Key takeaways

If a picture paints a thousand words, then this collection of charts should do a pretty good job of painting the landscape as it affects our economy and property markets.

Of course, Australia's economy doesn't operate in isolation, so it's important to keep track of how the economies of our major trading partners are performing.

Despite concerns around the world about recessions, Australia's economy is still growing and creating jobs but persistent inflation has caused the Reserve Bank to raise interest rates 3 times this year but this may now be at a peak.

Despite high interest rates and inflation have eaten away at the average household budget, in general Aussies have significantly more equity in their homes than they had four years ago.

Australia's residential property market is valued at $12.6 trillion, yet only $2.6 trillion worth of debt is against this large asset base. In fact 50% of homeowners don't have a mortgage against their homes.

Currently, Australia has a significant shortfall of housing, but the rising cost of construction means that most developments on the drawing board are not currently financially viable to get out of the ground.

Consumer confidence remains at very low levels and is likely to remain shaky for some time yet.

The unemployment rate is still relatively low at 4.5%, meaning Australians can feel secure about their financial futures.

The labour force participation rate is an estimate of an economy's active workforce. The participation rate has increased over the last few years, and there are currently over 337,900 jobs advertised, but nobody to fill them.

If a picture paints a thousand words, then this collection of charts should do a pretty good job of painting the landscape as it affects our economy and our property markets.

Each month the RBA summarises macroeconomic and financial market trends in Australia by providing a detailed chart pack.

World Economy

Australia's economy doesn't operate in isolation, so it's critical to keep track of how the economies of our major trading partners are performing.

Global economic conditions have shifted significantly since the start of March, with the US-Israel war on Iran becoming the most consequential new geopolitical shock in years. Oil prices have surged with the fallout especially acute in Asia, where around 80% of oil imports pass through the Strait of Hormuz, directly threatening the economies of Australia's major trading partners.

The OECD projects global growth slowing from 3.2% in 2025 to 2.9% in 2026, with US growth easing to 1.7% and China's declining to 4.4%. These forecasts were set before the Iran conflict escalated, so a downward revision in the OECD's late March update seems likely.

China's recovery remains patchy, weighed down by its ongoing property crisis and demographic headwinds — as well as the added pressure of US tariffs.

-

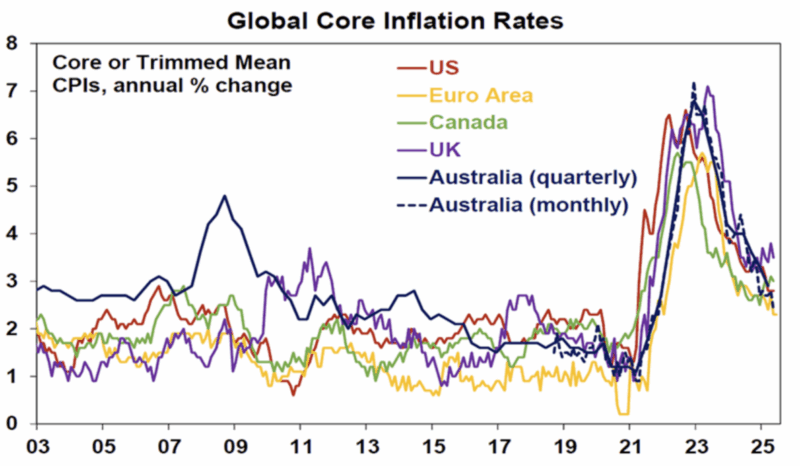

Global inflation is expected to rise modestly before beginning a gradual descent.

-

The World Bank and IMF project headline inflation to hover around 4% for the year, largely driven by energy supply disruptions and rising transport costs tied to geopolitical conflicts in the Middle East.

Australia's Economy

The Australian economy is currently navigating a significant slowdown, characterised by anemic GDP growth and persistent inflation.

While the broader economy expanded by 0.3% in the March quarter and 2.5% annually, GDP per capita is contracting. High interest rates and rising living costs are actively weighing on household budgets.

