Key takeaways

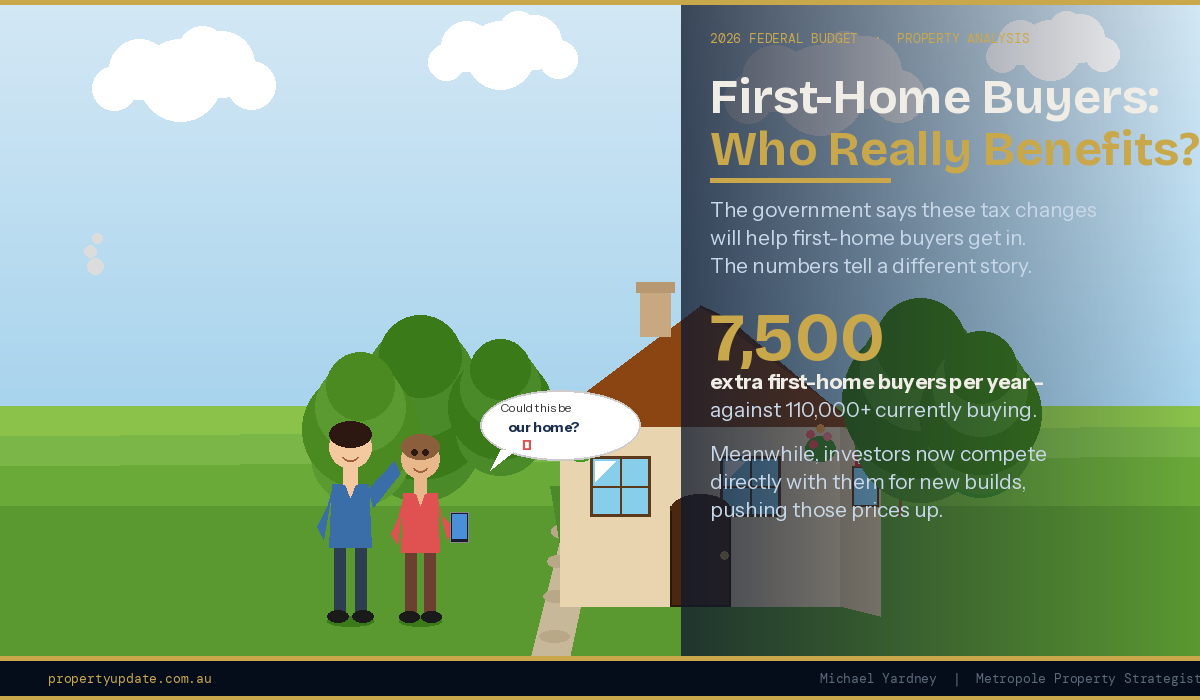

The Budget changes may sound like they help first-home buyers, but the actual impact is likely to be modest, with estimates suggesting only around 7,500 additional first-home buyers a year.

By pushing investors toward new builds, the policy may make them compete more directly with first-home buyers for the same properties.

More demand for new townhouses, apartments and house-and-land packages could push prices higher in the very market segment first-home buyers are being encouraged to enter.

Australia’s housing problem is fundamentally a supply problem, and tax changes alone won’t create enough homes in the locations where people want to live.

If investor confidence falls, rental supply could tighten further, making it harder for renters to save a deposit and eventually buy their own home.

