Key takeaways

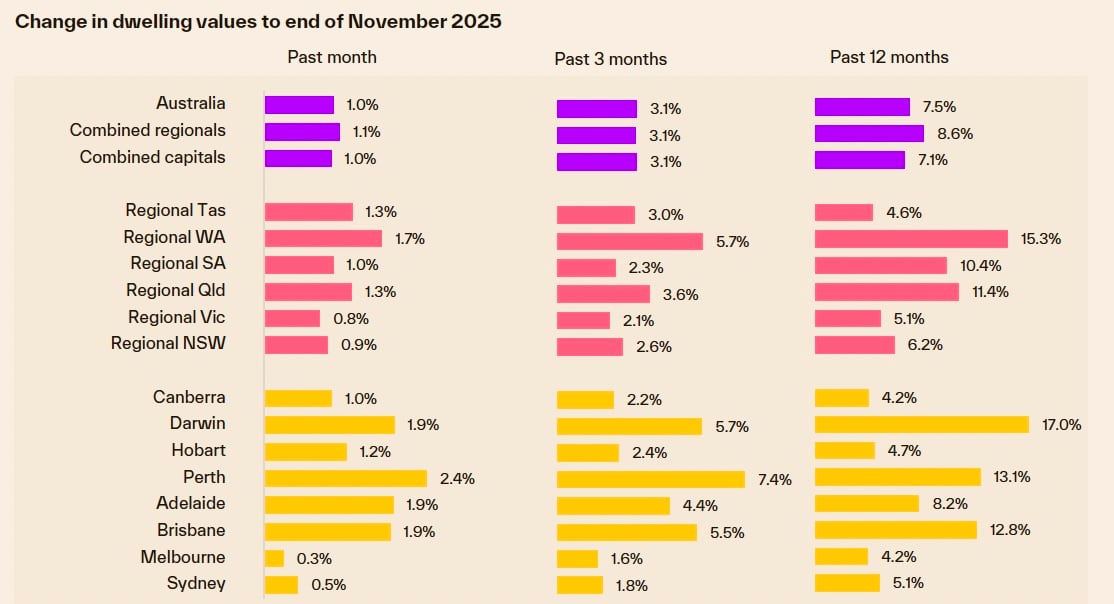

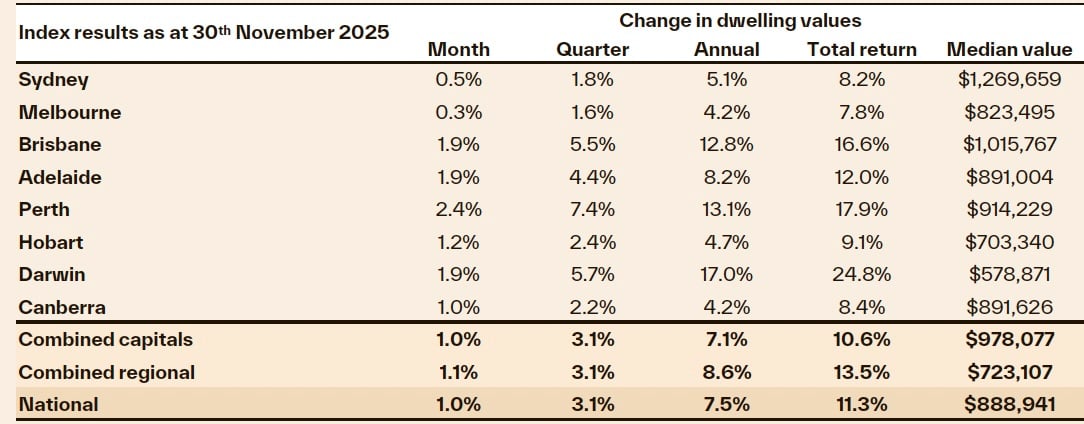

National home values rose 1.0% in November, marking the third consecutive month of strong growth, though the pace is easing from October’s 1.1% gain.

Mid-sized capitals are outperforming, with Perth leading at 2.4% growth, while Sydney and Melbourne lag at 0.5% and 0.3% amid affordability constraints.

