Australia’s COVID-induced whirlwind love affair with the country’s hottest regional cities has run its course with values declining sharply as vendor discounts climb and days on market blow out.

CoreLogic’s Regional Market Update, which examines Australia’s 25 largest non-capital city regions, shows 13 areas recorded an increase in house values over the year to January 2023, down from 21 over the year to October 2022.

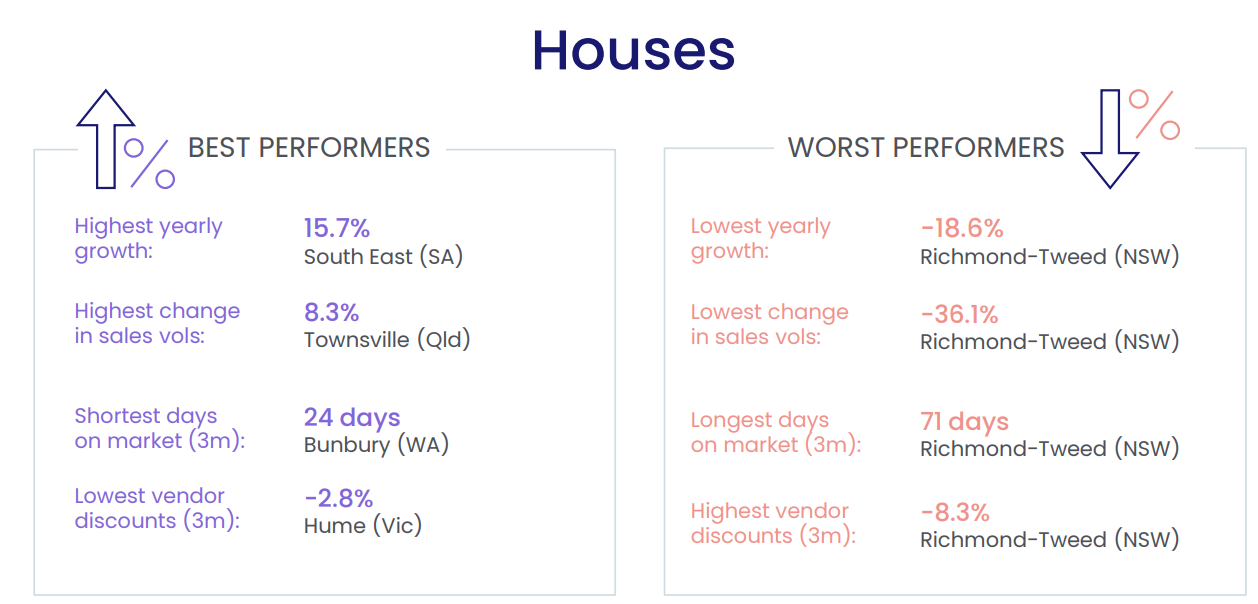

House markets

The South East region in South Australia, which includes areas such as Kangaroo Island, the Fleurieu Peninsula and the Limestone Coast, was the best-performing regional house market, with annual value growth of 15.7%.

The NSW regions of New England and North West and Riverina were not far behind, with values increasing by 11.5% and 10.1% respectively.

The country’s most popular lifestyle markets had been hardest hit by softer market conditions and rate increases.

The upmarket coastal and hinterland Richmond-Tweed region in NSW recorded the weakest performance across all metrics registering the lowest annual growth rate, the largest drop in sales volumes, the longest days on market and the highest vendor discounts.

It is unsurprising the Richmond-Tweed region recorded the strongest decline in house values and a sharp increase in other important metrics.

This was the region where values skyrocketed, with houses increasing more than 50% during COVID, taking the median house value to more than $1.1 million.

Since then much has changed with borders reopening, outbound travel returning, and workers returning to the office not to mention the overlay of nine rate rises. It’s been a swift and significant shift.

Those regional areas where double-digit annual growth rates were still occurring were predominantly areas that had emerged from a long period of subdued capital growth performance.

The COVID-boom unlocked enormous value across more affordable regional tree-change markets such as South Australia’s South East region.

The surge in demand for areas such as New England and North West was also likely due to a spillover from nearby markets such as Richmond- Tweed, where the strong migratory sea-change trend and low-interest rates priced out many lower-income households.

Richmond-Tweed’s house market value fell -18.6% in the year to January, with sales volumes down - 36.1% (in the year to November) and houses sitting on the market for 71 days.

Vendor discounting hit -8.3% for the same period.

Despite the drastic shift in market conditions, houses in the region are still up 23.7% on pre-COVID levels.

Houses in the Illawarra region, 90km south of Sydney, recorded the second lowest yearly change of - 12.6% after values surged 44.0% through the recent upswing.

Houses sold fastest in Bunbury (WA) where the median time on the market over the three months to January was 24 days.

- Also read:July Home Prices Sharply Down as Winter Freeze Bites | Latest Property Market Stats

- Also read:Australia’s jobs boom raises the risk of another interest rate rise | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:National Weekly Auction Report – July 25th 2026 | Chilly July Auction Market Concludes with Some Resilient Signs

Queensland’s Toowoomba region recorded the second fastest sales time, with a median time on the market of 28 days.

Unit markets

Across Australia’s regional unit markets, Queensland’s Cairns and Toowoomba recorded the highest annual increase in values over the 12 months to January 2023, up 17.3% and 14.1% respectively.

At the other end of the scale, Richmond-Tweed (NSW) and Geelong (Vic) recorded the largest decline in unit values over the past year, down -10.0% and -9.4% respectively.

Sales volumes lifted in only two of the 25 regional unit markets, up 19.2% in Mackay – Isaac –Whitsunday and 10.6% in Townsville in the year to November 2022.

Sales volumes fell in 23 regions, led by the Southern Highlands and Shoalhaven (-45.5%), Newcastle and Lake Macquarie (-37.3%) and Illawarra (-37.0%) regions, all located in New South Wales.

Units in Cairns took a median of 32 days to sell in the three months to January 2023, followed by Ballarat (35 days).

Richmond-Tweed and Capital Region (NSW) were the slowest-selling unit regions, with a median time on the market of 66 days and 60 days respectively.

Vendors across Richmond-Tweed are offering the largest discounts in order to secure a sale (-5.6%) while discounts of -2.4% in the Hume region (Vic) are the lowest amongst the unit markets analysed.

Regional outlook

Following the RBA’s warning that further rate hikes would be necessary to curb inflation, there was a good chance housing values will continue to trend lower, and regional areas would not be immune from softer conditions.

This is a trend we can expect to see playing out at least until interest rates top out.

With this in mind, sellers will need to be realistic about their pricing expectations, make sure they have a quality marketing campaign behind the property and be ready to expect some negotiation from buyers.

Considering some of these regional values will have only moved through a peak in the cycle more recently, it’s likely there will be a lag between buyers and sellers, and it may take some time for vendors to adjust their expectations.

While some regional markets were experiencing sharp price falls, regional market performance overall remained more resilient than capital city-dwelling markets.

Since the rate hiking cycle commenced in May, monthly value changes have averaged -0.8% across regional Australia through January, compared to -1.1% in the capitals.

This also follows a larger price boom in the regions of 41.6% compared to the combined capital increase of 25.5%.