Key takeaways

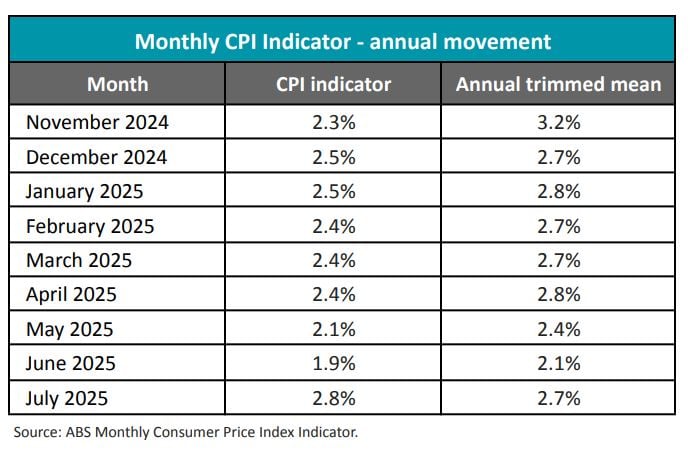

Headline CPI rose to 2.8% in July (up from 1.9% in June), driven mainly by electricity price hikes, delayed rebates in NSW and ACT, and higher holiday travel costs.

The Reserve Bank will likely wait for the September quarter CPI results (due 29 October) before cutting again, with November shaping up as the earliest timing.

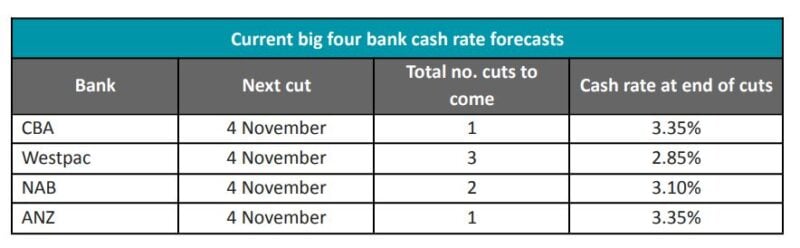

All big four banks expect the next cut in November, with Westpac forecasting up to three more reductions in the cycle.

Despite inflation rising, 88 lenders have reduced variable rates since August’s RBA cut.

Lower rates are already filtering through the lending market, even before the RBA acts again.

This is an opportunity to reduce costs, strengthen cash flow, and strategically position portfolios ahead of the next rate cut cycle.

Australia’s inflation story just took an interesting twist.

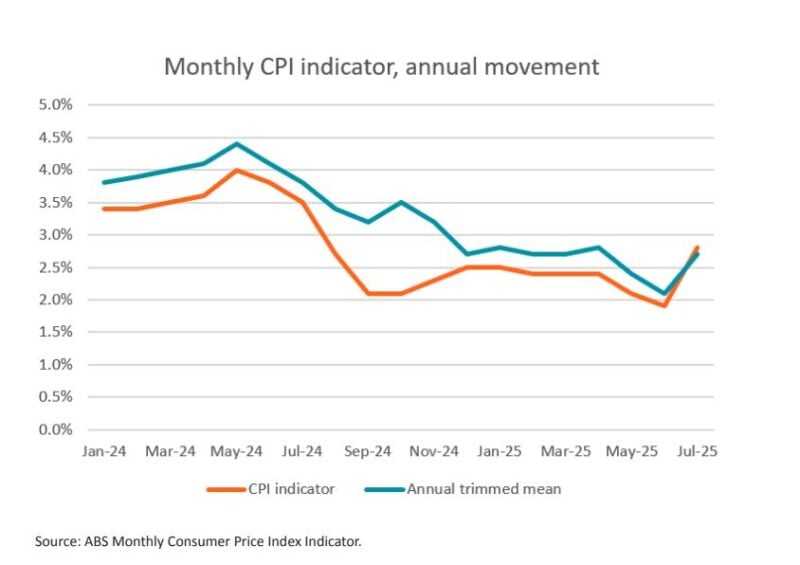

After months of trending down, headline inflation nudged higher in July: lifting to 2.8% from June’s 1.9%.

That may not sound like much, but it’s the first rise we’ve seen in the monthly CPI series since late 2024.

So, what’s driving it?

