Key takeaways

Most Australians sit on a clearly defined level of the wealth pyramid - and rarely move unless they change how they think, earn, spend, and invest.

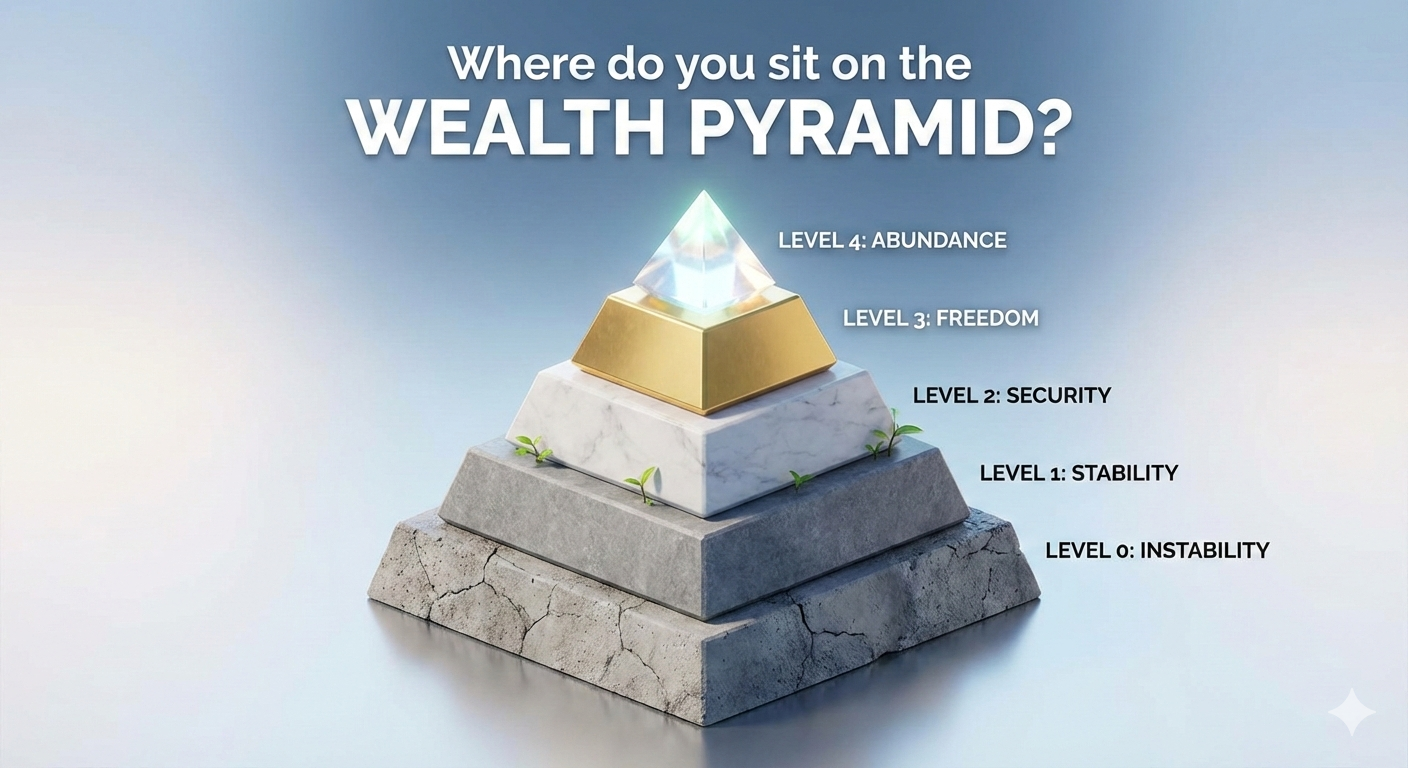

Level 0 and Level 1 are survival zones. People here rely almost entirely on wages, have little margin for error, and are most exposed to economic shocks.

Level 2 is the turning point. This is where people begin accumulating assets, but progress is fragile without discipline and a long-term strategy.

Level 3 is where real wealth momentum begins. Asset growth starts to outpace income, leverage works in your favour, and time becomes a powerful ally.

Level 4 is reserved for a small minority. Here, assets do the heavy lifting, income is optional, and financial decisions are driven by optimisation, not necessity.

