Both the Fairfax newspapers and The Australian ran pieces on the prudential regulator and lending settings, following a media interview with the APRA Chair.

The gist running through several media articles was that mortgage arrears remain low for now, and the 3 percentage points lending assessment buffer introduced in October 2021 remains in place for the time being.

Back in the distant olden days - well...in 2019 and before - mortgages were typically stress-tested to ensure borrowers could comfortably absorb a 2 percentage points increase in interest rates.

But lending standards have continued to tighten, continuing an ongoing trend over the past dozen or more years.

Mortgage prisoners in stress

APRA reported that there are "pockets of stress" but these don't cause undue concern - except for the borrowers themselves, I guess - although small businesses are increasingly falling into arrears.

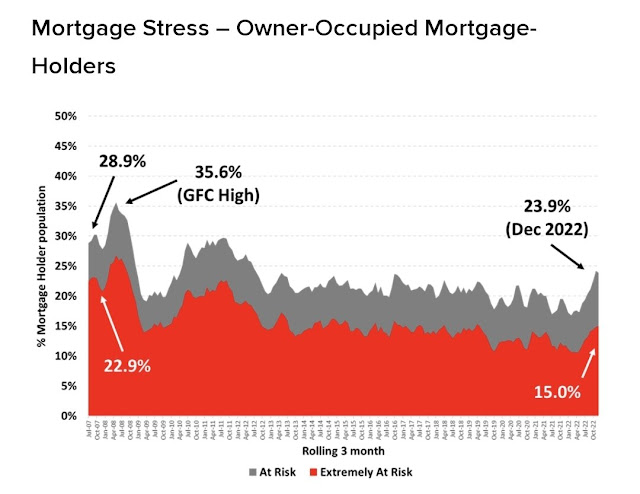

In reality, mortgage stress is of course at decade highs and rising, and is already tracking at the highest levels since July 2013:

Source: Roy Morgan Research

Roy Morgan calculates that mortgage stress will increase significantly further by March due to rising interest rates.

Monitoring settings

The regulatory Chair John Lonsdale noted that "we are looking at the serviceability buffer very very closely" - and noted that it can be tweaked back down if necessary - but, for now, "we are happy with where the prudential settings are."

These settings are self-evidently making it very difficult for many recent and existing borrowers to refinance, having been slugged with higher rates as the record surge in fixed-rate mortgages resets too much onto much higher mortgage rates.

Essentially, it's a softer echo of the US subprime reset through the global financial crisis.

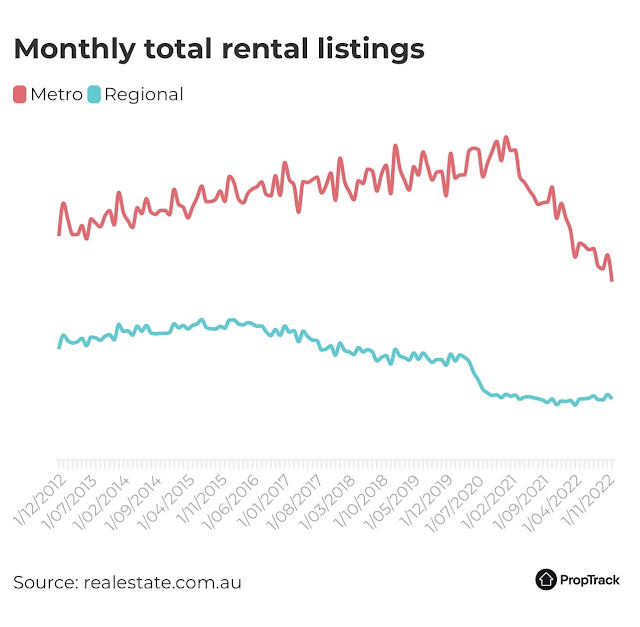

The other pressing issue is that the extremely wide buffer has effectively choked off the supply of credit to landlords.

Metropolitan rental listings - having already halved from a year ago - are plummeting at warp speed towards zero.

I'm not sure if it's fully appreciated that there will be well over 100,000 international student arrivals in February - possibly more than 150,000 - with permanent migration also finally set to get moving again.

We're now in an unusual situation where rents are rising by around 20 per cent per annum, but many prospective landlords can't borrow, so there is no supply response.

APRA said it will release an updated paper on macroeconomic policy settings in February, but in my opinion, settings need to get back to normal.

The 3 percentage points buffer made perfect sense when interest rates were at zero, but now the interest rate hiking cycle is almost complete, and stress-testing should simply go back to the usual settings.