.6%.

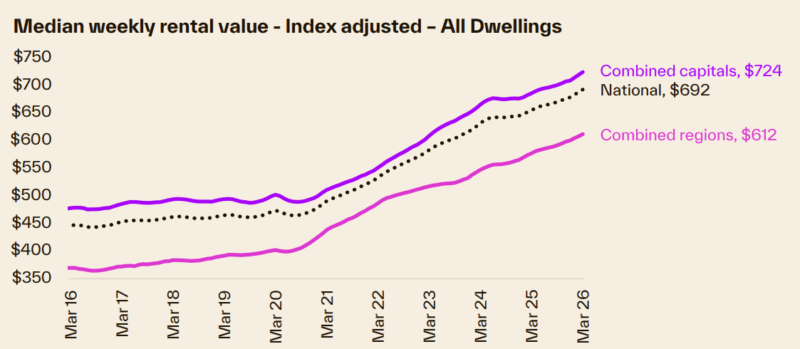

The regional median rent of $612 per week remains considerably below the $724 per week recorded across the combined capitals and vacancy rates in regional areas were slightly higher at 1.9%, compared with 1.7% for the capital cities.

Unit rents have outpaced house rents consistently over the past five years, increasing 46.9% since March 2021 compared with 39.0% for houses.

The stronger unit growth was in part a recovery from the sharp decline in unit rents recorded at the onset of the pandemic.

However, the trend has continued more recently, with unit rents rising 2.5% over the three months to March compared with 2.0% for houses.

The stronger relative growth in unit rents is now less about catch-up and more consistent with renters seeking affordable options as overall rent levels remain elevated.

As total weekly rent prices continue to increase, we’ve seen demand shift toward more accessible price points, and units are bearing the brunt of that competition.

Further growth expected as rental pressure remains

Persistently low vacancy rates and limited new supply entering the market is expected to apply pressure on the rental market in the short term.

While rental affordability, measured as the share of income committed to rent, is at its most stretched level on record, market conditions mean there is unlikely to be any material easing without a significant increase in rental housing supply.

The reacceleration in market rents also carries implications for headline inflation as rent growth is yet to fully flow through to reported inflation figures.

The rental market continues to exert upward pressure on the broader economy in ways that extend beyond housing.

With vacancy rates showing little sign of meaningful improvement and market rents reaccelerating, the flow on impact rents have to CPI data will remain an important factor for policymakers to navigate in the months ahead.