Key takeaways

If a picture paints a thousand words, then this collection of charts should do a pretty good job of painting the landscape as it affects our economy and our property markets.

Australia's economy doesn't operate in isolation, so it's important to keep track of how the economies of our major trading partners are performing.

Despite concerns around the world about recessions, Australia's economy is still growing and creating jobs but inflation has been rising, causing the Reserve Bank to raise interest rates in February .

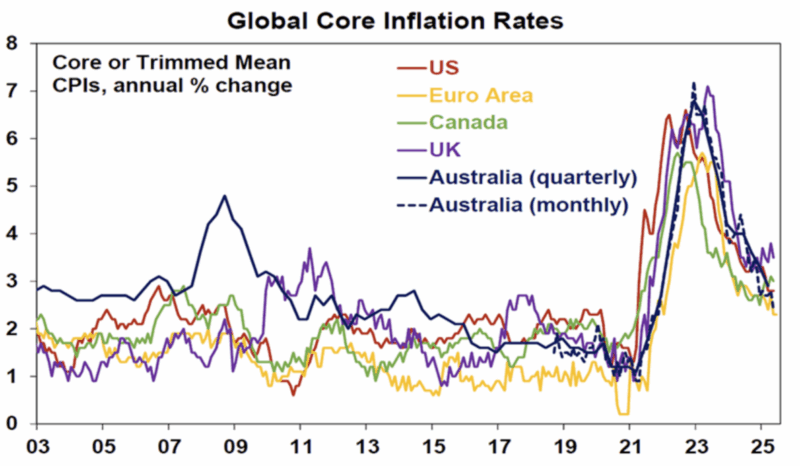

On the other hand, inflation around the world has peaked.

Despite high interest rates and inflation have eaten away at the average household budget, in general Aussies have significantly more equity in their homes than they had four years ago.

Australia's residential property market is valued at $12.3 trillion, yet only $2.5 trillion worth of debt is against this large asset base. In fact 50% of homeowners don't have a mortgage against their homes.

Currently, Australia has a significant shortfall of housing, and the cost of residential construction has risen substantially in the last few years. This means that most developments on the drawing board are not currently financially viable to get out of the ground.

Consumer confidence remains at low levels and is likely to remain shaky due to all the geo political problems in the world.

The unemployment rate is still low at 4.2%, meaning Australians can feel secure about their financial futures.

The labour force participation rate is an estimate of an economy's active workforce. The participation rate has increased over the last few years, and there are currently over 326,700 jobs advertised, but nobody to fill them.

If a picture paints a thousand words, then this collection of charts should do a pretty good job of painting the landscape as it affects our economy and our property markets.

Each month the RBA summarises macroeconomic and financial market trends in Australia by providing a detailed chart pack.

World Economy

- Australia's economy doesn't operate in isolation, so it's critical to keep track of how the economies of our major trading partners are performing.

-

Global economic growth remains subdued, with major economies like the US and EU continuing to experience slower momentum due to the legacy of high interest rates, persistent inflation above targets, and tighter financial conditions. Geopolitical risk and trade policy uncertainty (including tariff unpredictability) continue to cloud prospects for export-led growth.

-

In the United States, while the economy has shown resilience into 2026, growth has slowed and is projected to be modest (around 1.5–2.0% in 2026). Consumer demand and investment have helped avert a sharper downturn, but labour market softness and elevated pricing pressures relative to targets suggest growth is cooling.

-

Global inflation is trending downward from its mid-2022 peak, but remains elevated relative to the pre-pandemic era and shows substantial variation across countries. Advanced economies are expected to see gradual convergence back to target inflation, though risks persist from supply shocks and policy uncertainty.

Source: AMP

-

After one of the most aggressive global tightening cycles in decades, interest rates have peaked in many parts of the world. Central banks across advanced economies had pushed rates sharply higher through 2022 and 2023 in a coordinated attempt to tame post-pandemic inflation. As a result, policy rates in the US, UK, Europe, and Australia all reached levels not seen in over a decade. However, in recent months, the narrative has shifted. Inflation is trending lower -albeit stubbornly - and growth is softening, prompting several central banks to signal that the hiking cycle is over. Of course in Australia, the RBA raised rates in February.

- China’s recovery remains patchy, despite stimulus measures; its property crisis and demographic headwinds continue to weigh on consumer confidence and growth projections and of course it is experiencing the challenges of Trump's tariffs.

- Geopolitical risks remain elevated and increasing trade tensions between the US and China - adding uncertainty to global supply chains and investment flows.

- The International Monetary Fund (IMF) recently published its latest update on the state of the world economy. Global growth is projected at 3.3 percent for 2026 and 3.2 percent in 2027, revised slightly up since the October 2025 World Economic Outlook. Technology investment, fiscal and monetary support, accommodative financial conditions, and private sector adaptability offset trade policy shifts.

- Global headline inflation is expected to decline to 3.5 per cent in 2026, converging back to target earlier in advanced economies than in emerging market and developing economies.

