Key takeaways

The Federal Government is fast-tracking the expanded Home Guarantee Scheme to October 1, right before the Spring selling season.

Buyer confidence and demand surge will collide with already rising clearance rates and prices.

Treasury predicts only a 0.5% price impact over six years, but real-world dynamics suggest much stronger near-term heat.

Demand spikes matter more than averages — especially in supply-constrained markets at entry-level price points.

The policy will help some Australians buy sooner, but it’s not an affordability solution.

Instead, it risks pushing property values higher, worsening the challenge for the next wave of buyers.

Until Australia tackles supply properly, demand-side subsidies will just add fuel to an already hot market.

Rates are easing. Buyer and seller confidence is rising. Auction clearance rates are humming.

And now, the Federal Government has decided to throw additional demand into the mix by fast-tracking its expanded Home Guarantee Scheme to October 1.

Income caps are being removed, property caps are being lifted (to $1.5m in Sydney, $950k in Melbourne, $1m in Brisbane), and more buyers will be able to purchase with just a 5% deposit and no LMI because the government guarantees up to 15% of the loan.

Let’s be blunt: for the current wave of first-home buyers, that’s exciting news.

But for the housing system as a whole, it’s a familiar story - more demand meets constrained supply, prices ratchet higher, and affordability worsens for the next wave of buyers.

We’ve seen how this plays out before.

What exactly changed, and why it matters right now

Bringing the start date forward to October 1 means this demand pulse hits the Spring selling season, already the most active period of the year, just as borrowing capacity improves with falling rates and rising buyer and seller confidence.

While previously the scheme allowed 50,000 participants, the Treasury estimates that the adjustments to the scheme will see an extra 20,000 first-home buyer families taking advantage of the scheme, meaning 70,000 first-home buyers are set to flood the market in the first year.

Treasury says the overall price impact will be “around ½% after six years,” but even they acknowledge tens of thousands more buyers will transact earlier (estimating about +20,000 guarantees in year one).

As I see it, prices will rise significantly more than that because timing matters more than the long-run average.

It's more likely that at the lower end of the market prices will increase by up to 10% over the next year. Concentrated demand spikes move prices at the margin, especially at entry price points of our housing markets.

Auction clearance rates are already at their strongest levels in more than a year, holding around the low- to mid-70s on preliminary reads - firm territory by any standard - and national price indices have been grinding higher through 2025 on tight stock and the prospect of easing monetary policy.

Layering a deposit shortcut onto that backdrop doesn’t cool a market; it stokes it!

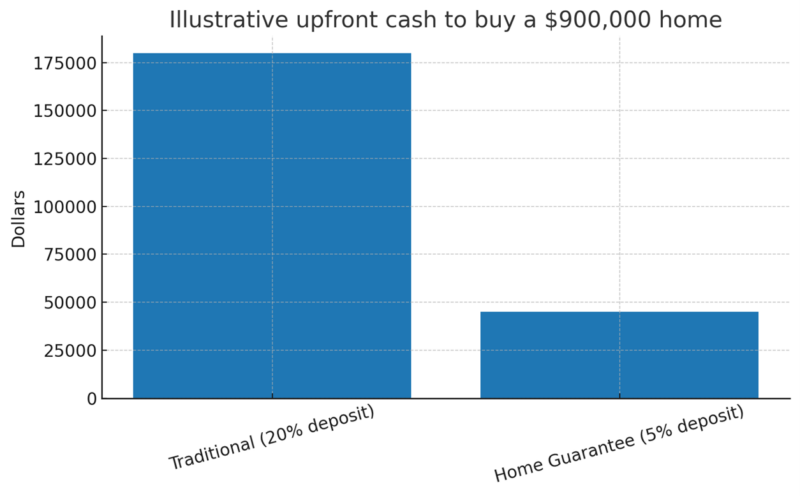

The following chart compares a traditional 20% deposit with the 5% deposit path under the scheme (which also avoids LMI - often tens of thousands, with reported savings up to about $42k in some cases).

This is precisely why the policy is politically popular: it materially lowers the cash barrier to entry.

The economics: demand cheques cash out as higher prices

All economists agree that demand-side subsidies push up prices when supply can't respond quickly.

It wasn't that long ago, in the early days of the COVID pandemic, that the HomeBuilder incentive and first-time buyer grants pushed up demand and property prices.

The pattern repeats itself: policy changes occur, demand increases, prices rise, and affordability for future entrants deteriorates.

Independent think-tanks have called out the same dynamic.

Grattan Institute, for example, warned years ago that expanding deposit guarantees risks lifting prices and benefiting sellers more than buyers, without materially improving ownership rates.

That was for a smaller scheme; today’s expansion is larger and faster.