Each level requires different financial rules. What keeps you safe at lower levels will stop you progressing at higher levels.

Moving up the pyramid is sequential - you can’t skip levels, and shortcuts usually end in setbacks.

Property is the primary vehicle Australians use to climb the pyramid, providing leverage, income, tax efficiency, and long-term capital growth.

The real risk isn’t investing too early - it’s staying too long on the lower levels while time quietly works against you.

Most people say wealth means a big salary with a lifestyle to match.

Most people equate wealth to money, but that’s not how wealth works.

You need a lot more than money to be truly wealthy.

You need your health, your friends and family to share it with, you need personal growth, spirituality (this means different things to different people) and contribution.

As you can see, to me wealth is a product of the mind and no amount of money will make you wealthy.

To be truly wealthy you have to be grateful for what you have in life and you have to be living a life where you know you are contributing or giving back.

Financial independence is different to wealth

It means you never have to work again to live your life.

That’s what you’re really investing for, isn’t it?

My suggestion is that you should be committed to being wealthy as well as financially independent.

Just to make things clear… income by itself does not make you financially free.

In fact, income is one of the worst predictors of financial freedom.

You spend some, maybe you save some, and taxation takes away a portion of it.

Most people in Australia never become wealthy; they never develop real financial independence.

For most people, the bills keep mounting up and despite working more and more hours they can’t make ends meet.

So it’s not really income you are after

To secure your financial future you need to acquire assets that grow in value and bring in passive recurring income.

Having dealt with Australians from all walks of life, I’ve developed a number of models to explain the progression most investors take in their path to developing financial freedom.

These models help you know exactly where you are heading financially, where you are at along the way, and the key focus areas and leverage points you can use to fast-track your journey.

Let’s look at what I call…

The Wealth Pyramid

My financial model — the Wealth Pyramid — shows your current level on the path to financial independence and identifies the key focus areas and leverage points to accelerate your progress.

Like all pyramids, it has a wide base and tapers towards the top; in other words, most people are at the lower levels of the wealth spectrum, and fewer reach the top.

Hopefully, the knowledge and skills you’ll learn from articles like this, my books and my podcasts will help you work your way up the pyramid, but the solutions you’ll need to move from one level to the next will vary depending on where you are.

Unfortunately, most people don’t really have any wealth and therefore are at…

Wealth Level 0 — Financial Instability

Since most people live from pay cheque to pay cheque, they are what I call Financially Unstable.

If they lose their job, or if they have an emergency (you know how these keep cropping up — an illness, the car breaks down, the refrigerator breaks down), they have no financial reserves to cope.

Since they have no spare financial capacity, the only way to cope with these burdens is for people at Level 0 to borrow more (and get further into debt), and this only creates more financial hardship.

They live their lives with their heads buried in the sand, not really conscious about money and their spending habits.

If they have money, they’ll spend it; if they don’t, they’ll borrow it because their favourite pastime is shopping and buying “stuff” they don’t really need.

This means much of what they own has debt attached to it.

They keep doing this and fooling themselves that they’ll just work harder and pay off their debt someday.

If you ask them what their problem is, they’ll tell you they don’t make enough money.

They think more money will solve their problems. But that’s not right.

Their biggest problem is their money habits, which have nothing to do with how much they earn.

It’s what they do with the money they earn.

As they move on in their lives and earn more, they just spend more.

Today, they can’t survive on the type of income they would have only dreamed they could achieve five years ago.

There are many high-income earners who fall into this category because they spend as much or more than they make.

Sure some people at Level 0 Wealth can look rich — they may even have big homes or fancy cars, but they also have huge loans that they struggle to repay.

Unfortunately, they often argue with their spouses about money, being in financial denial and justifying why they bought this or that.

Wealth level 0 can really be divided into two subgroups

- Casualties — I call those at the lowest level this because they’re casualties of the money game. Each month they seem to find themselves in a worse place than they were the month before — getting themselves deeper and deeper in debt, usually through credit card debt.

They’re paying high-interest rates today to use tomorrow’s money now.

Of course, they blame others for their problems — it’s never their “fault”.

They’ve often read books about budgeting or been told the trick of cutting up credit cards, but that just doesn’t work.

