Key takeaways

The May 2026 Budget has introduced significant changes to negative gearing and capital gains tax, taking effect from 1 July 2027 - but existing investors are largely protected through grandfathering provisions.

From 1 July 2027, negative gearing on established residential properties purchased after Budget night (12 May 2026) will be limited - rental losses can only be offset against property income, not wages or other income.

The 50% CGT discount will be replaced by cost base indexation and a 30% minimum tax on capital gains from 1 July 2027, for assets other than new builds.

New builds remain fully exempt - investors who buy newly constructed properties can still negatively gear and choose between the old or new CGT treatment.

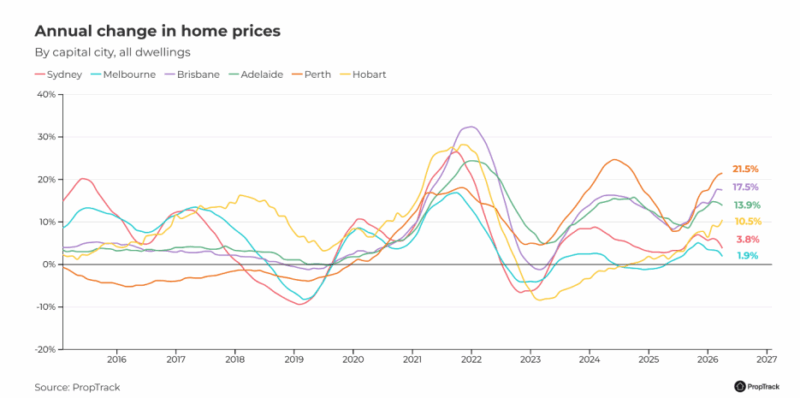

Price growth was already moderating before the Budget, reflecting the later stages of the current cycle, and the changes are expected to slow growth further over the medium term.

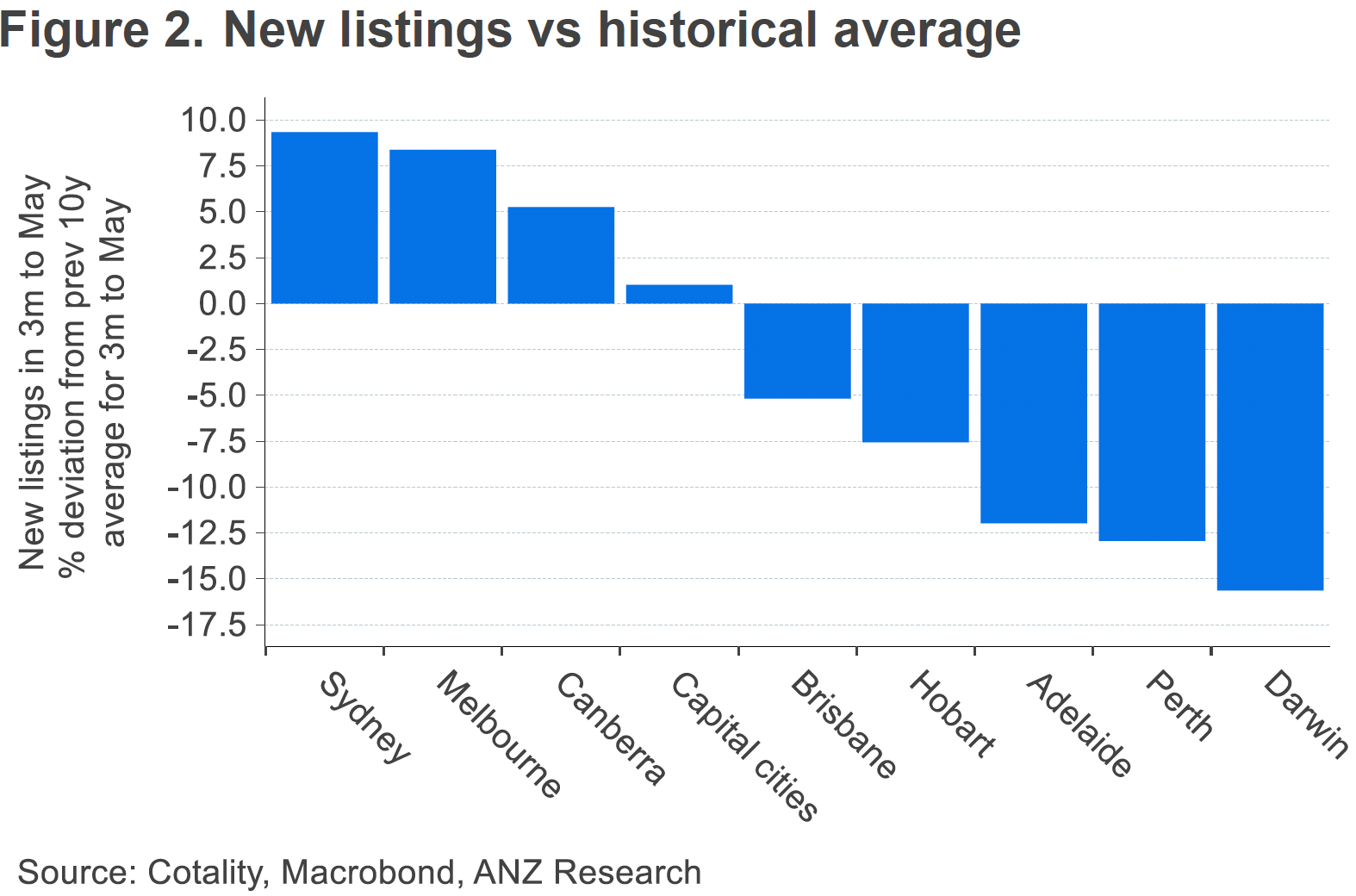

Auction clearance rates and listing volumes are the key indicators to watch in the short term, particularly in Sydney and Melbourne where listings are already running above their long-term averages.

Over the long term, the fundamentals haven't changed - population growth, housing undersupply, and Australia's wealth trajectory will continue to underpin property values.

Strategic investors who buy well-located, investment-grade properties and hold them for the long term will continue to outperform.

CBA, NAB and ANZ all expect the RBA to leave the cash rate unchanged for the rest of this year.

Westpac expects two further cash rate hikes in August and September this year, followed by cuts, but not until 2028.

The Australian property market in 2026 has entered genuinely new territory, with a another rate rise from the Reserve Bank and the most significant tax changes to property investment in nearly three decades landing within weeks of each other.

The three RBA rate rises this year delivered the shortest and shallowest rate-cutting cycle since inflation targeting began to a close.

Then in May, the federal Budget announced that from 1 July 2027, negative gearing on established residential properties bought after Budget night will be restricted, and the 50% CGT discount will be replaced by cost base indexation with a 30% minimum tax on capital gains.

That's a lot to absorb, and I understand why many investors are trying to work out what it all means.