History rhymes: three case studies

1. FHOG (2000) and the 2008–09 “boost”

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

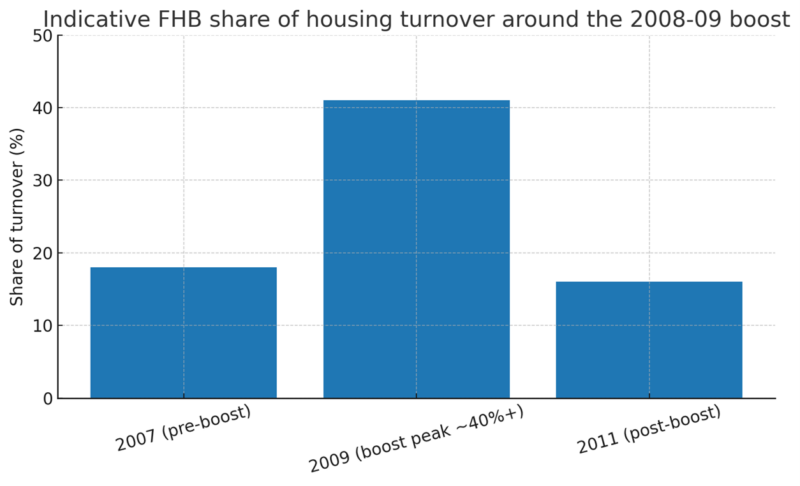

Western Australia saw a 91% month-on-month jump in first-home buyer commitments when the initial 2000 grant kicked in—classic demand spike. Nationally, during the 2008–09 boost, first-home buyers climbed to 40%+ of turnover, and prices at the lower end rose sharply as new entrants bid against each other. When the boost rolled off, first-home buyer activity slumped. That’s not “solving affordability”; that’s bringing forward demand.

2. COVID-era HomeBuilder and state grants (2020–21)

First-home buyer activity surged from mid-2020, and prices followed - exactly what you’d expect when you mix record-low rates with cash incentives. The RBA later noted these subsidies made housing less affordable overall by elevating prices.

3. Earlier Home Guarantee iterations (2019–2023)

Even at a smaller scale (10–50k places), take-up rose as prices climbed, and analysts cautioned that expanding places and loosening eligibility would risk bidding up entry-level stock. We’re now removing income caps and lifting price caps significantly; expecting a neutral price effect in Q4 is optimistic.

Why the current timing will amplify the effect

There are a number of reasons why this policy change will add fuel to the flames of our housing markets.

- Supply is still tight. ABS new house building approvals have hovered near decade lows across the cycle; there was an uptick in June 2025, but infill and medium-density projects still face cost and planning headwinds, meaning there will not be a significant increase in housing supply for some time yet.

- Spring is when buyers show up. Auction clearance rates are already in the 70s, signalling a seller’s market; now add a deposit shortcut and you mint more qualified bidders now.

- Price caps were lifted materially. Allowing Sydney purchases up to $1.5 million captures a significant swathe of family-grade stock, not just tiny entry-level units. And it's much the same in Melbourne, where the $950,000 price cap is higher than the median price. That broadens the competitive impact beyond the very bottom of the market.

Put it all together and you have a policy shock that accentuates an existing upswing.

Winners and losers

As always, there will be winners and losers.

Winners (now):

- Current first-home buyers with stable incomes but thin deposits will benefit. The scheme meaningfully shrinks the cash they require to get into the property market, and many will be able to borrow the $50,000 or so deposit required from the bank of mum and dad.

- Vendors at the affordable end. With more financed bidders, more competitive auctions, and stronger underbidders, this will likely become an established homeowner grant.

Losers (later):

- Next year’s first-home buyers. Today’s support becomes tomorrow’s higher prices. In my mind, Treasury’s six-year, ½% % figure understates the near-term, segment-specific heat where the policy bites (entry-level houses/units in supply-constrained suburbs).

- Household balance sheets taking on 95% LVR loans in a world where rates can rise again are a risk. Several industry voices have cautioned about the risk of thin equity buffers, particularly if prices wobble. I don't like seeing people take on such significant debt if they haven't managed to develop a savings discipline.

The structural fix is still supply

You don’t fix affordability with handouts to buyers. You fix it by building more of the right homes, in the right places, faster. That means:

- Streamlined planning pathways for well-located medium-density development in our middle ring suburbs,

- Stable building code settings (the government has just announced a pause on non-essential NCC changes to 2029),

- Infrastructure sequencing and funding that brings shovel-ready sites forward, and

- Targeted finance access for small-to-medium developers who actually supply infill stock.

To their credit, ministers have flagged clearing backlogs of environmentally assessed projects.

Even so, none of that lands by October. The demand arrives immediately; the supply arrives slowly. That’s the mismatch.

What we’re telling clients at Metropole

- Expect a busier Spring, especially in Brisbane for sub-$1m to $1.2m, Melbourne family suburbs for $900k–$1.2m, and Sydney's middle rings for $1.2m–$1.6m. Those bands align with lifted caps and typical first-home budgets.

- Investors - the window of opportunity is closing before the rush. Have a wealth discovery chat with wealth strategists at Metropole.

Whether you’re buying your first home, adding to your investment portfolio, or simply want a strategy to make the most of this unique window, we can help you:

- Create a personalised strategic plan that matches your goals and risk profile

- Identify high-performing opportunities in strong, stable markets

- Navigate the property cycle with confidence and clarity

Click here now to book your Wealth Discovery Chat

First-home buyers: yes, this can bring forward your purchase, but understand what you’re trading - low deposit = higher LVR risk. Be location-first, quality-first: buy scarcity (land value, streetscape, school zones), not “cheap”.

The bottom line

Bringing the Home Guarantee expansion forward to October 1 will help some Australians buy sooner - and that’s terrific for them.

But it’s not an affordability fix. History tells us demand-side sweeteners inflate prices, especially when supply is constrained.

We’ll likely push values to new highs through late 2025, handing an even steeper entry hurdle to the next cohort of first-home buyers.

If the aim is genuine affordability, supply is the lever.

Until we treat it that way, policies like this will keep pouring fuel on an already hot market.