They don’t know how to “do” money. Then, half a level up the pyramid are the…

- Survivors — these are employees, self-employed or even business people who seem to make just enough money each month to have nothing.

And if by accident they end up with some money in the bank they spend it or take a holiday. They are just surviving.

While the fact is that at Level 0 people simply live beyond their means, the real cause of their problems is in denial of this.

Unless they are prepared to change, their financial future is bleak.

The fundamental key to getting out of this level is mindset, education and taking financial responsibility.

So first be honest with your personal cash flow position.

Then stop the bleeding by changing your financial habits and at the same time get a financial mentor.

The fact is, when you’re at Level 0, you can’t get out of your problems on your own.

You need someone to mentor you, and you need to be part of a group — just like getting fit or losing weight — it’s just too hard to do on your own.

How many people sit on the couch watching diet videos while eating ice cream? The next rung up is…

Wealth Level 1 — Financial Stability

This is the most basic level of wealth and provides some financial security.

You have achieved Financial Stability when:

- You have accumulated sufficient liquid assets (such as money in an offset account, line of credit or savings) to cover your current living expenses for a minimum of 6 months.

- You have private medical insurance and some life insurance to protect you and your family’s lifestyle should you become permanently ill, disabled, unable to work or, if worse comes to worst, you suddenly die.

I know that’s an unpleasant thought, but in the last year, two of our acquaintances died, leaving their families in financial trouble.

At this level, you will have the peace of mind that should any unexpected challenges come your way, such as retrenchment, a business failure, illness or disability, you and your family’s lifestyle will not be unduly compromised.

You will have sufficient time to identify new income sources to get back on track.

The problem at this level is that your cash flow is being controlled by others — your boss who pays your salary, or your clients who pay for your services.

This means you’re still on a treadmill and you don’t have the ability to increase your cash flow without working more, and that has its limits.

Sure you’ve got a bit of a financial buffer, but if you stop working for a while you slip back to Level 0.

Note: If you’re at Level 1 your goal should be to move more of your cash flow into assets and build that Cash Machine so your income does not depend on you putting in more effort.

At this level, your biggest leverage comes from investing in yourself and becoming financially savvy building a solid base of financial and investment skills upon which you can grow your financial future, as well as beginning to build a network of peers you can make your journey with.

You’ll also have to choose the first wealth vehicle you are committed to master and become a devoted student, learning all you can about this niche wealth vehicle.

In my opinion, the best place for most people to start is residential real estate investing.

In making the decision on which wealth vehicle to go after, you must cultivate the discipline to say no to the pull of other "great opportunities" and vehicles.

I’ve made more money by saying no to second-rate investment opportunities than I’ve made by saying yes to them.

Then carefully choose who you’ll study with.

Contrary to popular belief, the most expensive education isn't "graduate school" like an MBA.

The most expensive education is one based on a flawed model and incorrect information.

The hardest form of learning is UN-learning all the wrong, mistaken, and flawed things you "learned" from unqualified teachers.

So choose to learn from the best.

It will save you years of frustration following defective models.

Your aim should be to move up to…

Wealth Level 2 — Financial Security

You achieve Financial Security when you have accumulated sufficient assets to generate enough passive income to cover your most basic expenses.

These would include not more than the following;

- Your home mortgage and all home-related expenses such as your utilities, rates and taxes.

- All your tax payments plus the interest payments on your loans and debts.

- Your car expenses.

- Your grocery bills and minimal living expenses.

- Any insurance premiums including medical, life, disability and your house.

When you reach the level of Financial Security, you will be able to stop working and still be able to maintain a simple, basic lifestyle.

Of course, you’ll want more than that.

At Level 2, you will be an investor focused on building your net worth by owning assets that appreciate in value, and ideally, you’ll accelerate the process by “manufacturing” capital growth through renovating or developing residential real estate (I’ll get into this in Section 4 of this book)

At the advanced stage of Level 2, you are beginning to make the transition from capital gains investing to investing for passive, residual cash flow.

This means you've got to master a whole new skill set.

You’ll also have to radically upgrade your advisor network and peer group.

Being the big fish in a small pond no longer serves you. You need to begin playing with people better than yourself ,because you want to move up to…

Wealth Level 3 — Financial Freedom

You know you have achieved Financial Freedom when you have accumulated sufficient assets to generate enough passive income to pay for the lifestyle you desire (not necessarily your current lifestyle) and all of your expenses, without ever having to go to work again.

