Key takeaways

Despite media noise about easing rental conditions, the data clearly shows a persistent and severe rental shortage.

While there’s been a lot of noise lately about rental growth slowing and affordability improving, the data paints a very different, and much more persistent picture.

Despite slight upticks in rental vacancy rates in recent months, Australia remains firmly in a landlord’s market.

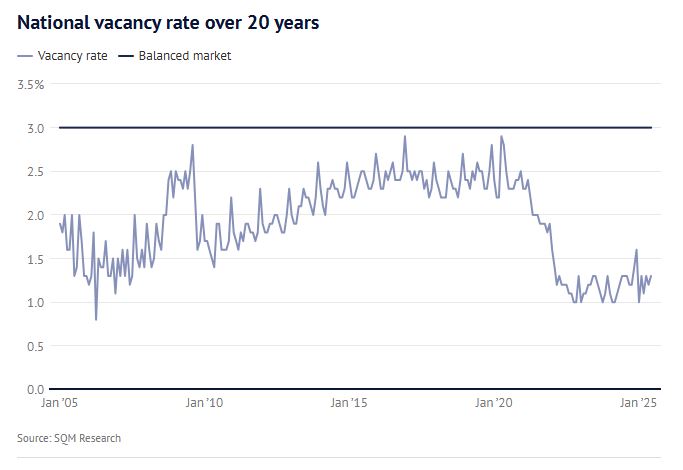

Vacancy rates remain well below the balanced market benchmark of 3%. As of June, the national vacancy rate was just 1.3%.

While there’s been a lot of noise lately about rental growth slowing and affordability improving, the data paints a very different, and much more persistent picture.

Despite slight upticks in rental vacancy rates in recent months, Australia remains firmly in a landlord’s market.

And this isn’t a short-term blip, it’s a structural trend that’s been playing out for the better part of two decades.

The rental market: out of balance for years

A healthy, balanced rental market typically sees a vacancy rate of around 3%.

That’s the level where supply and demand are roughly aligned, enough properties for renters to have choice, without flooding the market and pushing landlords to drop rents.

But the reality is, we haven’t seen those conditions in quite some time.

According to SQM Research, the national vacancy rate sat at just 1.3% in June—up slightly from 1.2% in May, but still dramatically below the long-term average.

Source: The Age

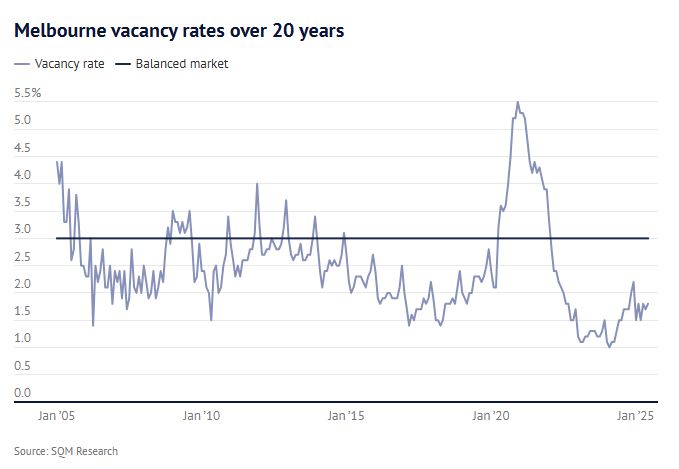

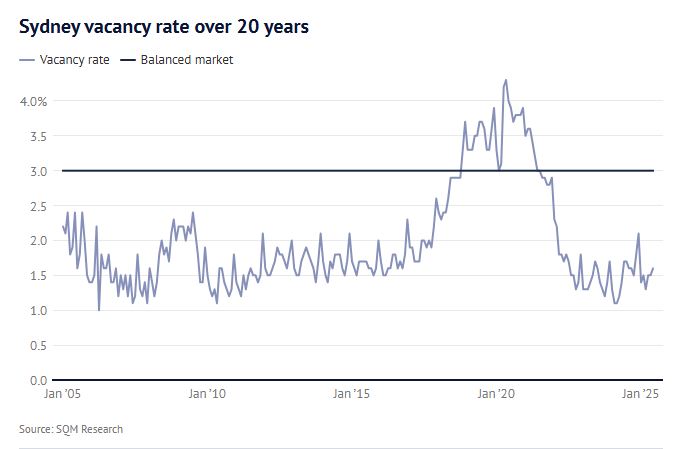

Sydney and Melbourne both experienced minor increases, but remain deeply undersupplied, with vacancy rates of 1.6% and 1.8% respectively.

