Key takeaways

Sydney and Melbourne are currently underperforming, with softer prices and weaker sentiment driven largely by interest rate sensitivity. This is expected to continue through 2026.

Smaller capitals like Brisbane, Perth and Adelaide have led recent growth, but their cycle is maturing and momentum is expected to slow into 2027.

ANZ forecasts a shift in 2027, with Sydney and Melbourne regaining leadership and outperforming other capitals. This reflects a typical rotation in the property cycle.

Strong fundamentals remain in Sydney and Melbourne, including population growth, limited housing supply, and their role as economic hubs. These factors are tightening conditions despite the current weak sentiment.

The current softness presents a strategic opportunity, as markets tend to recover before sentiment improves. Investors who act early during uncertainty are typically best positioned for the next growth phase.

Right now, Sydney and Melbourne look like the laggards of Australia's property market.

Prices are soft, consumer confidence is at record lows, and most of the headlines are celebrating Brisbane, Perth and Adelaide.

But if you've been around property long enough, you know that today's underperformer is often tomorrow's leader.

That's exactly what the latest ANZ Research forecast is pointing to - and it's worth paying close attention.

The short-term pain is real

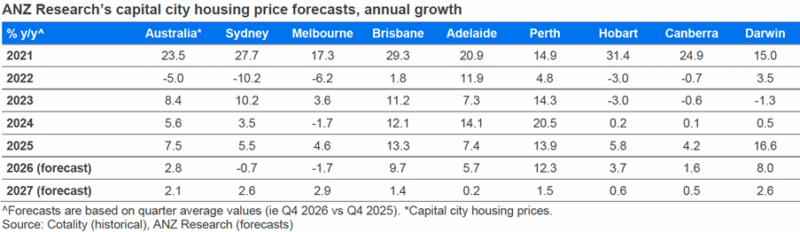

ANZ's April 2026 update has lowered its capital city housing price forecast to 2.8% growth for 2026 and 2.1% for 2027.

That's quite a step down from the 4.8% they were forecasting just a few months ago.

Sydney and Melbourne housing prices are already sitting below their October 2025 levels, and properties in the top quartile of both cities have declined for five consecutive months.

Both these cities tend to be more interest rate-sensitive than the rest of the country, and ANZ expects to see the sharpest price slowdowns there in 2026, including small falls in housing prices.

I won't sugarcoat it - 2026 is going to be a softer year for both cities, but that's not the story I want you to focus on.

The numbers tell the story

Over the last couple of years, the so-called “smaller capitals” like Brisbane, Adelaide and Perth have had their turn in the spotlight.

They’ve delivered strong growth, supported by affordability, interstate migration, and relative value compared to Sydney and Melbourne.

But ANZ is now signalling that this cycle is maturing and expect those markets to slow more noticeably into late 2026 and underperform in 2027.

That’s classic property cycle behaviour. Capital flows chase momentum, then overshoot, and eventually rotate back to the larger, more established markets.

We’ve seen this happen before.

The 2027 reversal is already baked in

By 2027, ANZ forecasts Sydney prices growing again at around 2.6% and Melbourne at 2.9%, outperforming most other capitals.

Sure, on the surface, those numbers don’t look exciting, but they’re telling you something important. The leadership baton is being passed back.

And in my view, that outperformance is likely to be stronger than the headline numbers suggest, particularly in the right segments, because, as always, there isn't one Sydney or Melbourne property, mark.

Let's look at why this is likely to occur.

1. They remain the economic engines

Sydney and Melbourne still dominate Australia’s economy. They attract the bulk of high-income jobs, corporate headquarters, and global capital.

When confidence returns, even modestly, these markets tend to respond first because that’s where the money is.

2. Population growth keeps pressure on

Population growth is expected to remain solid while supply remains constrained and that imbalance is more pronounced in Sydney and Melbourne than anywhere else according to ANZ.

We’re simply not building enough well-located dwellings, and planning constraints are making it worse.

In other words, the fundamentals are quietly tightening despite sentiment still being weak.