Having first built a substantial asset base (of properties, shares or businesses), now you are using your assets to create cash flow, which doesn’t mean you won’t go to work again, but you will now be able to make the choices you want because you have time freedom.

At Level 3 your focus should be on stabilising your passive income streams and fine-tuning your estate planning and asset protection.

Now is also a great time to grow your service to the world by finding ways to expand your contribution.

Tip: Level 3 is NOT about "retirement", it's about regeneration and contribution.

Wealth Level 4 — Financial Abundance

A small group of people around the world achieves Financial Abundance when their Cash Machine works overtime.

Not only are they free of financial pressures, but they have so much surplus income after paying for their lifestyle, all of their expenses and their contributions to the community (often through charity work or donations) that their asset base just keeps growing and growing.

A couple of thoughts about the Wealth Pyramid

There is nothing new about this hierarchy of wealth; it’s always been there, and we’re all part of it.

Complaining about where you are won’t help; however, your level of wealth is your choice. Despite that, most people get stuck at a particular level.

The good news is that everyone can move up the Wealth Pyramid.

Understanding where you are empowers you to ensure you do what you need to do to get to the next level.

But this never happens by accident; you have to earn your way up through personal development and upgrading your mindset.

In fact, the aim of our annual Wealth Retreat, which we'll be holding on the Gold Coast at the end of May, is to help you work your way up the wealth pyramid faster and more safely

The 4-step formula for financial independence

Here are four timeless rules for achieving financial freedom.

Please don’t dismiss them because they sound so simple:

- Spend less than you earn. This maxim may seem obvious, but many people have difficulty following it. If you're spending more than you earn, you will never become financially independent. You will be paying money to others for the rest of your life. The earlier you start living by this rule, the better. It is never too late to start.

- Invest the difference wisely. It may surprise you but the average Australian, earning between $60,000 and $70,000 a year for 40 years will earn somewhere between $2.5 and $3 million during their working life. Yet most of them will retire poor. Clearly, the level of your income has no bearing on the level of wealth you achieve, what is critical is the amount you save and invest wisely.

- Reinvest your investment income so you get compounding growth.

As you are beginning to understand, you will never become financially independent on your earnings alone.

You need to keep reinvesting.

In fact, by the time you become financially free almost all your assets will have come from compounding capital growth, not from your income, your savings or your rent.

- Keep doing steps 1 and 2 until your asset base reaches a critical mass so that you have the Cash Machine that gives you the income you desire.

If it’s as simple as that, why don’t more people develop financial independence?

Because it requires discipline and delayed gratification — sacrificing today in return for more choices later in life.

Here is what you can do to climb the Wealth Pyramid

Where you sit on the wealth pyramid today isn’t a judgment - it’s simply a snapshot in time.

It reflects past decisions, past habits, and how long your money has been working for you.

The encouraging part is this: your current level doesn’t dictate where you must stay.

But moving up the pyramid doesn’t happen by accident.

Each step requires better thinking, better strategy, and better decisions than the ones that got you where you are now.

And the higher you climb, the more costly mistakes become.

That’s why the most successful investors don’t rely on guesswork, media noise, or isolated advice - they surround themselves with people who’ve already walked the path.

That’s exactly why we created Wealth Retreat.

It’s an immersive, strategy-focused experience designed for people who are serious about accelerating their progress up the wealth pyramid - not by taking reckless risks, but by making smarter, more informed decisions.

Over five intensive days we break down what actually separates those stuck on the lower levels from those who systematically move higher, year after year.

You’ll gain clarity on where you really sit on the pyramid, what’s holding you back, and what needs to change if you want to move up faster and more safely.

More importantly, you’ll leave with a clear framework you can apply immediately - not theory, not hype, but proven principles refined over decades of real-world investing.

The reality is this: time alone won’t move you up the pyramid. Strategy does. And the sooner you get that strategy right, the less you need to rely on luck.

If you’re ready to stop drifting between levels and start deliberately climbing, Wealth Retreat 2026 could be the most important investment decision you make this year.

Click here to find out more and register your interest - Don't count yourself out

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026