My read is that the market was already moderating before any of this happened.

Price growth had been slowing since early in the year across most capital cities, auction clearance rates had been easing, and we were clearly moving through the later stages of a long growth cycle.

The Budget added another layer of complexity, but it doesn't rewrite the fundamentals.

I still believe property values will continue rising over the medium term, because the forces that drive prices in the long run - population growth, a chronic housing shortage, rising national wealth, and strong employment - haven't gone anywhere.

What has changed is the investment calculation for buyers of established properties going forward, and the landscape will look different for different types of buyers depending on their circumstances, what they're buying, and when they bought it.

Existing investors whose properties were purchased before Budget night are fully grandfathered, so nothing much changes for them.

New builds remain completely exempt from the new rules.

The people who need to think hardest about this are those planning to buy established investment properties from here.

As always, the markets will be fragmented - and I see the rest of 2026 playing out in two distinct phases, with the Budget and higher interest rates adding weight to the second half in particular.

Let me walk you through what the data is actually showing, what the tax changes really mean in practice, and where I see the best opportunities from here.

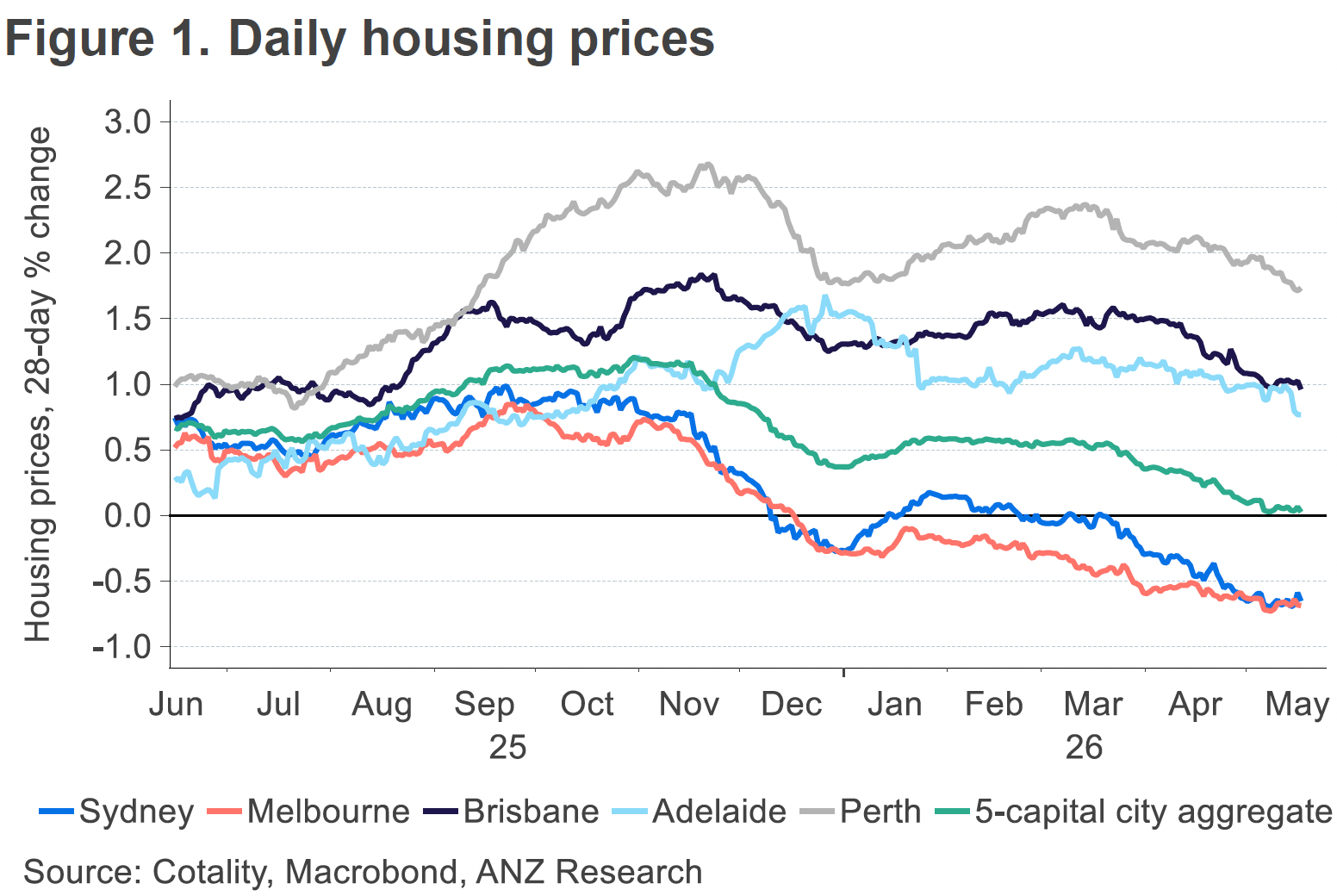

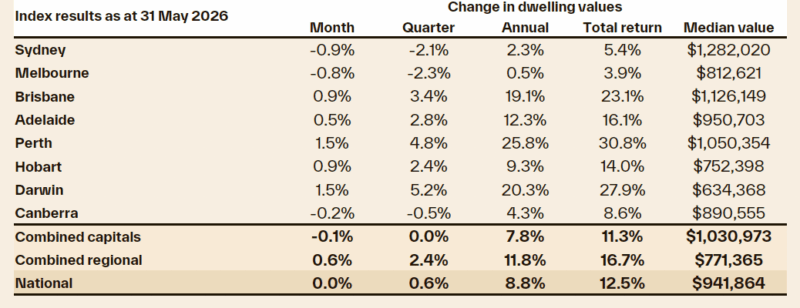

Cotality’s national Home Value Index was flat in May (0.0%), with the housing cycle continuing to weaken across most markets.

Beneath the flat national result, Sydney (-0.9%) and Melbourne (-0.8%) are leading the downturn.

Home prices nationally were flat in May, after a modest decline in April, according to the latest PropTrack data.

Home price growth has clearly stalled as the effects of this year’s consecutive rate hikes flow through.

Rather than seeing this as the beginning of a slowdown, I see this as a normal seasonal adjustment because the underlying forces that drove property price growth last year will continue into this year.

Of course, each state is at its own stage of the property cycle and within each capital city there are multiple markets.

While regional property markets became popular with homebuyers wishing to escape Covid a couple of years ago, and more recently regional markets were attractive to investors because of their comparatively lower prices, over the long term capital city property markets have outpaced regional areas and this trend is likely to continue.

Overall, persistently low supply relative to demand are supporting housing values despite high interest rates, ongoing cost of living pressures, worsening affordability pressures and a deeply pessimistic level of consumer confidence.

The gap between capital city house and unit values has widened substantially.

Capital city house values rose almost 3 times as much as unit values since the onset of Covid ... but the gap is narrowing across most cities.