In trend terms, in April 2026:

- employment increased by 22,100 to 14,753,800 people.

- the unemployment rate remained at 4.3%.

- participation rate remained at 66.7%

- employment to population ration remained at 63.8%

- underemployment rate remained at 5.9%

- monthly hours worked increased to 2,028 million

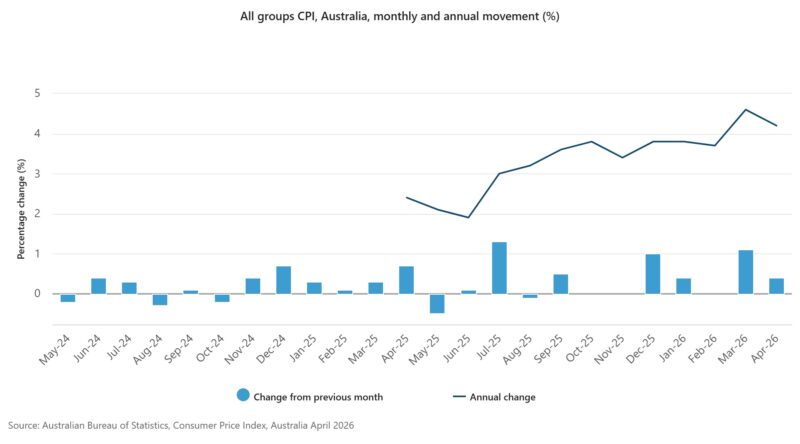

- The Consumer Price Index (CPI) rose 4.2%, down from 4.6% in the 12 months to March 2026.

- The largest contributors to annual inflation were Housing (+6.3%), Transport (+6.6%) and Food and non-alcoholic beverages (+2.8%).

Household Sector

- The following chart shows how the disposable income for Aussie households dropped last year as they grappled with rising costs, yet it has picked up over the last few months.

- Despite the Reserve Bank's best efforts to slow down household spending, we’re still spending up big on discretionary items such as clothes, restaurants, and lifestyle, defying cost of living pressures.

- According to the ABS: in April 2026, household spending:

- fell -1.1% month-on-month on a current price, seasonally adjusted basis

- rose 4.9% compared with April 2025.

- In seasonally adjusted, current price terms, household spending decreased for six of the nine spending categories. The largest decreases were in:

- transport (-4.7%)

- clothing and footwear (-2.2%)

- food (-1.3%).

- In seasonally adjusted, current price terms, household spending on goods fell 0.4% month-on-month, driven by decreased spending on:

- motoring goods

- food

- clothing and footwear.

This chart also shows how our savings ratio dropped as we kept spending our stashed cash to support our lifestyles.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State June 16th 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Why the opportunity is bigger than it looks

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- I keep a careful track of consumer confidence because it's a good leading indicator of what's ahead for our economy and property markets.

- The media's continual barrage of negative news about the economy, inflation and interest rates has a significant impact on consumer sentiment.

- While not long ago consumer confidence started bouncing up from historically low levels, it is now falling again due to rising inflation and the RBA's decision to raise interest rates, and the geopolitical problems are causing even more concern.

- While rising interest rates and inflation have eaten away at the average household budget, in general, Aussies have significantly more equity in their homes than they had before the pandemic.

- The following chart shows our net wealth position, and that our main assets are in real estate (particularly our homes) and financial assets (including our superannuation.)

- As you can see, the net wealth position of Australian households is still high since asset growth has outpaced the increased debt levels, meaning our net wealth position, while falling a little lately, is very strong.

- The Australian residential property market is valued at over $12.6 trillion, yet there is only around $2.6 trillion worth of debt against this large asset base. In fact, 50% of homeowners don't have a mortgage against their homes.

- Housing values are now languishing due to the affordability squeeze and renewed cost-of-living pressures, and I expect our property values to remains flat for much of the year. However, our markets are fragmented, and there are still some segments that are growing in value.

- Currently, Australia has a shortfall of housing, which is particularly showing up in our rental markets with historically low vacancy rates and skyrocketing rents.

