Key takeaways

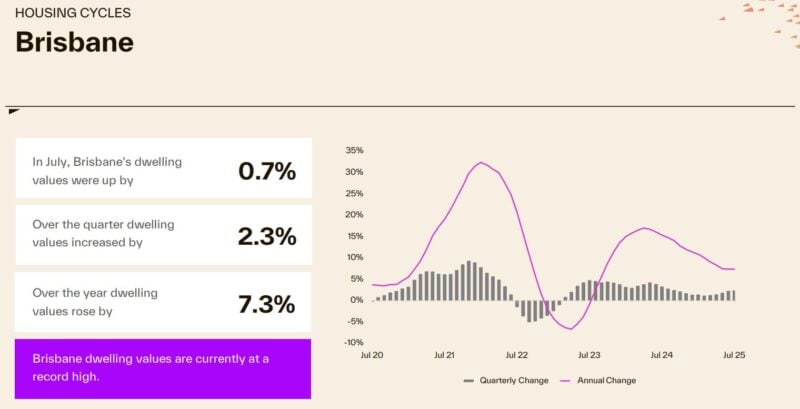

Brisbane’s house values have grown more than 50% since the onset of COVID, outperforming most capitals.

Demand continues to outpace supply, driven by interstate migration and low housing stock.

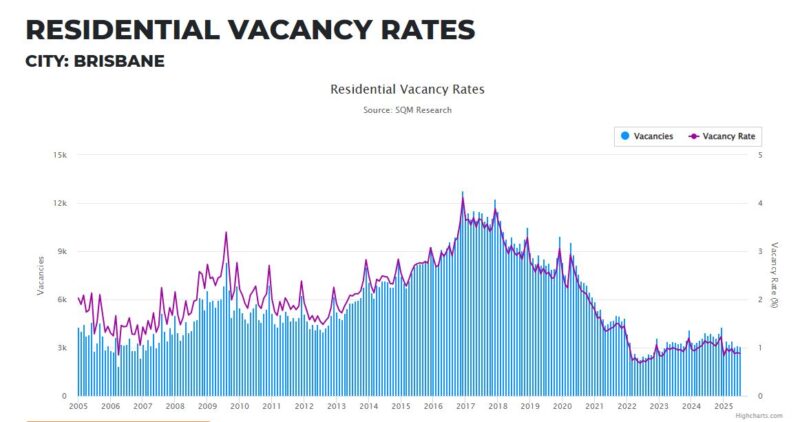

Vacancy rates remain critically low—below 1% in many suburbs.

Gross rental yields are strong, sitting around 4.5%–5.2% for houses.

Billions in infrastructure spending (Cross River Rail, Brisbane Metro, Queens Wharf) are enhancing connectivity and liveability.

The 2032 Olympics are providing long-term uplift and investor confidence.

Inner and middle-ring suburbs are outperforming outer fringe areas.

Affordability and lifestyle appeal make Brisbane a top pick for investors priced out of Sydney and Melbourne.

Brisbane has quietly but powerfully emerged from the shadows of Sydney and Melbourne and proven itself as a property market heavyweight.

While the southern capitals tend to grab many of the headlines, Brisbane real estate has delivered solid, sustainable growth over the last few years and it’s still going strong.

Now, with population surging, infrastructure booming, and the 2032 Olympic Games on the horizon, the River City is offering savvy property investors a rare mix of affordability, capital growth, and rental yield.

So, is Brisbane still a good place to invest in real estate in 2025?

What’s driving the Brisbane housing market?

Which types of property are primed for long-term growth?

In this article, we’ll unpack everything you need to know about investing in the Brisbane property market in 2025.

So far this year Brisbane’s housing market is defying gravity.

Despite all the economic uncertainty and rising living costs, demand continues to outstrip supply, especially in desirable inner and middle-ring suburbs.

Brisbane apartments are performing extremely well, as shown in the table below; especially larger, owner-occupier style units.

