Key takeaways

Building approvals are improving, but the recovery remains fragile. National approvals rose 2.4% in June, driven largely by a 17.8% jump in apartments.

Australia is still building far fewer homes than a decade ago. Capital city dwelling approvals remain 23.3% below their 2016 peak, while unit approvals are down 41.3%.

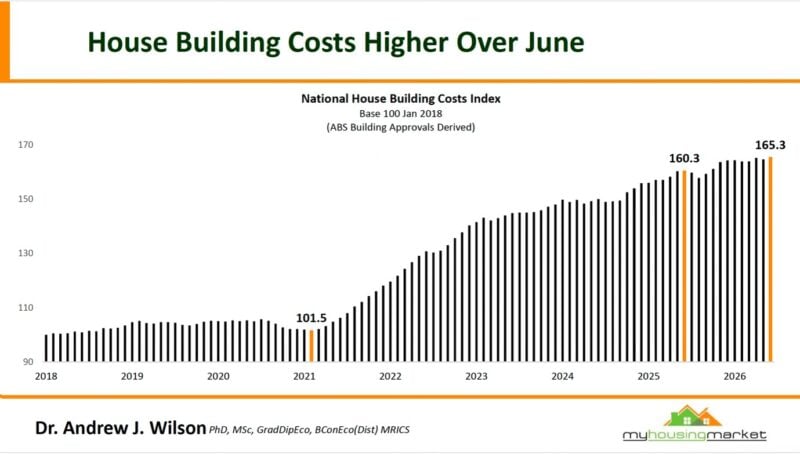

Construction costs remain a major barrier to new supply. The estimated cost of building a house has risen around 65% since the beginning of 2018.

More approvals won’t solve the housing shortage if projects aren’t financially viable. High land, construction, financing, tax and compliance costs mean many approved developments may never be built.

The housing shortage continues to favour quality established properties. Investors should focus on areas with strong demand, scarce land and limited economically viable new supply

Australia desperately needs more homes, and the latest building approval figures appear to offer some welcome news.

Approvals increased in June, apartment approvals rebounded strongly, and the quarterly trend is finally moving higher. However, another set of figures tells us why Australia’s housing shortage could remain with us for years.

The cost of building a new house has risen by around 65 per cent since the beginning of 2018, while apartment development remains well below the levels achieved a decade ago.

This creates a difficult contradiction for governments, developers and homebuyers. We may be approving more homes, but the economics of actually building them remain challenging.

In this week’s Property Insiders, Dr Andrew Wilson and I look behind the encouraging headline numbers to examine whether Australia is genuinely beginning to build its way out of the housing shortage.

Home building approvals rise in June

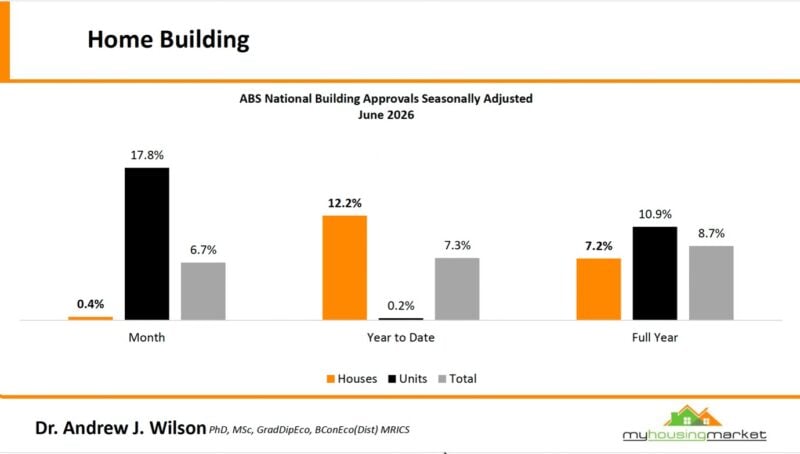

The latest Australian Bureau of Statistics figures show national home building approvals increased by 2.4 per cent in June, partially reversing the 6.7 per cent fall recorded in May.

Watch this week's Property Insider video as Dr Andrew Wilson explains how the improvement was led by the notoriously volatile apartment sector, where approvals jumped by 17.8 per cent over the month. Detached house approvals recorded a much more modest increase of 0.4 per cent.

That distinction matters because monthly apartment approvals can move sharply when one or two large projects enter the data. A strong result in a single month doesn’t necessarily indicate the beginning of a sustained construction recovery.