And after underperforming throughout the pandemic period, unit prices recorded stronger growth for much of 2025 as affordability constraints will mean more Australians trade backyards for balconies and courtyards this year.

The good news is that this creates a window of opportunity, as one can now buy established family friendly apartments considerably below replacement cost.

What the May 2026 Budget means for property investors

The May 2026 federal Budget was the most significant shake-up to property taxation in nearly three decades, and I've had a lot of questions from investors trying to work out what it really means for them.

Let me cut through the noise and give you the practical picture.

The government has announced two major changes that will take effect from 1 July 2027.

First, negative gearing on established residential properties will be restricted, so rental losses can no longer be offset against salary or other income. Instead, those losses will be quarantined and deferred to offset only residential property income or future capital gains.

Second, the 50% CGT discount will be replaced by cost base indexation and a 30% minimum tax on capital gains.

Before you panic, here are the parts that matter most to investors who already own property.

If you purchased your investment property before 7:30pm on Budget night, 12 May 2026, absolutely nothing changes for you.

The grandfathering provisions are generous and deliberate. You can continue to negatively gear exactly as you always have, and your CGT discount arrangements remain intact for gains up to 1 July 2027.

The new rules apply to established properties purchased from Budget night onwards. And even then, the impact varies considerably depending on the size of your rental loss and your marginal tax rate.

New builds are a different story entirely. Properties classified as newly constructed - including off-the-plan apartments, new house and land packages, and newly constructed stock - remain fully exempt.

Investors in new builds can still negatively gear under current rules and choose whichever CGT treatment suits them better.

So while the headlines will make this sound catastrophic for property investment, the reality is considerably more nuanced.

What will this actually do to property prices?

ANZ Research has analysed the budget changes and concluded that, over the long term, the effect on property price growth is likely to be only modest.

That aligns with my own view, and here's why.

Price growth was already starting to slow across most Australian cities before the Budget even landed, reflecting the natural end stages of a long growth cycle.

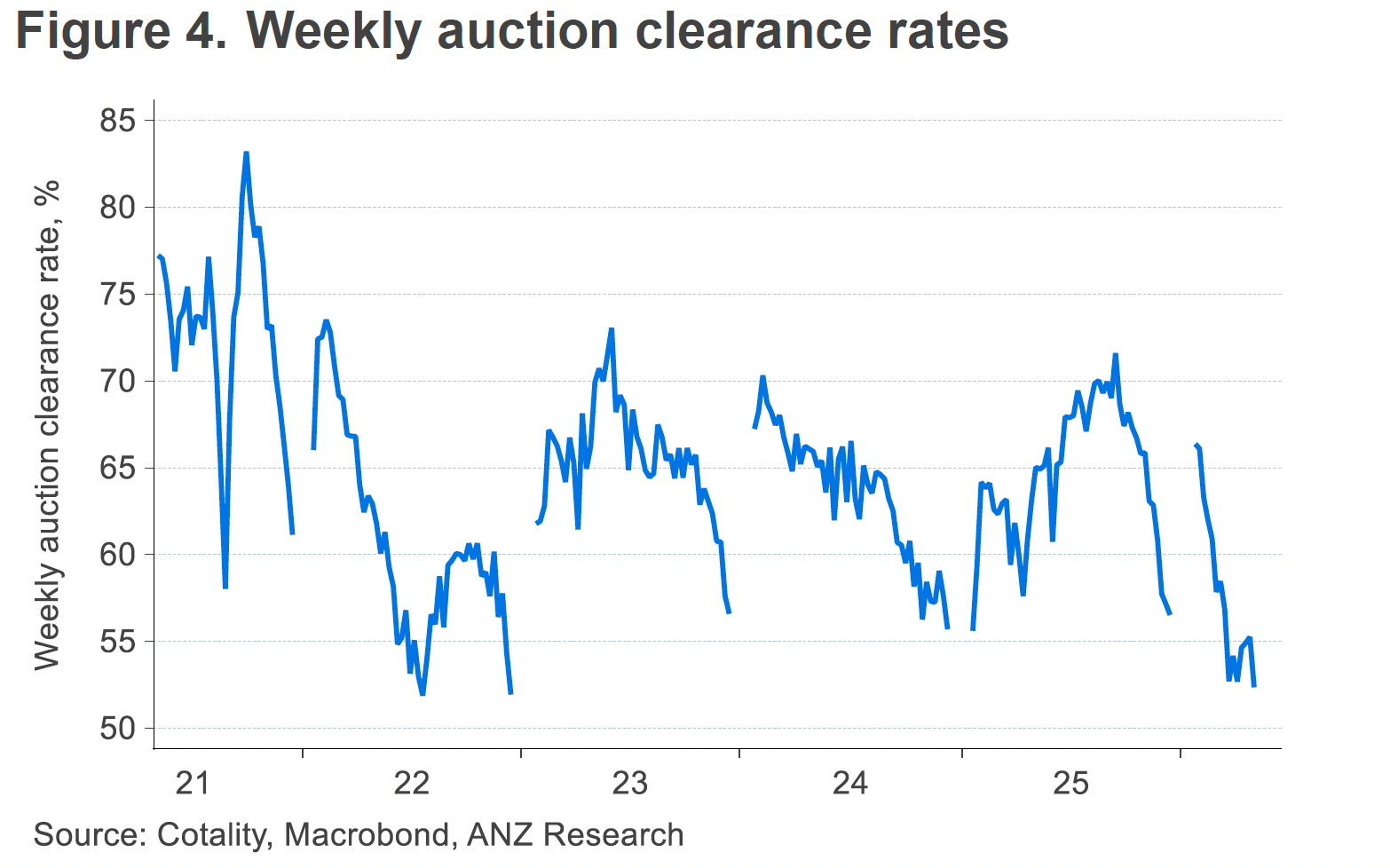

Auction clearance rates have been slipping gradually since late 2025, and listings in Sydney and Melbourne have crept above their long-term averages.

The Budget estimates suggest growth could moderate by around 2%. But that won't apply equally to every market or every price bracket. As always, there isn't one Australian property market.

The chart above shows that Sydney and Melbourne were already losing momentum heading into 2026, while other cities like Adelaide and Perth held firmer. The budget is one more piece of the picture, not the whole story.

In the short term, watch the "in-time" indicators closely - particularly auction clearance rates and total listings. Those will tell you more about buyer and seller behaviour than any single policy announcement.

On the supply side, there's actually a case to be made that the grandfathering provisions could keep a lid on listings from existing investors.

If current owners of established properties know they're protected under the old rules as long as they hold, many will simply hold longer rather than sell.

In a market already running lean on stock in the right suburbs, that dynamic could soften any downward price pressure considerably.

Sydney and Melbourne are the outliers, where listings are running above their long-term norms.