But it’s Brisbane’s detached housing market, particularly in lifestyle suburbs close to amenities and public transport, that continues to lead the way,

Here is the latest data on the median property prices for Brisbane.

| Property | Median price | Δ MoM | Δ QoQ | Δ Annual |

|---|---|---|---|---|

| All Capital city dwellings | $949,583 | 1.2% | 3.0% | 7.9% |

| Capital city houses | $1,040,651 | 1.2% | 2.9% | 7.3% |

| Capital city units | $740,992 | 1.3% | 3.9% | 11.1% |

| Regional dwellings | $752,533 | 0.8% | 2.5% | 8.5% |

Source: Cotality, 1st September 2025

Here's the forecast for Brisbane property prices in 2025-26

Domain’s latest Price Forecast Report for FY25-26 reveals that Australia’s property market is expected to see continued price growth over the next 12 months, with Brisbane unit prices expected to moderate from the previously unsustainable double-digit growth, while house prices continue to grow at a pace similar to that of last year.

Domain's House price forecasts

|

HOUSES | STRATIFIED MEDIAN PRICE |

||||||

| ANNUAL CHANGE | LEVEL | RECORD | BELOW PEAK | |||

| Capital City | FY25 | FY26 | FY25 | FY26 | FY26 | FY26 |

| Sydney | 4% | 7% | $1,717,107 | $1,829,576 | YES | |

| Melbourne | 0% | 6% | $1,046,246 | $1,112,623 | YES | |

| Brisbane | 5% | 5% | $1,037,357 | $1,093,414 | YES | |

| Adelaide | 12% | 4% | $1,013,204 | $1,049,117 | YES | |

| Canberra | -2% | 4% | $934,225 | $981,808 | NO | -7% |

| Perth | 7% | 5% | $934,225 | $981,808 | YES | |

| Combined capitals | 4% | 6% | $1,194,942 | $1,264,614 | YES | |

Domain's Unit price forecasts

| UNITS | STRATIFIED MEDIAN PRICE | ||||||

| ANNUAL CHANGE | LEVEL | RECORD | BELOW PEAK | |||

| Capital City | FY25 | FY26 | FY25 | FY26 | FY26 | FY26 |

| Sydney | 3% | 6% | $835,819 | $888,822 | YES | |

| Melbourne | -3% | 5% | $555,522 | $584,400 | NO | -3% |

| Brisbane | 12% | 5% | $670,798 | $701,490 | YES | |

| Adelaide | 10% | 3% | $568,000 | $586,366 | YES | |

| Canberra | -13% | 3% | $531,784 | $546,265 | NO | -15% |

| Perth | 12% | 6% | $519,551 | $552,487 | YES | |

| Combined capitals | 3% | 5% | $680,568 | $717,266 | YES | |

History suggests that once rates start falling, property prices don’t wait around.

Bank of Queensland chief economist Peter Munckton has crunched four decades of data which was reported in the Financial Review and said a 10 to 15 per cent price rise over the next two years is a reasonable bet – no matter how many cuts the RBA ends up delivering.

Munckton explained...

“There were smaller price rises in both the early 1980s and 1990s.

But on both those occasions, the unemployment rate was above 10 per cent.

Currently, the unemployment rate is within touching distance of 50-year lows,”

On the flip side, Munckton says the extraordinary 20 per cent-plus gains seen in the ’80s, ’00s and during the pandemic also seem off the cards over the next couple of years

Tip: The expansion of the first homebuyer support will add further fuel to our housing markets

From January 1 2026, virtually all first home buyers will be able to enter the market with just a 5 per cent deposit, via a taxpayer-backed guarantee.

This part of his election promise, prime minister Anthony Albanese promised to turbocharge the program by scrapping the $125,000 income cap, making it available to an unlimited number of applicants instead of just 35,000 per year, and dramatically raising property price thresholds.

A separate promise to build 100,000 new homes was also made – but that extra supply could take years to arrive, if it arrives at all.

