Key takeaways

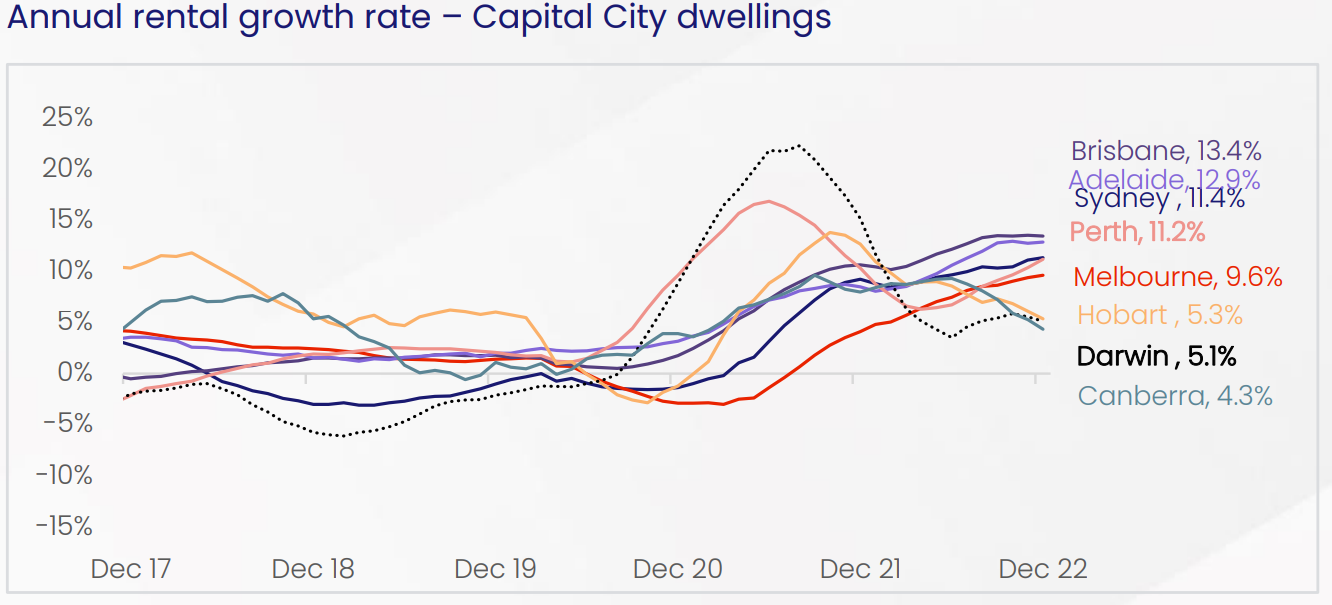

Rents nationally increased 10.2% in 2022, a record high for annual rent growth.

New rental listings hit 10-month high and vacancy rates ease, albeit slightly.