Affordability and rate pressures loom, as record-high dwelling value-to-income ratios and expectations of prolonged rate holds signal headwinds for housing sentiment and credit access.

Cotality’s national Home Value Index rose another 1.0% in November, marking the third month in a row where Australian home values have increased by one per cent or more.

However, the pace of growth is moderating, coming down from 1.1% in October.

The headline growth figure was weighed down by Australia’s two largest cities, with Sydney values rising 0.5% in November and Melbourne values up 0.3%.

Every other capital city recorded a rise of at least 1.0% through the month, led by Perth with a solid 2.4% surge in values.

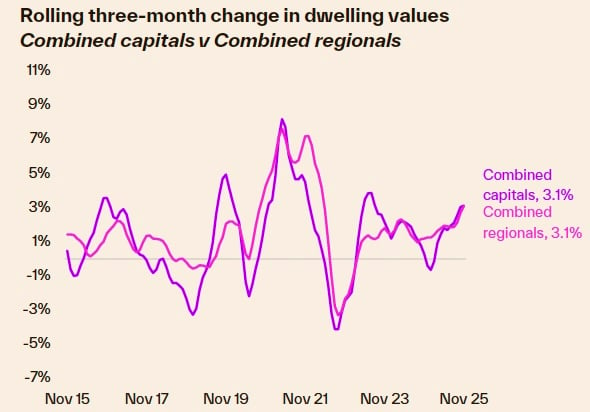

Growth in home values across the mid-sized capitals is once again diverging from the larger cities - a similar trend to the one seen in late 2023 and 2024.

The skew towards the mid-sized capitals is especially evident in Perth, where listings are holding more than 40% below average, buyer demand is elevated and the 2.4% monthly rise in dwelling values has added just over $21,000 to the median in November, roughly $5,000/week.

A lower monthly gain in Sydney, at 0.5%, could be reflective of affordability constraints putting a ceiling on growth .

Sydney has a smaller supply deficit, with listings tracking 2.2% below the five-year average for this time of the year.

This is compared with the capital city benchmark, where listings are about 16% below average.

While most markets gained price momentum through spring, Sydney’s monthly growth rate looks to have peaked at 0.9% in August.

The subtle easing in the headline result comes as auction clearance rates have trended lower since peaking in mid-September, falling below the decade average by mid-November.

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – April 2026

- Also read:National Weekly Auction Report – April 11th 2026 | Auction Markets Steady After Easter with School Holiday Listings

- Also read:Latest Property Asking Prices State by State | National Listings Rise in March

- Also read:Rents Surge Again as Interest Rates Bite – What Happens Next?| | Property Insiders

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

Both Sydney and Melbourne have seen clearance rates hold in the low 60% range through the second half of November.

Record levels of housing unaffordability are another factor, with affordability metrics to the September quarter showing a record high in the national dwelling value to household income ratio (the median dwelling value is 8.2 times higher than the annual pre-tax household income) and near record levels of income required to service a mortgage at the median value (45.0%).

Another demand-side factor that might weigh on housing growth going forward is the rebound in inflation as well as the now widely held expectation that interest rates won't be cut further anytime soon.

With inflation once again above the RBA’s target range and rates potentially on hold for the foreseeable future, it's likely housing sentiment will suffer.

With housing affordability already stretched and worsening, it stands to reason that fewer borrowers will be able to access credit as serviceability barriers become more prominent.

We can already see the flow through effect from such stretched affordability and serviceability measures, with growth in housing values skewed towards lower price points of the market.

Over the past three months, most of the state capitals have seen values across the lower quartile of the market rising the fastest.

Melbourne, where housing affordability isn’t quite as stretched, is the one exception, with the city’s broad middle of the market is seeing the fastest lift in values.

The impacts of the recent policy announcement from APRA to limit high debt-to-income (DTI) ratio loans to 20% of new lending will also be limited, as the majority of recent mortgage originations remain significantly below a DTI of six or more.

This new credit policy won't be implemented until February next year, but even then, it's likely to only affect the margins of borrowing activity