Brisbane rents set to surge

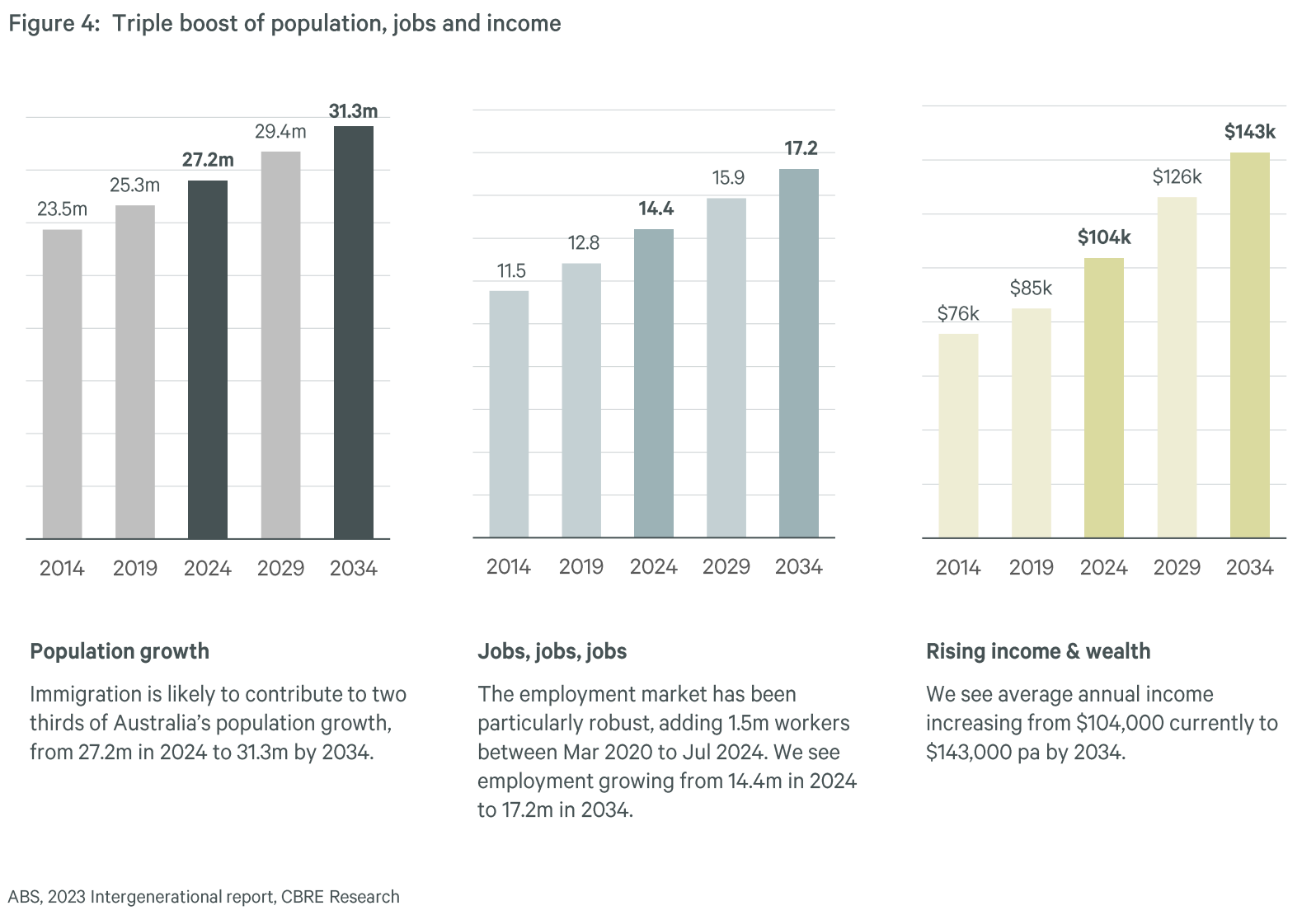

Median apartment rents are likely to grow by 24% between 2025 and 2030 across Australian capital cities, according to the latest report by International Property Consultancy, CBRE.

CBRE estimates Brisbane apartment delivery to average 4,600 per annum over 2025-2030. Demand for housing stock (apartments and communities) is likely to average 16,000 p.a., which will drive down city-wide vacancy from 1.1% to 0.7%.

Over the next 10 years, demand for housing is expected to benefit from a triple boost: rising population (+4.1 million), rising jobs (+2.8 million), and rising income (+$39k).

CBRE estimates around $960 billion of additional income in the system to support mortgage, rent, and other living expenses.

You can always beat the averages.

