Key takeaways

RBA reverses course to regain control over inflation, but a single hike is unlikely to alter the housing market balance.

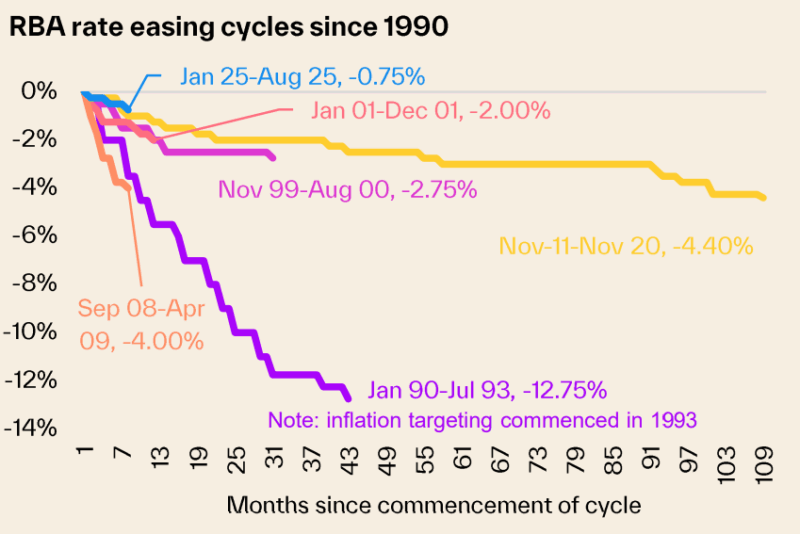

This marks the end of the shortest and most modest rate cutting cycle since the RBA started inflation targeting in 1993.

The outlook for the cash rate remains somewhat clouded.

Given the underlying supply and demand pressures in the Australian housing sector, it is unlikely that a single rate hike will substantially alter the market balance.

RBA reverses course to regain control over inflation, but a single hike is unlikely to alter the housing market balance.

At its first meeting for 2026, the Reserve Bank of Australia (RBA) lifted the cash rate to 3.85% (from 3.6% previously).

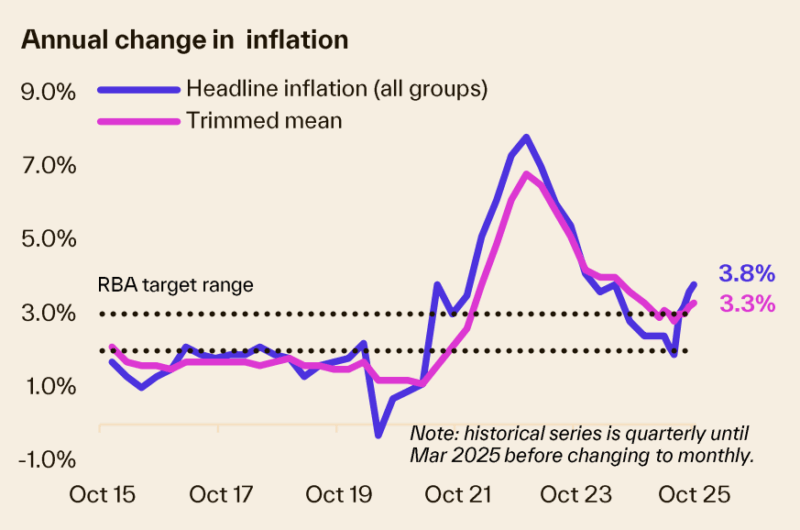

This decision came in the wake of a surprise tightening in the labour market (unemployment dropped to 4.1% in December) and inflation drifting away from the RBA’s target range (the trimmed mean measure increased by 3.3% yoy in December).

This marks the end of the shortest and most modest rate cutting cycle since the RBA started inflation targeting in 1993.

The RBA has been data driven, and the recent inflation and unemployment data are inconsistent with its dual mandate of price stability and full employment, meaning today’s decision to lift the cash rate was widely expected.

Housing was one of the largest contributors to annual headline inflation , increasing by 5.5% yoy in December.

Much of this increase reflects the sharp rise in energy costs (as electricity subsidies expired), however, higher rental prices and the costs of building a new home are also adding to the cost of living pressures.

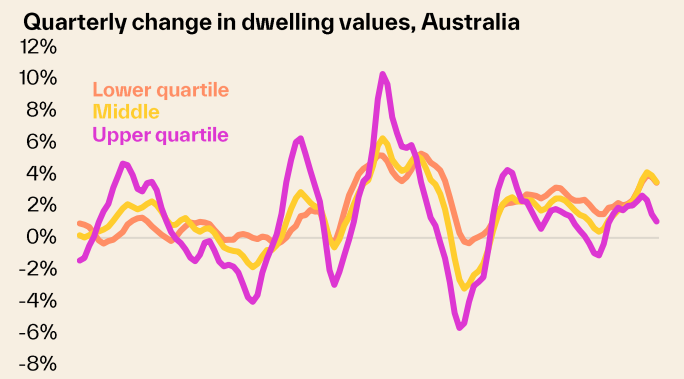

From an established housing perspective, Cotality’s Home Value Index has increased by 9.0% across Australia since the RBA’s rate cutting cycle commenced in February 2025, adding around $75k to the median dwelling value nationally.

Lower lending rates and increased borrowing capacity were key factors contributing to growth, fueling housing demand that has consistently outstripped supply for some time.

Home values rose by 0.8% month - on -month in January, with stronger growth evident in more affordable, lower quartile properties.

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – April 2026

- Also read:National Weekly Auction Report – April 11th 2026 | Auction Markets Steady After Easter with School Holiday Listings

- Also read:Latest Property Asking Prices State by State | National Listings Rise in March

- Also read:Rents Surge Again as Interest Rates Bite – What Happens Next?| | Property Insiders

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

This rate hike is likely to reduce some of the demand side pressure

The average new mortgage is close to $700k, and a full pass through of rates will add around $110 per month to repayments (assuming typical market interest rates on a 30-year mortgage).

Similarly, the hike will reduce the borrowing capacity of buyers, with a median income household in Australia losing around $18k from their mortgage limit.

This could push an increasing number of buyers from mid-tier properties to lower quartile ones, leading to higher demand on the urban fringes and regional markets close to capital cities.

That said, Australian housing markets will be impacted by a range of headwinds and tailwinds in 2026.

Affordability and serviceability pressures, only exacerbated by the rate hike, and slower population growth should temper demand to a degree, however first home buyer benefits have been extended and housing supply is likely to remain constrained.

Construction and labour costs, along with labour availability, is limiting the new supply of housing across the country, with interest rates unable to influence this trend.

Similarly, dwelling listings remain well below trend, with uncertainty unlikely to draw potential sellers from the sidelines.

The outlook for the cash rate remains somewhat clouded

Pricing in the interbank cash futures market in late January implied at least two rate increases across 2026.

Among market economists, three of the big 4 banks currently see this hike as a “one and done” move, with the RBA remaining on hold for the remainder of the year, while NAB see a second increase mid-year.

Given the underlying supply and demand pressures in the Australian housing sector, it is unlikely that a single rate hike will substantially alter the market balance.