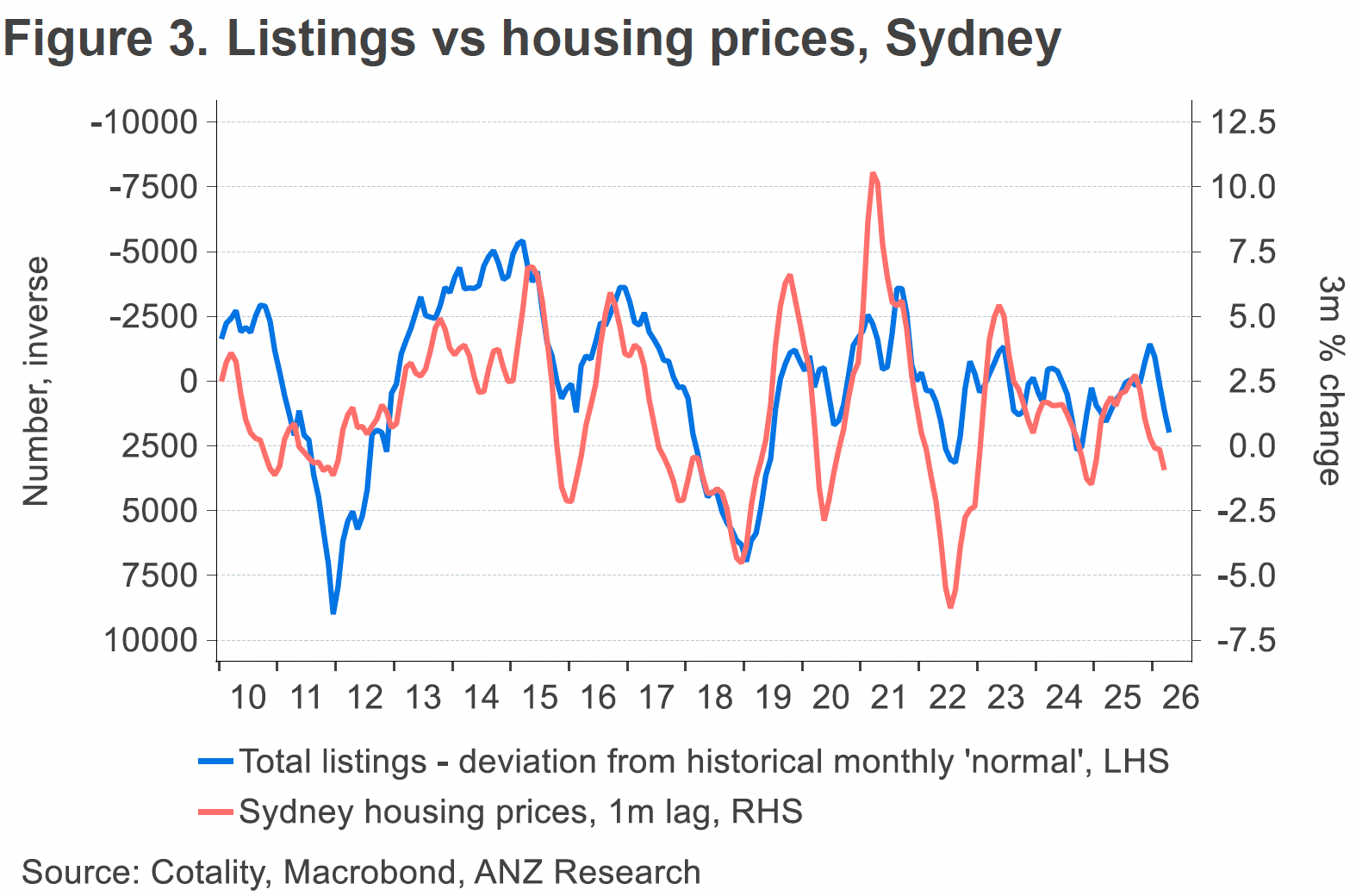

That's already weighing on prices in those two cities. The relationship between listing volumes and house prices in Sydney over the past 15 years makes this very clear.

The deeper point, which gets lost in all the budget commentary, is that macro factors - particularly the direction of interest rates - will matter just as much to where prices go from here.

A falling rate environment, which most economists still expect through 2027, provides a structural offset to the demand-side impact of the tax changes.

So what's ahead?

This will create a more subdued tone in the second half of the year, with growth diverging sharply by location and property quality.

Tip: The most desirable suburbs - the inner- and middle-ring, gentrifying, high-amenity, high-income areas - are positioned to outperform in the long term.

These suburbs benefit from scarcity, strong local wages growth, and lifestyle appeal, and they sit at the heart of the 20-minute neighbourhood trend highlighted in your report.

Outer suburban markets, by contrast, will feel the impact of affordability most acutely. With abundant supply, weaker wage growth, and limited lifestyle infrastructure, they will likely underperform as the year progresses.

Well-located houses will remain the strongest performers, but “family-friendly” established apartments in lifestyle suburbs remain attractive for budget-constrained buyers who still want access to good schools, infrastructure, and amenity.

Regardless of short-term cooling in the second half, property prices will continue to rise as the long-term drivers remain intact:

-

Continued population and household formation

-

Growing national wealth, albeit unevenly distributed

-

Persistent under-supply in desirable suburbs

-

Investors who focus on scarcity, land value, gentrifying areas, and value-add potential will continue to outperform. As your report emphasises, success in this environment is less about timing the cycle and more about selecting the right property in the right location and holding for the long term.

The pool of buyers for established investment properties will likely be smaller going forward, and that will apply some modest downward pressure on prices at the margin, particularly in the investment-heavy segments of the market.

But well-located, investment-grade properties - the kind I've always argued you should be buying - will remain highly sought after by owner-occupiers, who are completely unaffected by these changes.

Owner-occupier demand is what drives prices in the gentrifying inner and middle ring suburbs I favour, and that demand isn't going anywhere.

If anything, this is a reminder of why I've always said the investor mindset matters more than the investment.

The investors who bought quality assets, structured sensibly, and focused on long-term capital growth will be very well positioned. Those who were relying on the tax tail to wag the investment dog may need to rethink.

Apartment rents set to surge over the next few years.

Median apartment rents are likely to grow by 24% between 2025 and 2030, across Australian capital cities, according to a recent report by International Property Consultancy, CBRE.

By 2030, 92% of 2-bed apartments are forecast to have rents exceeding $700/week (33% exceeding $1000/week)

CBRE expect that capital city vacancy rates will fall further to 1.1% by 2030 from 1.8% in 2025.