While it’s likely that Brisbane property price growth will moderate a little in the second half of 2025, the good news is that you can always beat it by investing in the right property in the right location.

Now by that, I don’t mean look for the next hotspot.

I mean buying quality properties in locations that will outperform in the long term such as gentrifying suburbs.

You see...property offers countless opportunities to improve your results through your own time, skills and knowledge – so you don’t need to settle for average.

And there’s more to it than just location. You can add value through refurbishment, or redevelopment.

Why Brisbane is Set to Keep Growing

Despite more homes being listed for sale and rising prices making property less affordable, the Brisbane property market is expected to keep steaming ahead in 2025.

A slowdown in construction has hampered the supply of new housing, concentrating buyer demand on existing properties.

But as interest rates keep falling throughout the year, buyer and seller sentiment will return to the market and it is likely the Brisbane will once again be one of the strongest performing housing markets in 2025.

At Metropole Brisbane we’re finding that strategic investors and homebuyers are actively back looking to upgrade, picking the eyes out of the market.

However, even when interest rates fall, affordability will remain an issue for many potential buyers who will only be able to pay up to the limit of what they can afford, so I would only invest in locations where wages are increasing faster than average and residents have multiple streams of income, not just wages.

This means investing in the more affluent inner-ring suburbs and the gentrifying middle-ring suburbs of Brisbane which will outperform the cheaper suburbs, where residents will still find it difficult to afford to buy a home and tenants are prepared to pay a premium to live in these locations.

Why Brisbane is Set to Keep Growing

1. Population Growth is Surging

Queensland continues to attract the lion’s share of interstate migration, with Brisbane absorbing much of the population inflow.

People are chasing lifestyle, affordability, and job opportunities—and that’s putting sustained pressure on housing demand.

2. Infrastructure Boom

Billions are being poured into infrastructure:

-

Cross River Rail

-

Brisbane Metro

-

Queen’s Wharf development

-

Major upgrades to road, transport, and health services

This isn’t just about short-term stimulus. It’s reshaping Brisbane’s accessibility and appeal, unlocking previously undervalued suburbs and supporting long-term growth.

3. Olympics 2032: A Decade of Opportunity

Hosting the Olympics will supercharge Brisbane’s global profile and catalyse further investment.

As we’ve seen in other host cities, this has a compounding effect on property values, infrastructure, and economic activity.

4. Affordability Advantage

Compared to Sydney and Melbourne, Brisbane remains significantly more affordable:

-

Brisbane’s median house price is significantly lower than Melbourne’s

-

Buyers and investors can enter the market with less capital, increasing competition in entry- to mid-tier suburbs

This affordability drawcard makes it appealing for both owner-occupiers and investors priced out elsewhere.

The best performing investment properties in Brisbane for 2025

Brisbane's property is offering savvy investors have plenty of opportunities to tap into its potential, but, as always not all properties will perform the same so it is crucial to pinpoint the types of residential properties and suburbs poised for out performance.

1. Houses in Lifestyle and Growth Suburbs

Detached homes in established Brisbane suburbs with lifestyle appeal will continue to be the top performers in Brisbane.

With a growing influx of families and professionals moving from southern states in search of more space, affordability, and a better lifestyle, houses in Brisbane’s established suburbs will maintain strong demand.

These properties offer capital growth potential and stable rental yields.

I would recommend investors buy a 3 or 4 bedroom home with land, proximity to schools, parks, shopping centres, and transport links.

Properties with renovation potential or extra land for future development can be particularly valuable and will allow the investor to “manufacture” capital growth and rental growth.

Brisbane’s Inner-City Suburbs like Paddington, Ashgrove, and Red Hill are likely to perform strongly.

These suburbs offer a blend of heritage charm, access to the CBD, and a strong café culture.

The scarcity of land, coupled with ongoing demand from professionals and families, makes them ideal for capital growth.

Also western suburbs in Brisbane like Indooroopilly, Chapel Hill and Kenmore should outperform.

Known for their excellent schools, green spaces, and family-friendly lifestyle, these suburbs have experienced consistent demand and offer strong rental yields and capital growth potential.