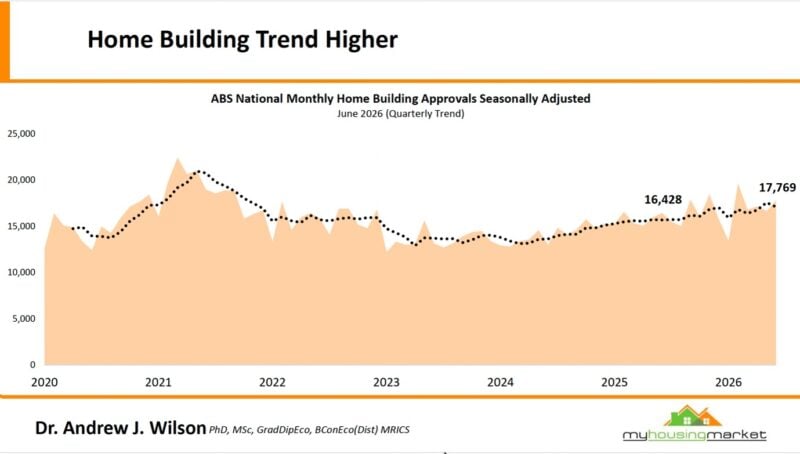

Even so, the broader trend is becoming more encouraging.

The quarterly trend in total approvals increased from 16,428 dwellings to 17,769, with unit approvals rising from 9,178 to 10,631. House approvals slipped slightly over the same period, from 7,250 to 7,138.

Year-to-date, total national approvals were 7.3 per cent higher, while the annual figure was up 8.7 per cent.

These numbers suggest the development pipeline is gradually improving, although Australia still has a long way to go before approvals are running at the level required to accommodate population growth and replace the housing we have failed to build over recent years.

Queensland leads the recovery

The improvement in building activity remains uneven across the country.

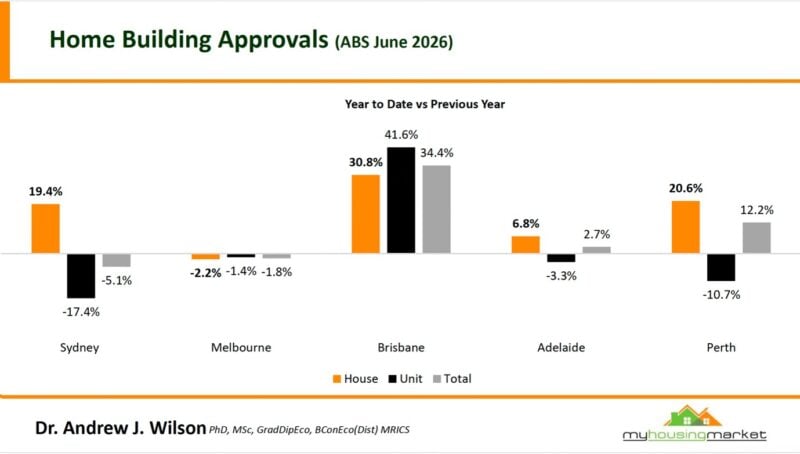

Queensland was the standout performer, with total approvals rising by 33.4 per cent compared with the previous year. Brisbane recorded 17,963 approvals year-to-date, including 6,951 houses and 10,850 units.

Brisbane’s total approvals were 34.4 per cent higher than a year earlier, with house approvals up 30.8 per cent and unit approvals increasing by 41.6 per cent.

Perth also recorded growth, with total approvals 12.2 per cent higher year-on-year. House approvals increased by 20.6 per cent, although apartment approvals remained 10.7 per cent lower.

Sydney’s result was more complicated. Total approvals were 5.1 per cent lower, but the composition changed significantly. House approvals fell by 17.4 per cent while apartment approvals increased by 19.4 per cent.

Melbourne continued to underperform, with total approvals down 1.8 per cent compared with the previous year. House approvals declined by 2.2 per cent and unit approvals fell by 1.4 per cent.

This is concerning because Melbourne has strong long-term population growth and arguably needs a significant increase in new housing. Yet developers remain constrained by high construction costs, planning delays, taxes, financing costs and weak project feasibility.

Adelaide’s total approvals declined by 3.3 per cent, despite a 6.8 per cent increase in house approvals, as unit approvals fell.

Approvals remain well below their previous peak

The longer-term figures put the recent improvement into perspective.