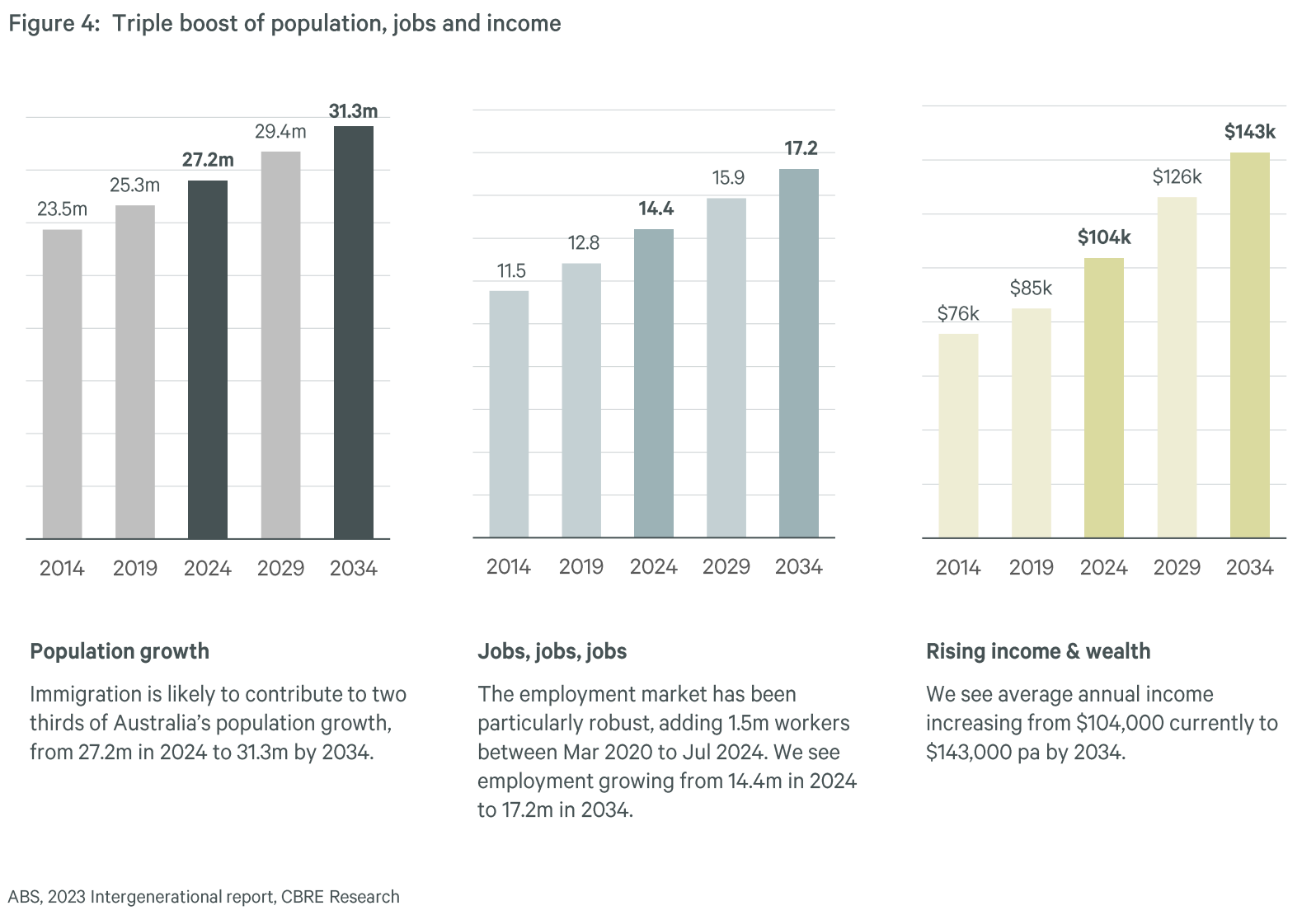

Over the next 10 years, demand for housing is expected to benefit from a triple boost: rising population (+4.1 million), rising jobs (+2.8 million), and rising income (+$39k).

CBRE estimates around $960 billion of additional income in the system to support mortgage, rent, and other living expenses.

You can always beat the averages.

While it’s likely that property price growth will continue to rise throughout 2026, the good news is that you can always beat it by investing in the right property in the right location.

Now by that, I don’t mean look for the next hotspot.

I mean buying quality properties in locations that will outperform in the long term such as gentrifying suburbs.

You see...property offers countless opportunities to improve your results through your own time, skills and knowledge – so you don’t need to settle for average.

And there’s more to it than just location. You can add value through refurbishment, or redevelopment.

What's ahead for interest rates?

The RBA has now raised the cash rate three times in 2026 - in February, March, and again in May - taking it from 3.60% to 4.35%, effectively unwinding all three of the cuts delivered through 2025.

All four major banks passed on the full 25 basis points from the May decision to existing variable-rate customers within days of the announcement.

Now the RBA is set to hit pause on further interest rises as it assesses the impact of both the war in Iran and the three cash rate hikes already inflicted on households.

This comes as Australia’s unemployment rate jumped to 4.5% in the April data, the highest seasonally adjusted rate since November 2021.

CBA, NAB and ANZ all expect the RBA to leave the cash rate unchanged for the rest of this year and for rates to fall in 2027.

Westpac expects two further cash rate hikes in August and September this year, followed by cuts, but not until 2028.

This divide highlights just how uncertain the economic outlook remains.

Inflation is still well above the Reserve Bank’s target band and global tensions are still elevated, keeping the Board firmly in wait-and-see mode.

How does this affect what buyers can borrow?

Each 25 basis point rate rise reduces the maximum borrowing capacity of an average income earner by around $12,000.

Three hikes in quick succession means a single-income buyer at average wages has lost roughly $36,000 in borrowing power since the start of 2026, and a dual-income couple has lost around $72,000.

On an average loan of $736,000, each 25 basis point increase adds roughly $120 a month to repayments. Three hikes in a row means many borrowers are absorbing an extra $360 per month compared to where they started the year.

That's real money, and it is already shaping buyer behaviour.

More buyers are gravitating toward units and townhouses rather than houses, toward the middle ring rather than the inner ring, and toward suburbs with lower price points where their reduced borrowing capacity still gets them access to the market.

| Borrower | Feb hike | Feb + March + May (combined) |

|---|---|---|

| Individual (avg. wage) | -$12,000 | -$36,000 |

| Couple (2 x avg. wage) | -$24,000 | -$72,000 |

Source: Canstar. Based on owner-occupier, 30-year loan, principal and interest.

But let me put this in context... Property markets kept rising through 2022 and 2023 when the RBA delivered 13 consecutive rate rises.

The structural forces - population growth, housing undersupply, strong employment - absorbed that cycle. They'll absorb this one too, though the pace of price growth will be slower while rates stay elevated.

The investors who will feel this most are those who are highly leveraged with little buffer, and first home buyers at the outer edge of their borrowing capacity.

For investors who bought well, structured conservatively, and have equity to work with, the current environment is more a test of patience than a genuine threat to their long-term position.

And when rates do eventually turn - which they will - there will be a meaningful uplift in borrowing capacity that flows back through the market.

How can values continue rising amid high interest rates and the cost of living crisis?