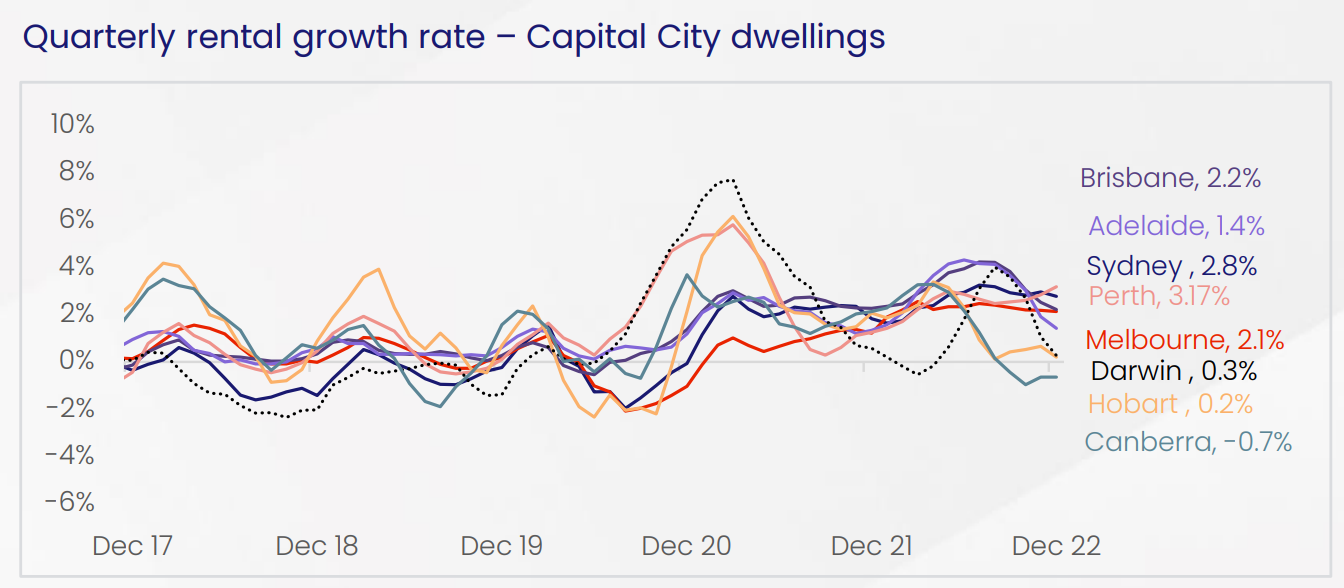

Canberra was the only capital city where dwelling rents declined in Quarter 4.

As Australia’s rental market continues to tighten to record levels, the pace of rental growth has slowed for the second consecutive month, possibly due to a seasonal lift in rental stock combined with affordability constraints.

CoreLogic’s Quarterly Rental Review for Q4 2022 shows the Australian dwelling market saw a slowdown in the pace of rent value growth to 2.0% in the December quarter.

This was down from 2.3% growth in the September quarter, and a peak quarterly growth rate of 3.0% in the three months to May.

December marked the second consecutive quarter that the pace of growth slowed, and coincided with a small lift in the rental vacancy rate to 1.17% in December (up from a recent low of 1.05% in the previous month).

The decline in quarterly rental growth rates observed in the December quarter was led by the capital cities where rents continued to increase but at a slightly slower rate than they have done in September and June quarters.

While a slowdown in the pace of rent rises could be a sign that the rental market is starting to shift, it’s not great news for tenants just yet.

Rents are still rising in most capital cities and regional areas with vacancy rates low.

Since the start of the upswing in September 2020, Australian rent values have lifted 22.2%, marking the largest rental upswing on record (based on the CoreLogic hedonic rental index back series, which goes back almost 18 years).

During this 27-month period, the median weekly rent valuation across Australian dwellings rose from $430 per week to $519.

Supply-side reaches a seasonal peak

The small lift in the rental vacancy rate to 1.17% in December, up from a low of 1.05% in November and a slowing rate of growth could be due to several factors.

It is not entirely clear whether the rental market will continue inching toward a turning point, or if this is a temporary, seasonal reprieve due to higher new listings through December.

Newly advertised rent listings saw a seasonal peak in the four weeks to December 11th.

Through this period, 50,867 new advertised rental listings were counted by CoreLogic, which is the highest volume observed since mid-February, another seasonal high point.

However, it’s important to recognise despite the increase in rental listings, the figures remain - 13.8% lower than the previous five-year average for this time of year.

With another seasonal uplift in advertised rents expected in the next few weeks, rental growth could ease further.

Capital cities vs regional rents

Quarterly growth in the combined regional rent market was 1.3%, unchanged from the previous quarter, though there were some mixed outcomes in rental performance below this headline figure.

The quarterly pace of rent value growth lifted in most regional markets, though it declined across regional NT, regional SA and regional Qld.

Rent value growth jumped notably across regional Tasmanian dwellings in the December quarter, to 3.0%.

This was up from 0.3% in the September quarter.