The Brisbane suburbs of Stafford, Kedron, Wavell Heights, Cannon Hill, Camp Hill and Mansfield enjoy infrastructure improvements, proximity to major employment hubs, good schools and with gentrification in full swing, these suburbs are gaining popularity among families and young professionals.

They offer affordable entry points with good prospects for capital growth over the next few years.

2. Townhouses in Inner and Middle-Ring Suburbs

The shift towards medium-density living is a continuing trend in Brisbane as more people seek affordable alternatives to traditional houses without compromising on space and location.

Townhouses offer a great balance, providing more room than apartments but at a lower entry price than standalone houses.

This segment is gaining popularity among young families, professionals, and downsizers.

3 bedroom townhouses in low-density, modern developments with easy access to transport, retail hubs, and lifestyle amenities make great long term investments.

Properties with outdoor spaces or private courtyards are highly sought after as both tenants and own occupies are prepared to trade backyards for courtyards.

Look for townhouses in South Brisbane and Greenslopes.

These inner-city areas are undergoing rapid transformation with new infrastructure and urban renewal projects, making them attractive for townhouse investments.

The demand from professionals working in the CBD and nearby hospitals ensures solid rental demand.

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – September 2025

- Also read:This week’s Australian Property Market Update – Latest Data, State by State September 9th 2025

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2025–26: Where Prices Are Headed After Three Rate Cuts.

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

Also Carina and Camp Hill are suburbs to target.

Located just 7-10 km from the CBD, these suburbs are experiencing an influx of young families and professionals looking for spacious living at a more affordable price point. Townhouses here offer good rental yields and future capital growth.

Stafford and Kedron have excellent access to public transport, shopping centers, and proximity to Brisbane Airport, these northern suburbs are emerging as townhouse hotspots.

They attract a mix of renters and owner-occupiers, providing strong rental yields and growth potential.

3. Apartments in Boutique Complexes

While I would avoid high-rise apartments in large complexes, boutique “family friendly” apartments (typically in complexes of 4 - 20 units) in well-located suburbs are expected to perform well in the next few years.

They cater to renters and owner-occupiers who want the convenience of apartment living without the congestion of larger complexes.

Investors who can’t afford a house or townhouse should consider 2 bedroom apartments with spacious layouts, quality finishes, and amenities such as balconies, secure parking, and access to nearby lifestyle facilities like cafes, restaurants, and public transport.

The trendy riverside suburbs of New Farm and Teneriffe are always in high demand among young professionals and downsizers looking for lifestyle-driven apartment living.

With their proximity to the CBD, high-end dining options, and recreational facilities, boutique apartments here have strong rental demand and capital growth potential.

West End and Highgate Hill are known for their vibrant, eclectic vibe and continue to attract renters and buyers looking for a lively urban lifestyle.

Boutique apartments in these suburbs perform well due to their proximity to the CBD, cultural attractions, and entertainment options.

The northern inner-city suburbs of Albion and Wooloowin are rapidly gentrifying, with infrastructure upgrades and new developments attracting renters and owner-occupiers. Boutique apartments in these areas provide an affordable entry point with good long-term growth prospects.

Best Brisbane Suburbs to Watch in 2025

Here are a few key areas with long-term growth potential:

Inner Ring

-

Paddington, Red Hill, Highgate Hill – lifestyle, character homes, close to CBD

-

New Farm, Teneriffe – prestige, river proximity, walkability

Middle Ring

-

Tarragindi, Holland Park, Ashgrove – family-friendly, leafy, great schools

-

Chermside West, Everton Park – strong value, infrastructure access

Growth Corridors

-

Mitchelton, Nundah, Carina – gentrifying areas with community investment

-

Woolloongabba – Olympic precinct uplift potential

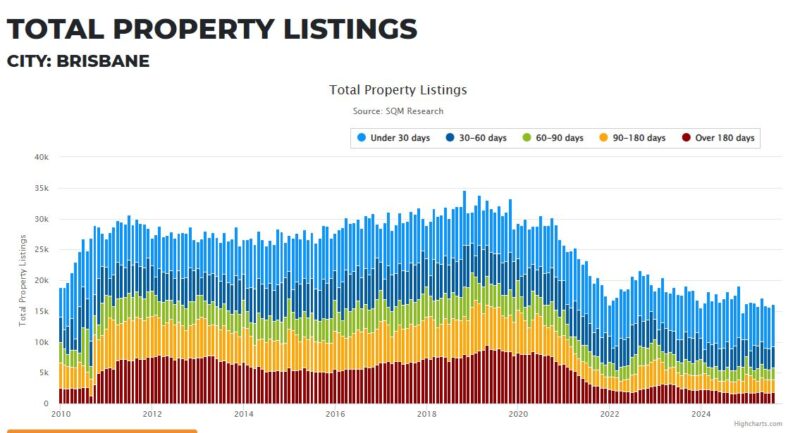

What's happening in the Brisbane property market?

Source: SQM Research

Moving forward, Queensland has been tipped to have more million dollar suburbs than Victoria by the end of 2025, according to analysis by Ray White.

Of the six states and two territories, Queensland is the fastest growing with its count of $1 million suburbs growing by 25 times over the last decade from just seven to 174.

Second in terms of growth rate is ACT with an 11 times growth in count of $1 million suburbs from just six in 2014 to 70 in 2024.

Assuming the growth rate of the last decade maintains its trend for the next 12 months, we can expect around 99 new suburbs to pass the $1 million mark.

Thirty of these will come from New South Wales, 24 from Queensland, and 18 from Victoria, which means Queensland has a very high probability of overtaking Victoria as the state with the second most count of million dollar suburbs.

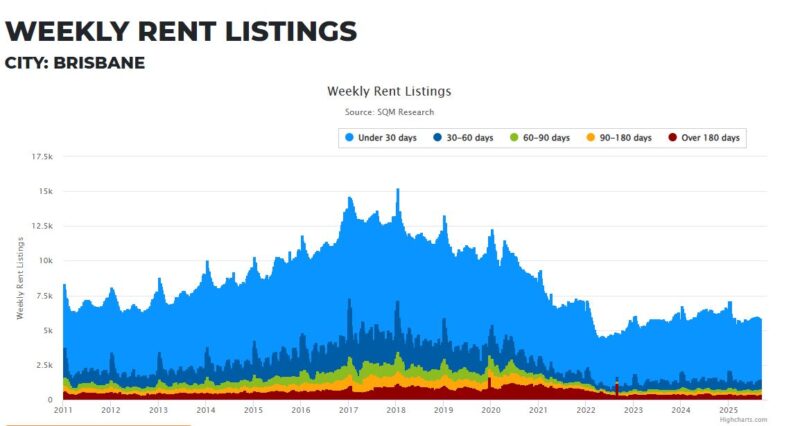

Brisbane’s rental markets remain exceptionally tight

Brisbane's rental markets remain tough for tenants with rising rents and continuing near record-low vacancy rates for both houses and units.:

Source: SQM Research

Like everywhere else in the country, Brisbane’s rental market is in crisis.

The city has seen significant investment in recent years, and many people have moved to Brisbane to take advantage of job opportunities and high quality of life.

But a migration surge has led to an increased demand for rental properties, which has kept the vacancy rate low.

While the current vacancy rate in Brisbane may be good news for landlords, it only serves to exacerbate the city’s already pressurised rental market with renters increasingly struggling to look for affordable housing.

Source: SQM Research

2024 is unlikely to provide any relief for tenants with new home building levels remaining chronically recessed despite government policies designed to reduce surging migration.

Key trends for Brisbane’s housing market 2025.

Brisbane’s many infrastructure projects, including the Cross River Rail, Brisbane Metro, and preparations for the 2032 Olympics, are transforming the city.

Suburbs benefiting from these developments are likely to see increased demand and continued capital growth.

At the same time Brisbane continues to attract residents from Sydney and Melbourne due to its more affordable housing, lifestyle advantages, and employment opportunities. This trend is driving demand in family-friendly and lifestyle-focused

Suburbs undergoing urban renewal and gentrification tend to outperform, as they attract a new demographic of more affluent residents (both owner occupiers and tenants) , which in turn boosts demand for housing and rental properties.

Moving forward there will be a flight to quality properties and an increased emphasis on livability.

That explains why we’re seeing robust demand for A-grade homes and investment-grade properties, particularly in lifestyle locations, with many holding their values well.