Clearly affordability has decreased, but the housing markets are being underpinned by a number of factors:

- Wealthy buyers entering the market with higher deposits.

- Downsizers who had a lot of equity in their homes are buying debt free - in fact a third of properties last year were transacted with no mortgage at all.

- The bank of mum and dad and inheritances are helping many buyers with a deposit.

- The recent first home buyer incentives offered by both major political parties will increase demand at a time of lack of supply further pushing up prices, especially at the lower end of the market.

- Some buyers are buying in cheaper markets while others are buying units rather than houses.

- Rentvestors will keep buying investment properties while renting in their preferred living locations

The latest housing market stats

Here are the latest stats provided by CoreLogic for property price changes around Australia:

We also keep track of “Asking Prices” as these are a good leading indicator for the property market because they reflect the sentiment of sellers and their expectations for the future value of their homes.

Sydney Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 2,118.430 | -8.430 | -0.6% | 3.4% |

| All Units | 926.794 | -3.094 | -0.2% | 9.7% |

| Combined | 1,631.157 | -6.349 | -0.5% | 4.6% |

Source: SQM Research, June 2026

Melbourne Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,318.835 | -4.335 | -1.2% | 1.6% |

| All Units | 688.442 | 2.048 | 0.3% | 8.7% |

| Combined | 1,119.285 | -2.258 | -0.9% | 2.9% |

Source: SQM Research, June 2026

Brisbane Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,407.065 | 1.824 | -1.0% | 13.3% |

| All Units | 889.208 | -1.708 | -0.5% | 22.6% |

| Combined | 1,275.920 | 0.821 | -0.9% | 14.8% |

Source: SQM Research, June 2026

Perth Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,289.610 | 7.769 | -0.8% | 13.1% |

| All Units | 794.622 | -6.122 | -0.3% | 24.6% |

| Combined | 1,159.466 | 4.096 | -0.7 | 14.9% |

Source: SQM Research, June 2026

Adelaide Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,132.141 | 2.258 | -1.5% | 7.5% |

| All Units | 626.364 | -2.964 | 0.1% | 12.8% |

| Combined | 1,040.950 | 1.296 | -1.4% | 8.1% |

Source: SQM Research, June 2026

Canberra Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,259.573 | -0.448 | 1.3% | 7.7% |

| All Units | 611.202 | 2.541 | 0.8% | 2.0% |

| Combined | 1,012.905 | 0.318 | 1.2% | 5.9% |

Source: SQM Research, June 2026

Darwin Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 850.546 | -2.546 | 0.3% | 9.6% |

| All Units | 464.895 | -3.895 | -2.7% | 13.8% |

| Combined | 698.832 | -3.072 | -0.5% | 10.6% |

Source: SQM Research, June 2026

Hobart Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 938.740 | 0.260 | 2.3% | 11.3% |

| All Units | 551.853 | 8.047 | 3.1% | 11.1% |

| Combined | 879.455 | 1.413 | 2.4% | 11.3% |

Source: SQM Research, June 2026

National Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,085.673 | -3.417 | 0.1% | 8.6% |

| All Units | 663.594 | 2.329 | 0.7% | 13.9% |

| Combined | 993.734 | -2.220 | 0.2% | 9.3% |

Source: SQM Research, June 2026

Capital Cities Property Asking Prices

| Property type | Price ($) | Weekly Change | Monthly Change % | Annual % change |

|---|---|---|---|---|

| All Houses | 1,556.190 | -1.266 | -0.6% | 5.0% |

| All Units | 815.362 | -3.285 | -0.2% | 11.6% |

| Combined | 1,333.939 | -1.979 | -0.5% | 6.0% |

Source: SQM Research, June 2026

The fundamentals of what drives Australian property prices

Property prices are driven by a combination of factors, and as we move through property cycles, they all come together to influence whether property values rise or fall.

If you take a telescopic view, rather than a microscopic view, and look at what's ahead for housing markets over the next decade or two, the two big factors driving our housing markets will be demographics (how many of us there are, have we want to live and where we want to live) and the wealth of the nation.

But first, let’s dig a bit deeper into the key underlying factors that will be influencing our property markets in the medium term.

1. Interest rates/affordability

While many people believe interest rates are a key driver of property values, and that's why there were so many pessimistic property forecasts as interest rates rose through 2022-23, our housing markets showed considerable resilience and kept rising in value despite the 13 interest rate rises the RBA threw at us.

Of course, falling interest rates and the subsequent increased affordability are strong drivers of property price growth, but the reverse isn't true.

House prices are driven by many other factors, not just interest rates, but rates are on the way down.

2. Supply and demand

Housing supply has a significant influence over house prices in the short term: an undersupply puts pressure on prices to rise while an oversupply does the opposite.

Despite very strong population growth, we’re just not building enough new dwellings, and this has put pressure on housing supply reflected in low rental vacancy rates and higher house prices.

At the same time, the strong absorption of new listings for sale has kept total listings in the market suppressed, intensifying competition between buyers.

These factors have created a sharp shortage of housing, outweighing the negative impact of rates on prices.

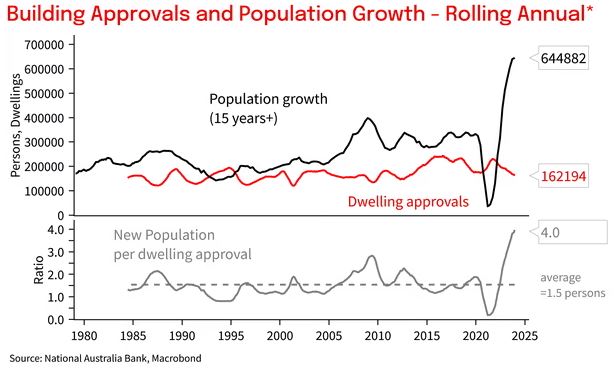

And there is no end in sight as building approvals (which are a good indication of future supply) are running at very low levels.

And just because a new apartment complex has been approved, it doesn't mean it will get built.

At the moment very few new complexes are coming out of the ground because it's not financially viable to build them at today's market prices.

Of course, this means future new developments will have to sell at prices considerably higher than today’s market value and this will, in turn, pull up the value of established apartments.