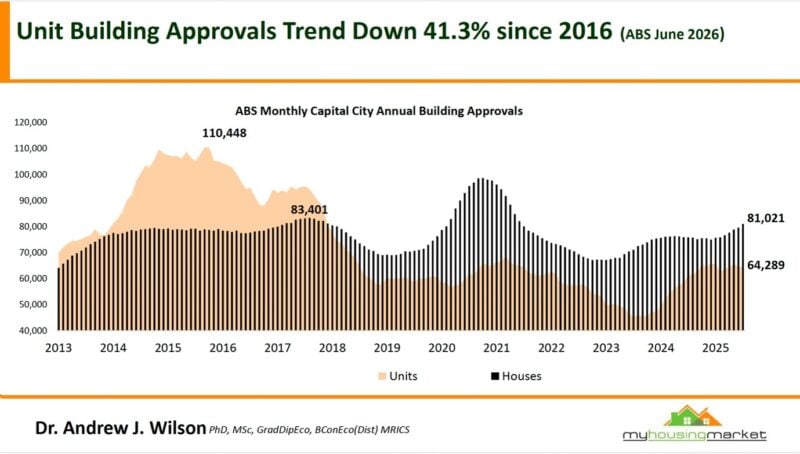

Annual capital city dwelling approvals peaked at 189,409 in 2016. They are now running at approximately 145,310, which is 23.3 per cent below that peak.

The shortfall is particularly pronounced in the apartment market.

Capital city unit approvals peaked at 110,448 in 2016 and are now around 64,289, representing a fall of 41.3 per cent. House approvals have held up better and are currently running at around 81,021.

Australia’s major housing shortage is concentrated in our largest cities, where land is scarce and expensive. These cities need more well-located, medium and higher-density accommodation, yet this is precisely the sector where building activity has fallen most sharply.

For all the discussion about increasing density, changing planning rules and setting ambitious housing targets, developers will only proceed when projects are financially viable.

As we often say when discussing this issue on our weekly Property Insider show. planning approval does not guarantee that a project will be built.

Building costs are rising again

Watch this week's Property Insider video as Dr Wilson discusses his house building cost index, derived from ABS building approval data, which increased to 165.3 in June, compared with a base of 100 at the beginning of 2018.

- Also read:Australia Needs More Property, but Builders Can’t Make the Numbers | Property Insiders

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:This week’s Australian Property Market Update – Latest Data, State by State August 11th 2026

- Also read:National Weekly Auction Report – August 8th 2026 | Home Auction Markets Rising

- Also read:National Property Listings Surge to Highest Level in Over a Year | Latest SQM Listing Data

In other words, the estimated cost of building a house has increased by roughly 65 per cent in a little over eight years.

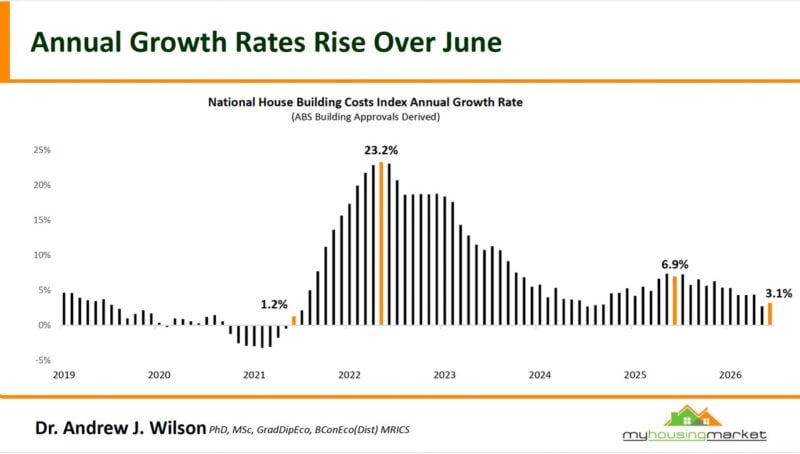

Annual construction cost growth surged to 23.2 per cent during the pandemic-era building boom as supply chain disruptions, labour shortages and government stimulus placed extraordinary pressure on the industry.

That rate of growth eventually eased, but building costs won’t return to their previous levels. They simply keep rising more slowly.

Annual house-building cost growth has now increased to 3.1 per cent. That is well below the pandemic peak but still adds to an already elevated cost base.