- The government has a plan to build 1.2 million homes in the next 5 years, but I can't see how this will be achieved.

- The cost of residential construction has risen substantially in the last few years, in part because of the lack of available skilled labour and supply chain restrictions.

- This means the cost to build new apartments has risen to such an extent that most developments on the drawing board (see the following chart of dwelling approvals) are not currently financially viable and won’t be built until the market is prepared to pay substantially more than the current prices.

- It has been estimated that currently we have a deficit of well over 250,000 properties, something that won't be made up any time soon.

- In other words... there is no end in sight for the undersupply of dwellings. It also means that there is substantial inbuilt equity in established properties, as their replacement cost is very much higher than their current market value.

- From a peak in December 2025, the value of home lending fell 3.8% in the March quarter.

- The decline was broad based across borrower types but led by owner-occupiers (down 4.3%) ahead of investors (down 3.0%).

- This saw the investor share of lending rise to its highest rate since September 2016.

- First-home buyer lending as a proportion of owner-occupier lending reached 29.0%, slightly exceeding the decade average of 27.6%.

- This increase highlights a rise in first-home buyer activity following the expansion of the 5% deposit guarantee.

- ACT remains the strongest market for first-home buyers at 37.0%, followed by the NT (36.6%) and TAS (33.4%), with all three regions sitting significantly above their respective ten-year averages.

- Conversely, QLD and NSW continue to represent the smallest shares at 27.0%.

- Specifically, QLD's share remains below its ten-year average of 27.3%.

Business Sector

- Australian businesses are facing a continual conveyor belt of challenges, including the rising cost of living, which is dampening discretionary spending as the RBA is hell-bent on slowing our economy.

- The near-term business outlook is one of softening consumption and investment growth, tightening government expenditures, and high debt costs.

- This troubled backdrop has been reflected in low business investment, which now seems to be picking up.

Labour Markets

- Australia's labour market continues to show impressive resilience in the face of high-interest rates and unprecedented global challenges.

- The ABS has reported the following Key Statistics in trend terms, in April 2026:

- unemployment rate remained at 4.5%

- participation rate remained at 66.7%.

- employment increased to 14,753,800

- employment to population ratio remained at 63.8%.

- underemployment rate remained at 4.3%.

- monthly hours worked increased to 2,028 million.

- Australia's unemployment rate, a key indicator of labour market health, has been at very low levels for a number of months now.

- The labour force participation rate is an estimate of an economy’s active workforce. The formula is the number of people ages 16 and older who are employed or actively seeking employment, divided by the total non-institutionalized, civilian working-age population.

- The participation rate in Australia averaged 63.51% from 1978 until 2022, as you can see from the chart below the participation rate has increased over the last few years as a bigger percentage of Australians have entered or re-entered the workforce.

- As you can see from the chart below, service-related industries have had significant growth, and in particular, there has been strong growth in the healthcare, accommodation and food services industries.

- Currently, there are 337,900 jobs advertised, an increase of 2.7% from November 2025.

- Private sector vacancies were 299,000, an increase of 3.2% from November 2025.

- Public sector vacancies were 39,000, a decrease of 0.7% from November 2025.

- While national average wages have underperformed inflation over the last couple of years, meaning that “real” wages have actually fallen, we are now experiencing moderate wage increases.

Interest Rates

- Interest rate levels set by the RBA respond to changes in inflation. When rates rise, they slow economic growth and discourage borrowing, typically signalling a strong economy. On the other hand, low interest rates promote economic growth.

- The Reserve Bank has now raised interest rates three times this year, bringing them back to the peak level of last year, and while it is still possible that we will have one more interest rate rise, three of Australia's four big banks believe we're at the peak of this interest rate cycle, and rates will fall in 2027.

- Despite the sharp rise in interest rates over the last few years, home loan arrears remain at post-GFC lows, defying those property pessimists who forecast that significant levels of mortgage stress would lead to forced sales by homeowners who got over their heads in debt.