Australia's Economy

- Growth remains modest but positive.

Australia’s GDP edged higher in the second half of 2025, with the Australian economy growing around 0.4% in the September quarter. For the full 2024-25 financial year, GDP expanded by about 1.4%, a slower pace than pre-pandemic averages but still positive. Household incomes and spending have supported growth, while business investment and construction have lagged more noticeably. - Inflation has re-accelerated, pushing up rates.

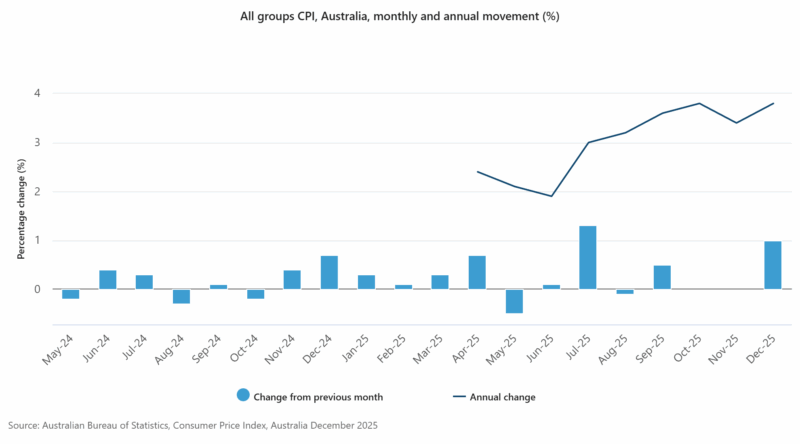

Instead of declining smoothly toward the RBA’s 2–3% target, inflation has bounced back, with the headline CPI running at 3.8% year-on-year to December 2025, up from around 3.4% in late 2025. The RBA’s preferred trimmed mean inflation measure also remains elevated at about 3.3%. Housing costs, food prices and utility bills have been the largest contributors to inflationary pressure. - With inflation sticking above target, the RBA lifted the cash rate by 25 basis points to 3.85% in early February 2026 - its first increase in over two years after a cycle of cuts in 2025. The RBA noted inflation is likely to stay above target for a while, and additional tightening can’t be ruled out if price pressures persist.

- The interest rate backdrop is now higher than many expected.

After cutting rates three times through 2025, the Reserve Bank has now reversed course in response to unexpected inflation strength. The cash rate at 3.85% is higher than typical markets were pricing just months ago, and major lenders have passed these increases into home loan rates, reducing borrowers’ capacity and pushing monthly repayments higher. - Jobs and the labour market remain a key focus.

Official unemployment sits at historically low levels, but there are signs the labour market is easing. Advertised job vacancies have declined from the peaks seen over the last couple of years, and some sectors are already moving to job cuts or hiring slowdowns as businesses adjust to higher financing costs and weaker demand. Wage growth remains moderate — not exploding, but high enough to sustain consumer spending and keep services inflation sticky. - Household finances and confidence are under pressure.

Mortgage stress is growing. Recent surveys suggest more than one-third of Australian homeowners are struggling with repayments, a trend that predates the latest rate rise but will likely worsen if rates stay elevated or rise further. This sentiment is feeding through into weaker consumer confidence and caution around big spending decisions. - Construction and dwelling investment growth have slowed sharply.

With borrowing costs higher and inflation eating into margins, residential construction growth forecasts have been cut dramatically. Industry groups warn that without policy reforms to address productivity, red tape and labour shortages, the federal government’s housing delivery targets are unlikely to be met.

In trend terms, in December 2025:

- unemployment rate decreased to 4.2%.

- participation rate remained at 66.8%.

- employment increased to 14,686,100.

- employment to population ratio remained at 64.0%.

- underemployment rate remained at 5.9%.

- monthly hours worked increased to 1,997 million.

- The Consumer Price Index (CPI) rose 3.8% in the 12 months to December 2025, up from a 3.4% rise in the 12 months to November 2025.

- The largest contributors to annual inflation over the past 12 months were Housing (+5.5%), Food and non-alcoholic beverages (+3.4%), and Recreation and culture (+4.4%).

Household Sector

- The following chart shows how the disposable income for Aussie households dropped last year as they grappled with rising costs, yet it has picked up over the last few months.

- Despite the Reserve Bank's best efforts to slow down household spending, we’re still spending up big on discretionary items such as clothes, restaurants, and lifestyle, defying cost of living pressures.

- According to the ABS: in November, household spending:

- Rose 1.0% month-on-month on a current price, seasonally adjusted basis.

- Rose 6.3% compared with November 2024.

- In seasonally adjusted, current price terms household spending increased for eight of the nine spending categories. The largest increases were in:

- furnishings and household equipment (+2.2%)

- clothing and footwear (+2.0%)

- recreation and culture (+1.7%).

- In seasonally adjusted, current price terms, household spending on goods rose 0.9% month-on-month, driven by increased spending on medicines, medical aids and therapeutic appliances, furniture, floor coverings and household goods, and goods for recreation and culture.