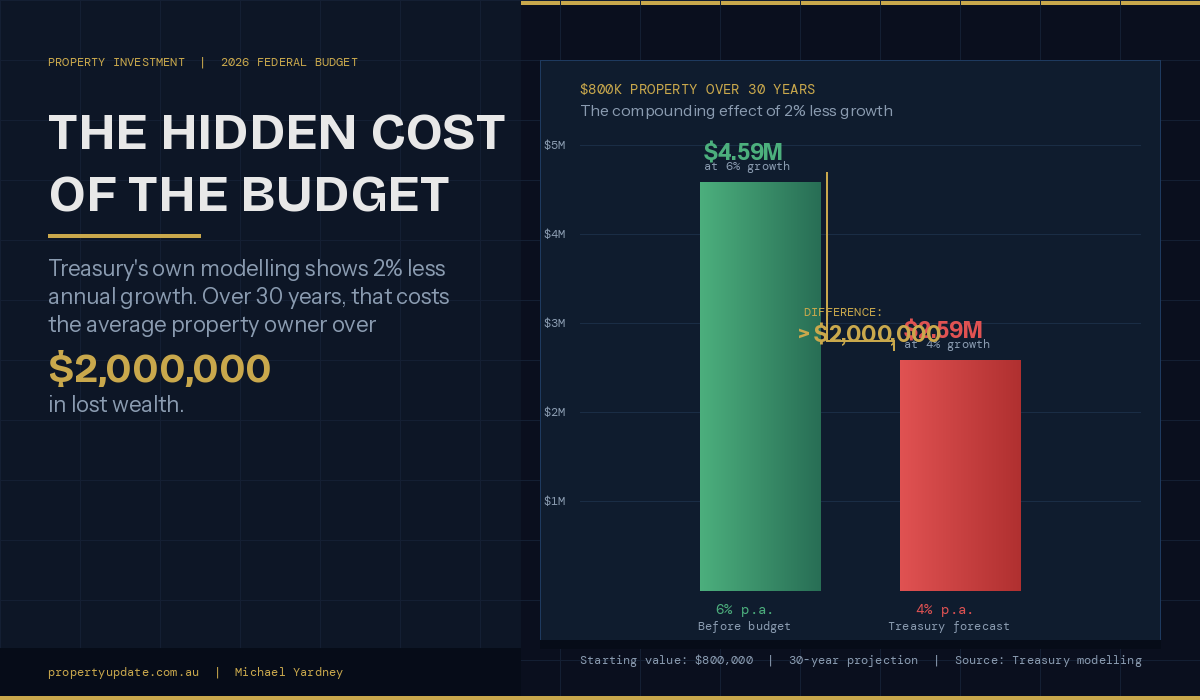

A small reduction in long-term property growth can have a large effect over time, because compounding can turn a 2% annual difference (Budget forecast) into a substantial wealth gap over decades.

Today’s first-home buyers become tomorrow’s homeowners, investors, retirees and parents helping the next generation, so policies that reduce long-term housing wealth may eventually affect them too.

Property is not just shelter in Australia - it is also a major source of household wealth, retirement security, business funding and intergenerational support.

The real solution is more housing supply, faster planning approvals, lower construction costs, better infrastructure and a serious rethink of inefficient taxes like stamp duty.

The Budget may have changed the rules, but Australia still needs more homes, more investment, more confidence and better long-term thinking.

The government’s message sounds simple enough: make property investing less attractive, reduce the advantages investors supposedly have, tilt the playing field back toward first-home buyers, and more young Australians will finally be able to get a foot on the property ladder.

On the surface, that sounds fair, and I can understand why many frustrated first-home buyers would welcome it, because when you’ve been saving for a deposit while property prices keep moving ahead of you, it’s easy to believe that investors are the main reason you can’t get into the market.

But housing markets are rarely that simple, and while this Budget may make for an appealing political story, I believe it has created a number of side effects that have not been properly explained to Australians.

In fact, the more I think through the likely consequences, the more convinced I am that these changes may not help first-home buyers in the way the government is suggesting and may actually make life harder for many of them.

The first-home buyer promise sounds bigger than it really is

The government has suggested that its reforms will help 75,000 Australians into home ownership over the next decade, which sounds like a large number when it’s presented in a press release or repeated in a news headline.

But when you slow down and put that number into perspective, it becomes much less impressive.

Seventy-five thousand buyers over 10 years works out to around 7,500 additional first-home buyers a year, while Australia already has roughly 110,000 to 120,000 first-home buyers entering the market each year, depending on interest rates, lending conditions, government grants, confidence levels and where we are in the property cycle.

So even if Treasury’s estimate turns out to be correct, and it still needs to be treated as an estimate rather than a certainty, we are talking about a relatively small addition to the overall first-home buyer market.

In other words, this is unlikely to shift the needle in any meaningful way.

And that’s before we even get to the more important point, which is whether the modelling properly accounts for how investors, developers, lenders and buyers will actually respond once the rules change, because markets respond, people change their behaviour, capital moves, and that’s where the government’s neat little theory starts to look much less convincing.

Investors may end up competing more directly with first-home buyers.

Tip: One of the most obvious unintended consequences is that if negative gearing is restricted to new builds, many investors who still want tax benefits will be pushed toward new properties.

That means investors may increasingly compete with first-home buyers for the same stock, and remember, first-home buyers are already being encouraged into new builds through grants, stamp duty concessions, shared equity schemes and other government incentives.

So what happens when the government gives investors a strong tax reason to chase the same kind of property?

Demand increases, and when demand increases without a matching increase in supply, prices rise.

That’s not political ideology - that’s basic economics.

The government seems to be assuming that investors will help fund new supply by buying new properties, and in some cases that may happen, but there is a very big difference between encouraging genuine new construction and pushing more buyers into the same limited pool of newly completed or soon-to-be-completed dwellings.

In practice, investors may simply bid up the price of the very properties first-home buyers are being told to buy.

That means a young buyer looking at a new townhouse, a new apartment, or a house and land package could find themselves competing against an investor who is prepared to pay more because the tax outcome looks better.