While this relatively small market may show more volatility in growth rates, Tasmania has also seen a strong surge in net overseas migration post-pandemic travel restrictions, which may be pushing rental demand higher.

The state saw an additional 2,745 people arrive from overseas in the year to June 2022, higher than the pre-COVID five-year average of 2,325.

Capital best and worst performers

Canberra saw a -0.7% decline in dwelling rents over the quarter, comprised of a -0.8% fall in house rents and a -0.2% decline in unit rents.

Canberra rent values have fallen a cumulative -1.1% since peaking in June, following a trough-to-peak upswing of 18.1% from September 2020.

Darwin house rents declined by -0.3% in the December quarter.

- Also read:National Weekly Auction Report – August 1st 2026 | Mixed Auction Results to Begin August – Sydney Down, Melbourne Up

- Also read:July Home Prices Sharply Down as Winter Freeze Bites | Latest Property Market Stats

- Also read:Australia’s jobs boom raises the risk of another interest rate rise | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

The overall dwelling market has seen a rapid deceleration in rental value growth, with the quarterly increase sitting at just 0.3%, down from 3.6% in the June quarter.

Rental value increases saw a notable slowdown in Adelaide, where dwelling rent appreciation was 1.4% in the December quarter, down 220 basis points from the previous quarter.

Brisbane also saw a notable drop in the rate of quarterly dwelling growth, at 160 basis points.

Quarterly growth in Sydney and Melbourne dwelling rents declined a milder 20 basis points, while Perth was the only capital city rental market to see an increase in the rate of quarterly growth.

Canberra maintained its position as Australia’s most expensive capital city rental market by just $2, with a median weekly rental value of $681, followed by Sydney ($679 per week) and Darwin ($594 per week).

Melbourne remains Australia’s most affordable capital city for rentals at $507 per week, followed by Adelaide ($518 per week), Hobart ($552 per week) Perth ($553 per week) and Brisbane ($588 per week).

Population dynamics may be creating some variation in performance across capital city rental markets with ABS population data showing a weakening internal migration trend across Canberra and a fairly strong return in net overseas migration for Sydney and Melbourne.

Unlike Canberra, high levels of net overseas migration to NSW and Victoria have vastly offset negative net internal migration flows in the year to June 2022.

Prior to the pandemic, Sydney and Melbourne alone accounted for around two-thirds of net overseas arrivals, with high-density city centres being among the most popular destinations.

This has likely contributed to unprecedented annual growth in unit rents over 2022, which was 15.5% across Sydney and 14.2% in Melbourne.

Gap between house and unit rent narrows

The growth in Australia’s unit rents remained high at 2.8% in the December quarter, while house rents rose 1.7% for the same period.

The unit market has seen higher rates of quarterly growth than houses since February 2022, however, growth across both housing types remains high relative to historic averages.

This trend broadly coincides with the repeal of overseas travel restrictions to Australia, suggesting the return of overseas migration could be diverting additional demand to the high-density housing market.

Yields continue to improve

The growth of rent values has outpaced purchase values on a monthly basis since February 2022 leading to an improvement in national gross rent yields of 57 basis points during this time period.

Nationally, gross rent yields across all dwellings increased to 3.78% in the December quarter, which still falls well below the pre-COVID decade average of 4.24%.

Rental market unclear for 2023

The rental market outlook is mixed for 2023, with an increase in demand from international visitors during a time of weak confidence among property investors.

On the one hand, returning overseas migration is likely to place continued demand on rental markets popular with overseas arrivals.

Historic migration data suggests this would be Inner Melbourne, the South East of Melbourne, the West suburbs of Melbourne and Sydney's Inner South West.

On the flip side investor activity, and therefore rental supply is not expected to pick up substantially in the year ahead.

Even though rent yields are rising, investors are facing higher interest costs and reduced capital growth prospects.

A seasonal uplift in newly advertised listings is expected in the first quarter of 2023, which is likely to provide more choice for renters and demand-driven shifts such as more share housing, and internal migration to more affordable markets may also help to ease rental conditions.