3. Supply is structurally constrained

Higher construction costs, labour shortages, and feasibility challenges are choking new development. And this is only going to get worse with the fuel shortages.

4. Interest rate sensitivity works both ways

Sydney and Melbourne fall faster as interest rates rise, but they also recover faster when rates stabilise or fall.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

Once the market becomes confident that the rate cycle has peaked, even before cuts actually happen, sentiment lifts and that’s typically when these markets turn.

Patient, strategic investors consistently outperform the crowd because they read these turning points early rather than following the herd.

In reality, it’s about positioning. By the time 2027 arrives and the outperformance is obvious, the opportunity will largely be gone.

The smart money moves earlier, during the uncertainty phase we’re in now.

Why Sydney and Melbourne have more runway

Sure, Sydney and Melbourne are expensive cities, but their current softness is primarily driven by interest rate sensitivity, not a fundamental deterioration in demand.

And that matters enormously for what comes next.

ANZ believes widespread falls in housing prices are unlikely given the structural tightness of the market, with higher interest rates and building costs likely to negatively impact supply, while population growth is expected to remain solid.

Sydney remains Australia's most globally connected city - a magnet for high-income earners, international migrants and knowledge workers.

Melbourne is the country's fastest-growing city by population and has a chronic undersupply of well-located housing relative to what's needed.

Neither of these underlying drivers goes away because the RBA raises rates.

CBRE estimates that over the next three years, investment returns for apartments in Sydney and Melbourne are set to outpace historic levels.

CBRE also estimates that apartment delivery in Sydney will average just 11,700 per year between 2025 and 2030 - well below the 30,000 per year required to meet demand - which means vacancy rates are forecast to fall from 2.0% to 1.2%, and rents are projected to grow 24% over that period.

You can't keep underbuilding a city and then be surprised when values recover.

The tax policy wild card

The upcoming federal budget is expected to include potential changes to the taxation of housing, including a possible reduction in the capital gains tax discount and limits to negative gearing.

More recent Grattan Institute analysis suggests that if the CGT discount for individuals and trusts was reduced to 25%, property prices would probably fall by less than 1%.

ANZ has explicitly chosen not to include these potential policy changes in its base case forecasts, noting that the impact would vary across markets and that the detail of any announcement is still uncertain.

My view is that well-located, investment-grade property in Sydney and Melbourne will absorb any policy adjustments far better than secondary markets.

Quality assets with genuine owner-occupier appeal aren't primarily driven by tax incentives - they're driven by scarcity, desirability and long-term demand.

What this means for investors right now

I've been saying for a while that Melbourne in particular represents one of the better value propositions in the country right now.

Prices have been soft for longer than any other capital city. Sentiment is negative.

And that's usually exactly when the best opportunities emerge for investors who are thinking about the next five to ten years, not the next six months.

Sydney is more expensive, but the same logic applies - quality assets in the right locations are being overlooked by investors chasing the Brisbane and Perth growth stories.

The market is not rewarding patience right now, but markets eventually do.

The investors who will look back on 2026 as their best buying year are the ones who understood that the softness was temporary, the fundamentals were intact, and the cycle was simply doing what cycles do.

The bigger picture

I'm not dismissing the growth that Brisbane will continue to enjoy, especially up to the Olympic Games, but when ANZ's forecasts show Sydney growing faster than Brisbane and Melbourne growing faster than Perth in 2027, that's the market telling you where the next chapter of this story is being written.

The question is whether you'll be positioned to benefit from that recovery, or still waiting on the sidelines while everyone else is celebrating returns you could have had.

If you'd like to understand how to position your portfolio for what's coming in Sydney and Melbourne - and how to identify the specific locations and property types most likely to outperform - the team at Metropole would be glad to help.

We are much more than another buyer's agent. We help our clients grow, protect, and pass on their wealth and safely outperform the markets through strategic property and wealth advice.

Click here now and organise a chat with one of our Wealth Strategists, and we will explain to you how we can build a Strategic Property Plan tailored to your circumstances and where the market is heading, not just where it's been.