Note: And that is the great irony of this policy, because a Budget measure designed to help first-home buyers may end up making the first-home buyer segment more expensive.

Developers are not charities, and if they know investors receive a better tax outcome from buying new stock, many will price that benefit into the product, which means the concession may not flow cleanly to the buyer at all. Part of it may simply be capitalised into the purchase price.

This is one of the reasons I’ve always warned investors not to buy a property just because it comes with a tax benefit, and the same warning applies to first-home buyers, because a government incentive can help with the purchase, but it can also distort the price.

Sometimes, the person who benefits most from a government incentive is not the buyer. It is the seller.

Buying new properties in outer suburbs, or off-the-plan apartments in large blocks, have proven to be very poor long-term investments.

And of course, if an investor who's bought a new property wants to sell in the future, their market will be limited, as other new investors will want to buy new property, not their established property.

The government is trying to solve a supply problem with a tax change.

Australia’s housing crisis is not mainly caused by investors claiming tax deductions, even though that is a convenient story for politicians to tell.

The bigger problem is that we have had years of underbuilding, slow planning approvals, rising construction costs, labour shortages, infrastructure bottlenecks, high development charges, and population growth running well ahead of dwelling completions.

So while it may be politically convenient to point the finger at investors, the real problem is that we simply have not been building enough homes in the locations where people want and need to live.

Punishing one group of buyers does not magically create more dwellings, and it may actually do the opposite if it reduces confidence, discourages investment, or pushes capital into other asset classes.

This is where the policy becomes particularly concerning, because if we help a relatively small number of first-home buyers enter the market but, at the same time, reduce investor participation and weaken rental supply, which will make developers less confident about future demand, then we haven’t really improved affordability.

We may have just moved the pressure from one part of the market to another.

Every housing market has two sides: there are buyers and there are renters, and many first-home buyers are renters before they buy.

That means if a policy makes renting harder or more expensive while they are trying to save a deposit, it may actually delay their ability to become homeowners.

That’s the part of the debate too many commentators keep skipping over, because you can’t separate the first-home buyer market from the rental market. They are joined at the hip.

A small change in growth can mean a very large change in wealth

Another issue that has been underplayed is the long-term impact of weaker property price growth.

Most of the public discussion has focused on whether these changes might make homes slightly cheaper, or at least slow future price growth enough to make housing more accessible.

At first glance, a small reduction in annual growth may sound harmless, and some people may even think it sounds desirable, especially if they are currently locked out of the market.

Now, the Budget suggests that future home price growth may decrease by around 2% per annum, but anyone who understands investing knows that small changes in annual growth rates become very large differences when they are compounded over time.

Let’s take a typical property that a first home buyer may purchase valued at $800,000.

- If that property grows at 6% per annum over 30 years, it would be worth approximately $4,594,793.

- But if it grows at 4% per annum over the same period, it would be worth approximately $2,594,718.

That is around $2 million less in wealth from one property.

Now, I’m not suggesting that every property will grow at 6%, or that every property will grow at 4%, or that Treasury has modelled that exact 30-year outcome.

Clearly, some areas are going to outperform, as they always have, while other areas are going to languish.

I think the divergence between A and B grade locations and C and D-grade properties is only going to widen. location will be even more important moving forward with regard to capital growth

What I am suggesting is that this is the type of conversation we should be having, because compounding is not intuitive to most people, and the long-term consequences of slower asset growth can be enormous.

A 2% difference (as the Budget is forecasting) may not sound like much in the first year, and it may not even feel particularly dramatic after five years, but over a generation it can completely change a household’s financial position.

That matters because property in Australia is not just shelter.

For most Australians, it is their largest asset, the foundation of their net worth, the security behind their retirement, and the asset that allows them to borrow, invest, start a business, help their children, downsize, fund aged care, and avoid relying entirely on the pension.

So if government policy structurally reduces the wealth-building capacity of residential property over time, the consequences won’t only be felt by today’s investors.

They will also be felt by tomorrow’s homeowners, and many of those homeowners are today’s first-home buyers.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

Today’s first-home buyers become tomorrow’s property owners. This is one of the biggest blind spots in the debate.

The government is presenting this as though there are two fixed groups in Australia: on one side, first-home buyers, and on the other, property investors and existing homeowners.

But that’s not how life works.

A first-home buyer becomes a homeowner the moment they buy, and some of them will later become investors, some will use their equity to upgrade to a better home, some will use their home as security to start or expand a business, some will eventually help their children into the market, some will downsize in retirement, and some will rely on their home equity to fund medical costs, aged care, lifestyle choices, or financial independence later in life.

So if these policies reduce long-term wealth creation through property, they may eventually hurt the very people they are supposed to help.

A young Australian might welcome a policy that slows property growth before they buy, and I understand that, because when you are outside the market looking in, rising prices feel like the enemy.

