Key takeaways

Once considered a symbol of luxury, $1 million is now standard for housing in many parts of Australia.

In August 2024, the combined capital cities’ median house value passed $1 million, confirming this is no longer just a “Sydney phenomenon.”

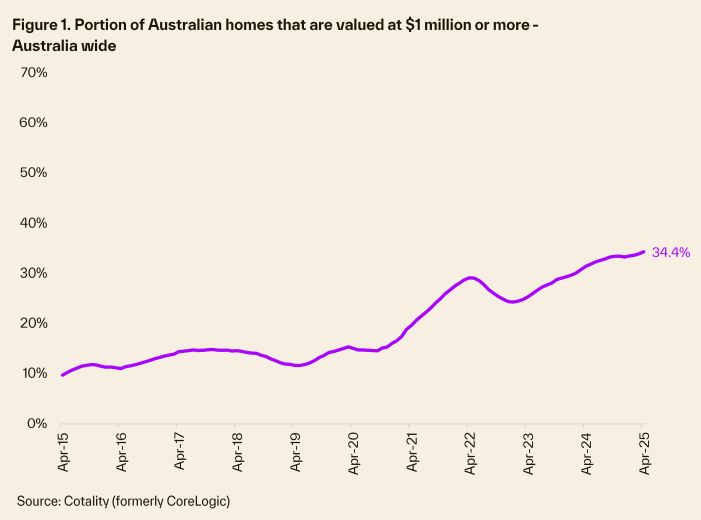

Nationally, 34.4% of homes are now valued at $1M+, up from just 9.7% in 2015.

Regional areas have seen a particularly sharp rise—from 0.5% to 19.4% of homes valued above $1M.

Capital cities surged from 14.3% in 2015 to 41.6% now, both figures at all-time highs.

When it comes to most aspects of life, $1 million goes a long way.

Whether it’s a lifetime of family groceries1, 75 years’ worth of household transport costs2, or smashed avocado for breakfast every day, for over 100 years3.

For housing, however, $1 million is increasingly standard.

In August last year, the median house value across the combined capitals surpassed the million-dollar mark, breaking the perception that Sydney was the only millionaire’s club for homeowners.

New research from Cotality (formerly CoreLogic) shows a over a third of homes nationally are now valued at $1 million or higher, with that vast amount of money buying less in the housing market now than ever before.

Data going back ten years shows the portion of dwellings valued at $1 million or more has risen from 9.7% in April 2015 to 34.4% as of April 2025, a series high.

This includes 19.4% of homes across regional Australia (up from just 0.5% a decade ago) and 41.6% across the combined capitals (up from 14.3% a decade ago).

Both were at a series high.

The trend reflects strong price growth across Australia’s housing market, where values have increased 67.3% in the past ten years.

Capital cities

Sydney had the highest portion of homes over $1 million, where almost two-thirds of stock are past the million-dollar threshold (64.4%, a series high).

This is unsurprising given that the median value of all houses and units in Greater Sydney was $1,195,000 in April.

Even for those with a budget of $1,000,000, the kind of property available in Sydney is generally smaller and further afield than a decade ago.

Only houses with five or more bedrooms had a median value over $1 million in Greater Sydney a decade ago.

Now the median house value for all bedroom types is over $1 million, ranging from a median of $1.3 million for a three-bedroom house to $2 million for a house with five or more bedrooms.

Brisbane had the next highest proportion of homes valued at $1 million or more, at 40.2%.

This is up from just 2.8% a decade ago and is the highest increase in the period of any region.

Figure 2 highlights the stark trajectory change of homes at $1 million or more, which went from 6.2% to 40.2%, in just five years.

Brisbane will almost certainly be Australia’s next ‘million-dollar’ house market of the capital cities, with a current median house value of $990,000.

Even if Brisbane house values rise at half the rate that they did in the 2024 calendar year, they would hit $1,010,000 by the end of 2025.

Third in the capital city rankings was Melbourne, where 30.9% of homes have a $1 million-plus value as of April.

This is down from a high of 33.1% in January 2022, shortly before interest rates were adjusted from historically low levels.

- Also read:Perth housing market update | June 2026

- Also read:Brisbane housing market update | June 2026

- Also read:Sydney housing market update | June 2026

- Also read:Australia’s Building Crisis Is Getting Worse – What It Means for Property Investors | Property Insiders

- Also read:Australian housing market update | June 2026

While this reflects more subdued market performance and more affordable housing conditions across the city, the portion has increased from 30.0% in February of this year, and is up from 12.4% of homes a decade ago.

Adelaide and Perth followed a similar trajectory to Brisbane, with strong value increases since the pandemic, creating a sharp increase in the portion of million-dollar-plus homes across these cities.

Adelaide saw million-dollar homes go from 4.2% of the market in March 2020 to 27.8% of homes in April this year.

For Perth, just over a quarter of homes are now $1 million or more, up from 6.0% in March 2020.

Hobart stands out as a city that has seen a reversal of the million-dollar home status, as dwelling values sit 11.1% below a high in March 2022.

Between March 2022 and April this year, the portion of dwellings in greater Hobart with a million-dollar-plus price tag went from 20.3% to 11.9%.

A combination of rapidly rising interest rates, weak population growth trends and relatively weak job growth may have contributed to sustained home value declines across the city.

Darwin had the lowest portion of million-dollar homes, at just 1.3% in April 2025.

This has been consistent across the city, where 1% of homes were valued at $1 million or more a decade ago.

Since the strong price rises through the 2000s infrastructure boom, values have been stagnant across Darwin over time.

While certainly the most affordable capital city by value, its remote location and relatively small economy mean it is simply not a viable option for many aspiring homeowners.

Why does a $1 million market matter?

Australia’s million-dollar housing markets are in part a reflection of our wealth and prosperity as a nation.

After all, housing markets wouldn’t have a million-dollar price tag if at least some Australians couldn’t come up with that level of finance.

As values continue to rise, the chance that homeowners hit millionaire status increases, opening up new opportunities for further investment or accessing that wealth through the sale of a property.

However, the downsides of such an extraordinary price point are also increasingly evident.

The rate of home ownership has gradually declined over time, particularly among younger, low-income households where income cannot keep pace with growth.

The average age of first home buyers has increased, and increasingly wealthy households are stuck renting for longer, which increases competition for low-income, renting households.

Housing debt has also blown out to keep pace with rising values relative to more subdued wages growth.

Housing debt relative to income was recorded by the RBA at 135% at the end of last year (albeit down from a high of 139% before the bulk of cash rate rises in September 2022).

This was up from 122% a decade prior.

With values expected to continue rising on the back of rate falls in 2025, the wealth divide between homeowners and non-homeowners is also likely to expand.