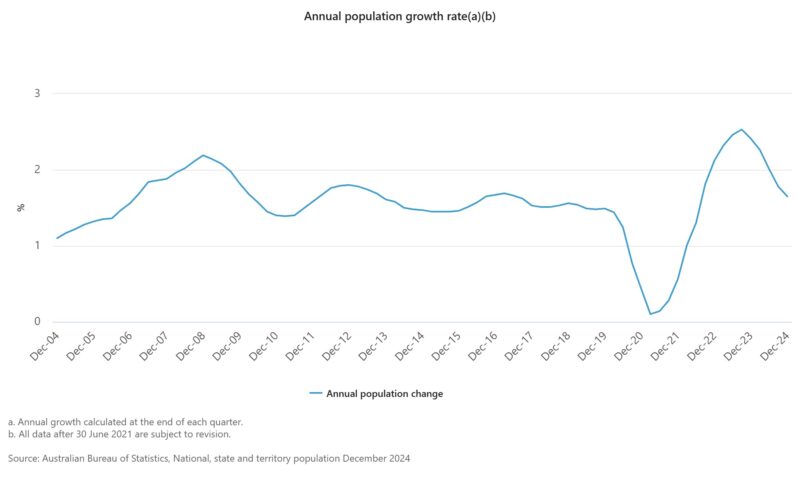

The surge in population growth to a record 660,000 last year, driven by record immigration levels meant that around an extra 250,000 new homes needed to be built last year alone.

But instead, completions have been running around 170,000 as the home building industry struggles to keep up with rising costs and material and labour shortages and as approvals to build new homes fell.

In fact it has been "conservatively" estimated that we have an accumulated housing shortage of around 200,000 dwelling currently, and it is unlikely our housing shortage will be resolved in the next decade, maybe we will have continue continuing pressure for rising house prices and rents.

3. Consumer confidence

Consumer confidence is a critical factor affecting the direction of property prices.

We don't make big financial decisions like moving home or buying an investment property unless we feel confident about our economic future and our financial stability.

Consumer confidence has been at historic lows because of all the economic and socio-political issues that have confronted us, but has picked up recently.

Consumer confidence has been whacked once again with the unprecedented changes in the budget, but this too shall pass, and eventually the “wealth effect” of an improving economy and rising property values will lead to further consumer confidence and bring home buyers and sellers back into the market.

4. Economic climate

Another key factor that affects the value of the property market is the overall health of the economy.

This is generally measured by economic indicators such as the gross domestic product (GDP), employment data, manufacturing activity, the prices of goods, etc.

While the RBA has been trying to slow our economy down to bring inflation under control, currently, everybody who wants a job can get a job and this will underpin our housing markets even if the economy falters a little moving forward.

5. Population growth

In the year ending 30 June 2024, overseas migration contributed a net gain of 446,000 people to Australia's population.

This was a decrease from the record 536,000 people the previous year once the floodgates were opened as we worked our way out of the Covid Pandemic.

While population growth has always been a key driver supporting our property markets, the influx over the last few years has pushed our supply/demand balance off-kilter and is key to the increase in housing prices and the shortage of rental properties.

6. Availability of credit

When the credit (the ability to borrow from the banks) is readily accessible, with lower interest rates and less stringent lending criteria, it tends to stimulate the housing market since more people find themselves able to borrow money to buy homes, leading to increased demand for housing.

On the flip side, when credit is tightened through higher interest rates or stricter lending criteria (as happened when APRA made the banks tighten the purse strings in 2016-7), the effect can be a cooling of the housing market.

Such measures are usually a deliberate policy response to an overheated market, aiming to reduce the risk of a “property bubble” and subsequent crash.

7. Investor Sentiment

This sentiment, essentially the collective attitude and outlook of investors towards property markets, can significantly influence both the demand for and the value of real estate.

Investors generally account for around one-third of all property transactions so positive investor sentiment can drive up property prices, especially in sought-after areas.

Conversely, negative investor sentiment, as occurred during the market downturn of 2022, can lead to a decrease in property values.

If investors believe that property prices will stagnate or fall, they may be less inclined to invest, or they might choose to sell off their properties, increasing supply in the market.

8. Government incentives

Government incentives cut both ways in the property market, and the May 2026 Budget is a clear example of that.

On the demand side, the government's first home buyer schemes continue to add fuel to the lower end of the market.

The ability to buy with a 5% deposit backed by a government guarantee, combined with the Help to Buy scheme allowing eligible buyers to purchase with the federal government contributing up to 30% of the purchase price for existing homes, is bringing thousands of additional buyers into the market.

History is very clear on this - these schemes lift demand and prices, particularly in the affordable segments.

On the investment side, the picture has changed more meaningfully with the Budget.

From 1 July 2027, negative gearing will be limited to new builds, with the stated policy intent being to focus tax support on new housing supply rather than established properties. Rental losses on established residential properties acquired after Budget night will only be able to reduce residential rental income or capital gains, rather than being deducted against salary or other income.

At the same time, the 50% capital gains tax discount will be replaced by cost base indexation and a 30% minimum tax on net capital gains from 1 July 2027, applying to individuals, trusts and partnerships.

The critical protections to understand are these.

Existing property owners, including those already under contract before the Budget night announcement, are grandfathered and can continue to access negative gearing under the current rules. And new builds remain fully exempt, with investors still able to access both negative gearing and the 50% CGT discount.

For investors thinking about their next purchase, the calculations have shifted. A new build bought from here on faces a very different tax environment to an established property, and the decision between the two now involves more than just yield and capital growth projections. Getting sound advice from a qualified tax professional before acting is more important than ever.

Over the long term, I still believe the structural forces driving Australian property values - population growth, housing undersupply, and rising national wealth - will outweigh the impact of these tax changes.

But the investment landscape has become more complex, and that rewards investors who take a strategic, informed approach.

8 economic and property trends to watch out for moving forward

1. The upturn phase of the market will continue throughout 2026

Property price growth will continue throughout 2026, albeit at a lower rate, and our housing markets will be fragmented as affordability will affect many homebuyers.

As mentioned above, it's likely that 2026 will be divided into two halves, with stronger growth in the first half.

2. The Budget has reshaped the investment landscape from 1 July 2027

The tax changes announced in the May 2026 Budget are real and meaningful, but their impact will be felt gradually and unevenly.

What I expect to see is a gradual reweighting of investor activity toward new builds, which remain fully exempt from both the negative gearing changes and the new CGT rules. This has implications for new apartment pricing, developer feasibility, and where future supply gets built.

In the short to medium term, the greater number of established property investors holding for longer - rather than selling and triggering a CGT event under new rules - could actually keep stock levels tight in desirable suburbs.

The market will adapt, as it always does.

3. Interest rates will remain steady for some time

The outlook for interest rates remains uncertain, but they are unlikely to change over the next few months.

4. Our property market will be even more fragmented

Of course, there was really never "one" Sydney property market or one Melbourne property market.

There are markets within markets – there are houses, apartments, townhouses and villa units located in the outer suburbs, middle ring suburbs, inner suburbs and the CBD, and they're all behaving differently.

But our markets will be much more fragmented moving forward as some demographics struggle with cost-of-living, rent and mortgage cost increases (at a time of low wage growth) more than others.

It will either stop them from getting into the property markets or severely restrict their borrowing capacity which will negatively impact the lower end of the property markets.

Meanwhile, many first-home buyers who borrowed to their full capacity will have difficulty keeping up with their mortgage payments at the time of rising interest rates or when their fixed-rate loans convert to variable rates.