But the moment they own a home, they are exposed to that same slower growth.

Of course, that doesn’t mean we should want runaway property prices or a market where younger Australians are permanently locked out, because that would be bad for society, bad for the economy, and bad for the property market itself over the long term.

But we also need to be honest enough to recognise that structurally weaker asset growth has consequences.

A country where households build less wealth over time is not necessarily a fairer country. It may simply become a poorer country.

Property is tied to Australia’s retirement system

Australia’s retirement system quietly assumes that most people will own a home by the time they stop working, which is why home ownership matters so much.

A retiree who owns their home outright has a very different financial profile from a retiree who is still renting.

The homeowner has security, lower housing costs and an asset base that gives them options, while the renter is exposed to market rents, lease insecurity and greater dependence on government support.

So when we talk about property tax reform, we shouldn’t only ask whether it helps a relatively small number of additional buyers into the market over the next decade.

We should also ask what it does to household wealth over 10, 20 and 30 years.

Because if Australians build less wealth through property, there are consequences.

They may retire later, spend less, invest less, rely more heavily on government support, have fewer choices, and have less ability to help their children. Over time, that means lower living standards.

That’s why the Budget’s side effects matter so much.

Property is deeply embedded in the Australian economy, not just because people live in homes, but because housing wealth supports retirement security, rental supply, small business borrowing, consumer confidence and intergenerational financial support.

You can’t pull one lever in the housing market and pretend nothing else moves.

Note: Did Treasury model the long-term wealth effect? This is the question I’d like to see answered.

Did Treasury model what happens to the broader economy if Australians build significantly less property wealth over the decades ahead?

I’m not just talking about what happens to median house prices over the short term, or how many extra first-home buyers might enter the market over 10 years, or whether rents move a little or a lot in the first few years.

I’m talking about what happens if the average Australian household has meaningfully less housing wealth by the time they retire.

What happens to pension reliance, consumer spending, small business formation, family support, inheritances and aged care funding?

What happens when parents have less equity to help their children into the market, and what happens to future government budgets if more retirees need more financial support for longer?

These are not fringe questions. They go to the heart of Australia’s long-term prosperity.

The political risk is that homeowners eventually work this out

Right now, much of the political focus is on first-home buyers, and that is understandable because many of them are genuinely frustrated.

But the critical mass in Australia is still made up of people who own residential property, including homeowners, mum and dad investors, retirees, upgraders, downsizers, small business owners, and parents who hope to help their children.

At some point, many of these people may start to realise that this Budget is not just about so-called wealthy investors. It is about the asset base of ordinary Australians.

And once that becomes clear, the politics could shift.

Most Australians don’t think of their home as a tax shelter, because they think of it as the reward for decades of work, saving and sacrifice.

They think of it as their financial safety net. They think of it as the asset that gives them choices.

So if voters come to believe that government policy is deliberately weakening the long-term wealth-building power of residential property, the backlash may be much broader than expected.

The real solution is still supply

None of this means we should ignore first-home buyers, because they do need help, but we need to help them in ways that deal with the actual problem rather than creating new distortions.

We need more homes in the locations where people want and need to live, faster planning approvals, lower construction costs, better infrastructure delivery, and fewer unnecessary costs loaded onto the creation of new dwellings.

We also need to rethink stamp duty, which remains one of the most inefficient and damaging taxes in Australia, and we need to encourage long-term rental supply rather than discourage it.

Most importantly, we need to stop pretending that making investors less confident will somehow make housing more affordable.

If investors leave the market, renters feel the pain first. If developers can’t make projects stack up, supply falls. If first-home buyers and investors are pushed into the same new-build market, prices rise in that segment.

And if households build less wealth over time, Australia becomes less prosperous.

That is not real reform, it is a side effect being sold as fairness.

The bottom line

I believe these unintended consequences will become clearer over time, and when they do, the political conversation around this will shift.

The question is how much damage gets done in the meantime, particularly for younger Australians and first-home buyers who are being told this budget works in their favour, without being shown the full picture of what it costs them once they own property themselves.

Because in the end, property is not just about investors, and it is not just about first-home buyers either.

It is about the financial future of millions of Australians.

When governments interfere with the wealth-building engine that underpins so many households, they need to be very careful about the consequences they create.

The Budget may have changed the rules, but it has not changed the fundamentals, because Australia still needs more homes, more investment, more confidence and more long-term thinking.

And that is where the real conversation should begin.

If you'd like to talk through how these changes affect your specific situation and what your best strategy looks like from here, the team at Metropole is here to help.

We've been helping Australians build and protect long-term property wealth through every cycle, every policy change and every market shift for decades, and this one is no different.

You can book a time with one of our strategists by clicking here