In fact, the tightest market on record came just earlier this year, in February 2024, when vacancy rates hit 1% nationwide and just over 5,000 properties were available for rent across the country.

That’s a dire level of supply.

Why it's still a landlord’s market

There are two sides to the rental equation: demand and supply.

Unfortunately, both are pulling in the same direction—and neither is offering much relief for renters.

On the demand side, we’ve had a tidal wave of returning migration. International students, skilled migrants, and Australians returning from regional moves or overseas relocations have flooded back into our capital cities.

But unlike earlier cycles, we weren’t prepared this time around.

Population growth has outpaced our ability to deliver new housing stock, especially rentals.

On the supply side, construction has failed to keep up.

Rising building costs, labour shortages, planning bottlenecks, and diminishing developer confidence have all contributed to a shortfall in new dwelling completions.

And let’s not forget the mounting pressure on mum-and-dad investors: land tax increases, tenancy reform, higher mortgage costs, and regulatory risk have forced many to sell up.

The result? Fewer properties to rent and skyrocketing rents in many locations.

How does this compare to the past?

It’s worth looking at history for context.

In June 2005, Melbourne’s rental vacancy rate was 3.9%—a renter’s market.

Source: The Age

Sydney was at 2.4%. We were building strongly then.

Source: The Age

Major urban renewal projects like Docklands and Southbank were coming online, and population growth was more subdued.

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – April 2026

- Also read:National Weekly Auction Report – April 11th 2026 | Auction Markets Steady After Easter with School Holiday Listings

- Also read:Latest Property Asking Prices State by State | National Listings Rise in March

- Also read:Rents Surge Again as Interest Rates Bite – What Happens Next?| | Property Insiders

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

Fast forward to today, and not only are vacancy rates significantly tighter, but our housing pipeline has slowed to a trickle in many areas.

The same cities now have vacancy rates under 2%, with no sign of a quick fix.

Are Government targets enough?

Yes, there are housing targets.

The federal government wants to see 1.2 million homes built in five years.

Victoria has set its own goal of 800,000 over a decade.

And NSW is aggressively rezoning land to boost density around transport hubs.

But here’s the catch: these targets are aspirational.

They require coordination, private sector investment, faster approvals, and an easing of cost pressures across the board.

That’s a tall order.

Even if Victoria meets its national housing goal, that won’t be enough to instantly unwind years of undersupply.

The pipeline is long, and the bottlenecks are structural.

What it means for property investors

If you’re a landlord, this is likely music to your ears. A tight rental market with strong tenant demand means:

-

Rising rents (or at least sustained high levels)

-

Lower vacancy risk

-

Improved rental yields

-

More control over tenancy terms

But it’s not all smooth sailing.

Many investors are also dealing with rising interest rates, higher holding costs, and more aggressive land tax bills, particularly in states like Victoria.

And with the push toward greater tenant protections, you need to be strategic and selective in your property purchases and management practices.

For the astute investor, these conditions create an opportunity, not just to ride the current wave, but to plan for the next decade.

Owning the right type of property in the right location, where demand will remain high and supply constrained, will be the key to long-term success.

The bigger picture: housing as infrastructure

What’s becoming increasingly clear is that housing isn’t just a social issue, it’s economic infrastructure.

Without enough homes, people can’t relocate for jobs. Students can’t afford to study.

Families are forced into unsuitable living arrangements.

We’re already seeing households double up: two couples sharing a two-bedroom apartment just to afford the rent.

This squeeze isn’t going away anytime soon. And unless we radically boost the supply of quality, affordable rental housing, Australia will remain a landlord’s market for the foreseeable future.