As you will hear when you watch Andrew Wilson's explanation, a lower inflation rate doesn’t mean building has become cheaper. It means already-high costs are increasing at a slower pace, and the latest figures suggest that pace may be accelerating again.

Builders also face labour shortages, rising insurance costs, stricter building standards and higher compliance expenses.

Developers must contend with expensive land, government charges, infrastructure contributions and the cost of financing a project through a lengthy approval and construction period.

The completed dwelling must then be sold at a sufficiently high price to compensate for all those costs and risks.

The fact is that in many locations, particularly for medium-density and apartment projects, prospective buyers are unwilling or unable to pay the price required to make the development viable.

Why the housing targets remain difficult to achieve

Australia’s housing debate tends to focus on how many homes governments want built, but targets don’t build houses.

Private developers and construction companies deliver most new housing, and they can’t undertake projects that are commercially unviable.

This helps explain why the gap between approvals and completions can become substantial. Some projects receive approval but are deferred, redesigned or abandoned because the anticipated returns no longer justify the risk.

Higher construction costs also reduce the number of homes that can be delivered within affordable price ranges. Even when new dwellings proceed, they may need to be sold at prices beyond the reach of many households.

Governments could improve the situation by streamlining planning, reducing unnecessary delays, releasing suitable land with infrastructure in place and reconsidering the taxes and charges imposed on new housing.

However, we also need to recognise that planning reform alone will not solve the shortage. Faster approval of an unviable project simply produces an unviable project more quickly.

Australia needs policies that address feasibility, construction capacity and productivity, as well as planning.

What does this mean for property investors?

For property investors, the latest figures reinforce a trend we have discussed for some time.

Australia is unlikely to produce enough well-located housing to satisfy demand in the foreseeable future. Population growth, smaller households and the concentration of employment in our major cities will continue to place pressure on established housing markets.

This doesn’t mean every property will perform well. Markets with large pipelines of generic, investor-grade apartments can still experience periods of oversupply, while properties in areas with weak owner-occupier demand may underperform despite a national housing shortage.

Strategic investors should focus on locations where demand is deep and diverse, land is genuinely scarce, household incomes are rising and new supply is difficult to deliver economically.

In my view, the construction cost problem strengthens the investment case for established properties with strong land components in proven suburbs. Replacement costs are rising, which can provide an underlying floor beneath the value of existing quality housing.

At the same time, higher costs will make renovation and development strategies more difficult. Investors considering these approaches need realistic budgets, larger contingencies and a clear understanding of local end values.

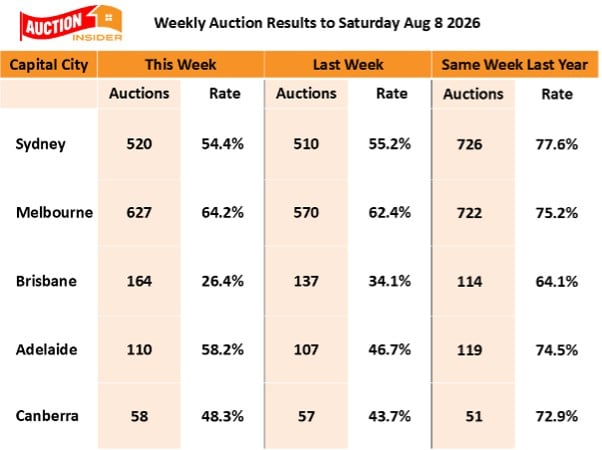

Auction markets show tentative improvement

Auction markets generally produced better results over the past week, although conditions remain subdued and clearance rates are well below those recorded at the same time last year.

The national weekend auction market reported an average clearance rate of 50.3% over the past week, which was again higher than the 48.4% reported over the previous week but again well below the 72.9% reported over the same week last year.

Auction markets continue to show early signs of a pre-spring selling revival typical of August - but from a low base, with all eyes now shifting to the RBA decision on interest rates this coming week.

The bottom line

The June approval figures are a step in the right direction, particularly the improvement in apartment approvals and the stronger quarterly trend.

However, Australia remains well below previous levels of residential construction, while the cost of delivering new housing has risen dramatically.

Approvals can signal future supply, but they do not guarantee that homes will be built. Until construction becomes more financially viable, housing completions are likely to remain below what our growing population requires.

That means the housing shortage will continue to influence rents, affordability and property prices, particularly in established locations where demand is strong and new supply is difficult to create.