This chart also shows how our savings ratio dropped to below pre-pandemic levels as we kept spending our stashed cash to support our lifestyles but this is rising slowly again.

- I keep careful track of consumer confidence because it's a good leading indicator of what's ahead for our economy and property markets.

- The media's continual barrage of negative news about the economy, inflation and interest rates has a significant impact on consumer sentiment.

- While not long ago consumer confidence started bouncing up from historically low levels, it has started to fall again due to rising inflation and the RBA's decision not to lower interest rates.

- Also read:Melbourne property market forecast for 2026 & 2027 | Why the opportunity is bigger than it looks

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State May 26th 2026

- While rising interest rates and inflation have eaten away at the average household budget, in general, Aussies have significantly more equity in their homes than they had before the pandemic.

- The following chart shows our net wealth position, and that our main assets are in real estate (particularly our homes) and financial assets (including our superannuation.)

- As you can see, the net wealth position of Australian households is still high since asset growth has outpaced the increased debt levels, meaning our net wealth position, while falling a little lately, is very strong.

- The Australian residential property market is valued at over $12.3 trillion, yet there is only around $2.5 trillion worth of debt against this large asset base. In fact, 50% of homeowners don't have a mortgage against their homes.

- Housing values continued to rise in January despite affordability squeeze and renewed cost of living pressures and I expect our property values to keep rising moving forward.

- Currently, Australia has a shortfall of housing, which is particularly showing up in our rental markets with historically low vacancy rates and skyrocketing rents.

- The government has a plan to build 1.2 million homes in the next 5 years, but I can't see how this will be achieved.

- The cost of residential construction has risen substantially in the last few years, in part because of the lack of available skilled labour and supply chain restrictions.

- This means the cost to build new apartments has risen to such an extent that most developments on the drawing board (see the following chart of dwelling approvals) are not currently financially viable and won’t be built until the market is prepared to pay substantially more than the current prices.

- It has been estimated that currently we have a deficit of well over 200,000 properties, something that won't be made up any time soon.

- In other words... there is no end in sight for the undersupply of dwellings. It also means that there is substantial inbuilt equity in established properties, as their replacement cost is very much higher than their current market value.

While the property pessimists were making a fuss about low housing loan commitments, which are clearly a leading indicator of what's ahead for our property markets, the following chart shows that they have picked up recently and are well above long-term averages.

In particular, investor lending is up by more than 30% over the last 12 months. In other words, strategic investors are taking advantage of the current window of opportunity to get into the housing market.

Business Sector

- Australian businesses are facing a continual conveyor belt of challenges, including the rising cost of living, which is dampening discretionary spending as the RBA is hell-bent on slowing our economy.

- The near-term business outlook is one of softening consumption and investment growth, tightening government expenditures, and high debt costs.

- This troubled backdrop has been reflected in low business investment, which now seems to be picking up.

Labour Markets

- Australia's labour market continues to show impressive resilience in the face of high-interest rates and unprecedented global challenges.

- The ABS has reported the following Key Statistics in trend terms, in December 2025:

- unemployment rate decreased to 4.2%.

- participation rate remained at 66.8%.

- employment increased to 14,686,100.

- employment to population ratio remained at 64.0%.

- underemployment rate remained at 5.9%.

- monthly hours worked increased to 1,997 million.

- Australia's unemployment rate, a key indicator of labour market health, has been at very low levels for a number of months now.

- The labour force participation rate is an estimate of an economy’s active workforce. The formula is the number of people ages 16 and older who are employed or actively seeking employment, divided by the total non-institutionalized, civilian working-age population.

- The participation rate in Australia averaged 63.51% from 1978 until 2022, as you can see from the chart below the participation rate has increased over the last few years as a bigger percentage of Australians have entered or re-entered the workforce.

- As you can see from the chart below, service-related industries have had significant growth, and in particular, there has been strong growth in the healthcare, accommodation and food services industries.

- Currently, there are 326,700 jobs advertised, a decrease of 0.2% from August 2025.

- Private sector vacancies were 287,400, a decrease of 0.5% from August 2025.

- Public sector vacancies were 39,300, an increase of 1.8% from August 2025.

- While national average wages have underperformed inflation over the last couple of years, meaning that “real” wages have actually fallen, we are now experiencing moderate wage increases.

- Recently the Fair Works Ombudsman increased the minimum award wage.

Interest Rates

- Interest rate levels set by the RBA respond to changes in inflation. When rates rise, they slow economic growth and discourage borrowing, typically signalling a strong economy. On the other hand, low interest rates promote economic growth.

- In a unanimous decision, the Reserve Bank Board increased interest rates by 0.25% at its meeting last Tuesday. This marks the end of the shortest and most modest rate-cutting cycle since the RBA started inflation targeting in 1993.

- Despite the sharp rise in interest rates over the last few years, home loan arrears remain at post-GFC lows, defying those property pessimists who forecast that significant levels of mortgage stress would lead to forced sales by homeowners who got over their heads in debt.