Buyers will be willing to pay a little more for properties with a little more space and security, but it won’t be just the property itself that will need to meet these newly evolved needs – a “livable” location will play a big part too.

To many, livability will mean a combination of:

- Proximity – to things like parks, shops, amenities, and good schools

- Mobility – access to good public transport (even though this may be less important moving forward) or a good road system

- Access to jobs

Another driver of strong capital growth in Brisbane is school zones.

As part of their property decision-making process, many parents and investors consider the geographical location of a potential property in relation to a school catchment zone.

When people are looking for a home, they’re looking for a lifestyle, and education is a big part of that picture.

Brisbane’s migration and population growth vs. property prices

Brisbane and Queensland can thank a huge influx of internal migrants for the robustness of their property markets over the last few years – between the pandemic, lockdowns, and a surging property market many Australians, particularly from Victoria and NSW, flocked northwards to our Sunshine State in search of more affordable property in lifestyle suburbs.

And this lifestyle move still holds true today.

Source: ABS data

Popular areas of the Gold Coast and Sunshine Coast have enjoyed strong demand considering the increased flexibility of being able to work from home and commuting to the big smoke less frequently.

At the same time property investor activity has been strong, particularly for houses, not only coming from locals but from interstate investors who see a strong upside in Brisbane property prices as well as favourable rental returns.

Of course, there is not one Queensland property market, nor one south-east Queensland property market, and different locations are performing differently and are likely to continue to do so.

Queensland recorded a population growth rate of 2.3% in the 12 months to 30 June 2024, above the national average (2.1%).

And there is more forecasted population growth on the horizon.

Federal government forecasts suggest that Queensland’s population is expected to grow by more than 16% by the time Brisbane hosts the Olympic Games in 2032.

And the population spread in Australia’s most decentralised state is tipped to sway towards the city, with most Queenslanders expected to live in Greater Brisbane by the time the Olympic flame is lit at the Gabba.

Greater Brisbane is expected to grow faster than the rest of Queensland, with a rate of 1.9% projected for the capital in 2022-23, compared to 1.4% for the rest of the state.

That means that Queensland’s population is set to boom in the coming decades, from the current 5.4 million people to as much as 8.27 million by 2046.

Brisbane’s fundamentals are very strong

It’s not just Brisbane’s population and migration growth that is holding up the state’s economy, the remainder of the city’s underlying fundamentals are also very strong.

CommSec's State of the States report assesses economic performance across Australia and shows that on an aggregate basis our resources-focused states Queensland and Western Australia both have the strongest annual economic momentum, supported by robust housing markets and solid population growth.

Queensland is now in first spot with Western Australia slipping to second.

There is little to separate the commodities and tourism-heavy states, with Queensland ranked first or second on five of the eight key economic indicators.

While Brisbane’s property market was significantly more affordable before the recent property boom, it still represents a valuable benefit to buyers who are looking to purchase at a time when interest rates are falling and we move into the next phase of the property cycle.

And the impending 2032 Olympics, hosted by Brisbane, will only serve to put even more pressure on the city.

The need for upgraded infrastructure and transport in Brisbane, the Gold Coast, and the Sunshine Coast will likely put a rocket under Brisbane’s property market.

Why?

Because infrastructure spending is one of the most powerful forces in residential real estate – it can transform local economies and generate real estate booms.

That’s because major infrastructure projects can elevate the appeal of locations by improving the accessibility or amenity of an area and they can also generate economic activity and jobs during construction.

Final Thoughts

The Brisbane property market continues to offer compelling investment opportunities—but only for those who take a strategic, research-backed approach.

With strong population growth, infrastructure investment, rising rental demand, and the Olympics ahead, Brisbane has all the ingredients for sustained capital growth and wealth creation.

But success won’t come from following the herd or buying in hype-driven locations.

It will come from careful selection, long-term vision, and expert advice.

Ready to Invest in Brisbane?

If you’re looking to grow your wealth safely and strategically, now’s the time to talk to the team at Metropole Brisbane.

Our Brisbane-based buyer’s agents and property strategists understand this market inside out—and we’re here to help you make the right move.

👉 Click here to schedule your complimentary Wealth Discovery Chat