In other words, there will be little impetus for capital growth at the lower end of the property market.

That's why I would only invest in areas where the locals’ income is growing faster than the national average - such as gentrifying suburbs - as locals will have higher disposable incomes and be able to and are likely to be prepared to pay a premium to live in these locations.

Many of these locations are the inner and middle-ring suburbs of our capital cities which are gentrifying as these wealthier cohorts move in.

At the same time, I see well-located properties in our capital cities outperforming regional property markets.

5. Migration

Net overseas migration to Australia will remain strong in 2026; however, the Federal government has lowered its forecast for migration in the recent budget.

The influx of immigrants will keep driving rental growth as migrants tend to rent.

Only 38% of migrants own a home after being in Australia for five years, yet 71% of migrants own their home after 10 years.

6. Rents will keep rising

There is no end in sight for our rental crisis, and rent prices will continue skyrocketing into 2026.

In fact, increased rental demand at a time of very low vacancy rates will see rentals continue to rise throughout the next few years.

7. Strategic investors will keep entering the property market

They will compete with first-home buyers who benefit from several government-backed incentive schemes.

As rents continue to rise and the share of first-home buyers continues dropping, strategic investors with a realistic long-term focus will return to the market.

8. Neighbourhood will be more important than ever

In our post Covid world, people will pay a premium for the ability to work, live and play within a 20-minute drive, bike ride or walk from home.

Many inner suburbs of Australia’s capital cities and parts of their middle suburbs already meet the 20-minute neighbourhood tests, but very few outer suburbs do because there is a lower developmental density, less diversity in its community, and less access to public transport.

And ‘neighbourhood’ is important for property investors too, and here’s why.

In short, it’s all to do with capital growth, and we all know capital growth is critical for investment success, or just to create more stored wealth in the value of your home.

This is key because we know that 80% of a property’s performance is dependent on the location and its neighbourhood – in fact, some locations have even outperformed others by 50-100% over the past decade.

And it’s likely that moving forward, thanks to the current environment, people will place an even greater emphasis on neighbourhood and inner and middle-ring suburbs where more affluent occupants and tenants will be living.

These ‘liveable’ neighbourhoods with close amenities are where capital growth will outperform.

What sets these neighbourhoods apart is the demographics – these locations are generally gentrifying or are lifestyle locations and destination locations that aspirational and affluent people want to live in.

So lifestyle and destination suburbs where there is a wide range of amenities within a 20-minute walk or drive are likely to outperform in the future, fetching premium prices in 2024.

9. Our economy and employment will remain robust

Our economy will keep growing (albeit a little slower) and the unemployment rate will remain low thanks to the many new jobs created as our economy grows.

Long-term forecasts for Australian property markets (2025-2030)

Over the next decade, demand for housing is expected to benefit from the triple boost of rising population, rising jobs, and rising income.

Collectively this wealth effect will add around $860 billion of income over the next decade, a significant portion of which is likely could be directed towards housing.

The average Australian tend to spend 13% to 20% of their income and either rent or mortgage servicing.

Of course, no matter how many times you forecast property prices, it will always be difficult to predict exactly where property markets and prices will be in three months' time, let alone 6-7 years into the future.

After all, history shows us that some properties will outperform others by 50-100% in terms of capital growth, so strategic property investors who buy investment-grade properties could expect to see the value of their properties more than double within the next seven to 10 years.

So we always have to take forecasts for Australian property markets with a big pinch of salt.

But what I am confident we’ll see for our future property markets comes off the back of our strong projected population increase.

- Also read:Melbourne property market forecast for 2026 & 2027 | Why the opportunity is bigger than it looks

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – May 2026

Currently, there are about 27.6 million Australians and Australia's population is forecast to rise to over 30 million people by 2030.

This means close to 3 million more people will need somewhere to live and this will underpin our property markets.

What we predict for Australia’s property market is that there will be many more high-rise towers of apartments, not just in the CBD but in our middle-ring suburbs.

In fact, we are already starting to see this, particularly in Melbourne and Sydney.

And we also expect there will be lots more medium-density housing – in particular townhouses will be a popular way to live with modern large accommodation on more compact blocks of land.

So what about property prices for 2025-2030?

Some economists predict a 40-50% growth in Australia's house prices between now and 2030.

This isn’t surprising because it’s often said that over the long term, the average annual growth rate for well-located capital city properties is about 7% (and we know that prices have risen 6.8% per annum over the past 30 years), which would mean, in general, well-located properties should double in value every 7-10 years.

That would put Australia’s median dwelling price at around $1.1 million in 2030.

Final Thoughts: So, Where to From Here?

I believe we’re in a window of opportunity for property investors who take a long-term view.

While in the short term, flat buyer and seller sentiment will dampen our housing markets as always, this too shall pass, and we will enter a period that some would call a “perfect storm” of fundamentals that are aligning to support strong property markets in the years ahead:

- Continued rapid population growth is putting pressure on housing.

- An acute undersupply of dwellings,

- A chronic shortage of skilled labour, making new development slower and more expensive.

- Inflation has moderated, now sitting within the RBA’s target range.

- Interest rates will fall again but probably not until next year – bringing more buyers into the market.

- Government first homebuyer incentives will keep pouring fuel on the flames of our undersupplied housing market.

To be clear, I’m not suggesting anyone try to "time the market"—that’s near impossible to get right consistently.

However, many successful investors built significant wealth by buying during the early stages of an upturn, when fear still lingered and competition was low.

Looking ahead, demand will continue exceeding supply for the foreseeable future. Strong immigration, restrictive planning regulations, and the slow delivery of new housing stock will keep upward pressure on prices.

Meanwhile, the cost to deliver new dwellings is rising and will continue to rise.

It’s not just supply chain issues or labour shortages—it’s also financial viability. Developers won’t launch projects unless the numbers stack up, and right now, that means new stock will need to enter the market at significantly higher prices than existing homes.

So if you’re in a financially stable position and thinking of buying your next home or investment property—this may be your moment.

Because in property, like in life, you don’t get rewarded for waiting. You get rewarded for acting with clarity while others are uncertain.

Fact is, the smart money is already on the move.

But what about you? Are you clear on how to take advantage of these market conditions — or are you still waiting for "certainty"?

Tip: Need some clarity? Why not start with a complimentary Wealth Discovery Consultation with one of our Property Strategists? Leave us your details here.

That’s where our Complimentary Wealth Discovery Session comes in. We’re offering you a 1-on-1 chat with a Metropole Wealth Strategist to help you:

- Clarify your financial goals

- Understand how macro trends affect your position

- Build a personalised, data-driven property strategy

- Get ahead of the curve — before everyone else piles in

There’s no cost, no obligation — just practical, tailored guidance based on decades of experience.

Click here now to book your free Wealth Discovery Session

NoBookmark this page and check back regularly — we update this forecast often to reflect the latest insights and trends.

The property market never stands still, and neither should you.