Electricity prices surged by over 13% in the past year, partly thanks to July’s price hikes and the delay in government rebates for NSW and ACT households.

Add in pricier holiday travel during the school holidays, and suddenly inflation has momentum again.

For property investors and homeowners, the question is: what does this mean for interest rates and, therefore your mortgage?

Why a September rate cut is off the table

The Reserve Bank was never expected to rush into another move at its 30 September meeting, but this uptick in inflation has shut the door completely.

As Sally Tindall, Canstar’s Research Director, puts it:

“The possibility of a September cash rate cut was a long shot at best, however, this round of monthly data squashes pretty much all hope of back-to-back moves."

The RBA Board has already signalled it prefers a gradual easing cycle.

They’ll want to see the September quarter CPI numbers (due 29 October) before taking action.

If the trend is still under control, then the November 3–4 meeting is shaping as the next opportunity.

The big banks agree. CBA, NAB, Westpac and ANZ all expect November to be the month, though their forecasts for how far cuts will go vary.

- Also read:Rents Surge Again as Interest Rates Bite – What Happens Next?| | Property Insiders

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

- Also read:National Weekly Auction Report – March 28th 2026 | Auction Clearance Rates Still Fading Over Super Week of Listings

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

Westpac sees three more cuts, potentially taking the cash rate to 2.85%.

Source: Canstar

Mortgage rates keep falling anyway

Here’s the real twist: despite inflation ticking higher, mortgage rates are still drifting lower.

Since the RBA’s August cut, 88 lenders have trimmed their variable rates, with most passing on the full 0.25% reduction.

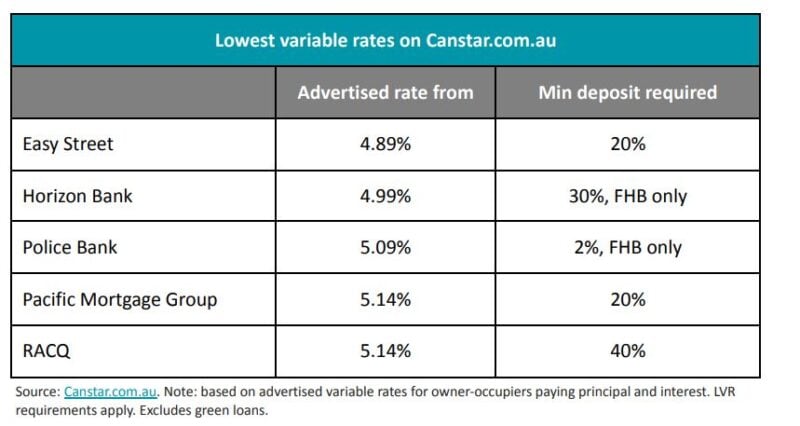

Easy Street has dropped to 4.89%, the lowest variable rate on the market right now. That’s ultra-competitive, but the offer is time-limited, available only for applications lodged before 10 October and settled by 10 December.

It’s not just Easy Street. Almost 30 lenders are now offering at least one variable rate under 5.25%, which is great news for borrowers willing to shop around.

What this means for property investors

If you’re a property investor waiting for the RBA to hand you another cut, don’t hold your breath, at least not until November. The RBA is being cautious, and rightly so.

I believe this offers a window of opportunity for property investors as we’re seeing what some would call a “perfect storm” of fundamentals that are aligning to support strong property markets in the years ahead:

- Continued rapid population growth is putting pressure on housing.

- An acute undersupply of dwellings,

- A chronic shortage of skilled labour, making new development slower and more expensive.

- Inflation has moderated, now sitting within the RBA’s target range.

- Interest rates will keep falling – bringing more buyers into the market

- Government first homebuyer incentives will pour fuel on the flames of our undersupplied housing market after October.

Are you clear on how to take advantage of these market conditions - that’s where our Complimentary Wealth Discovery Session comes in. We’re offering you a 1-on-1 chat with a Metropole Wealth Strategist to help you:

- Clarify your financial goals

- Understand how macro trends affect your position

- Build a personalised, data-driven property strategy

- Get ahead of the curve — before everyone else piles in

There’s no cost, no obligation — just practical, tailored guidance based on decades of experience.

Click here now to book your free Wealth Discovery Session