Key takeaways

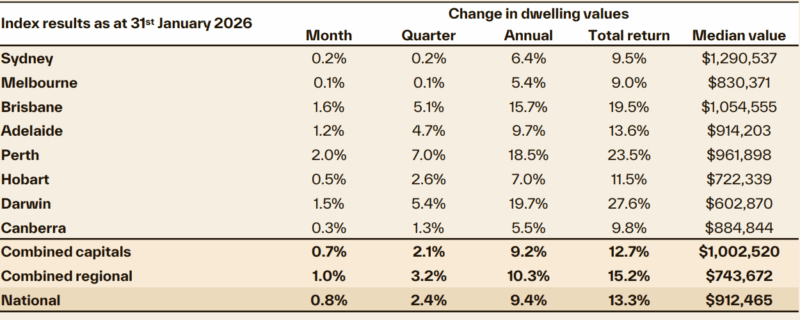

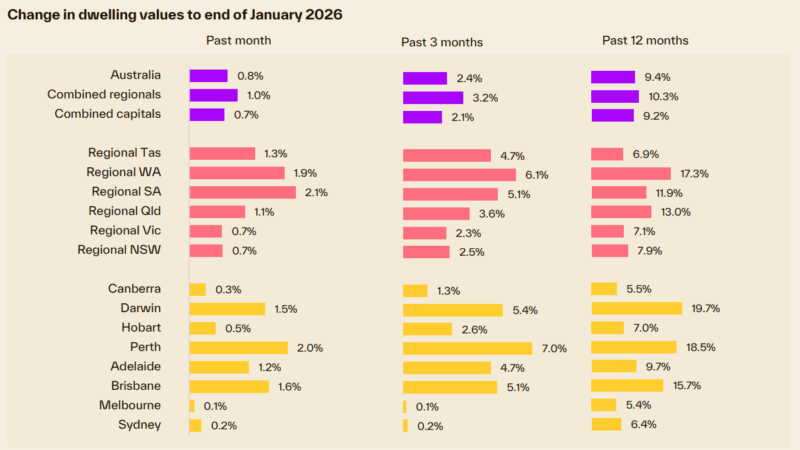

Australian home values rose by 0.8% in January according to Cotality’s Home Value Index, a subtle acceleration from the 0.6% increase recorded in December.

Sydney and Melbourne are weighing on the headline numbers, recording a 0.2% and 0.1% increase respectively in January; a marginal pickup following the slight falls recorded in December.

The mid-sized capitals have continued their solid growth run, however some momentum has left the upswing in these cities as well.

Demand-side headwinds are becoming more evident as acute affordability constraints, normalising population growth, and a cautious credit environment combine with fragile consumer sentiment and the potential for rate hikes.

Tailwinds likely to support prices despite softer demand include persistently low supply levels, attractive incentives for first-home buyers, ultra-tight rental markets nudging renters toward ownership, and labour market resilience alongside steady economic growth.

Australian home values rose by 0.8% in January according to Cotality’s Home Value Index, a subtle acceleration from the 0.6% increase recorded in December.

While every capital city and broad rest of state region recorded an increase in home values through the month, the start of the year returned a mixed result.

Sydney and Melbourne are weighing on the headline numbers, recording a 0.2% and 0.1% increase respectively in January; a marginal pickup following the slight falls recorded in December.

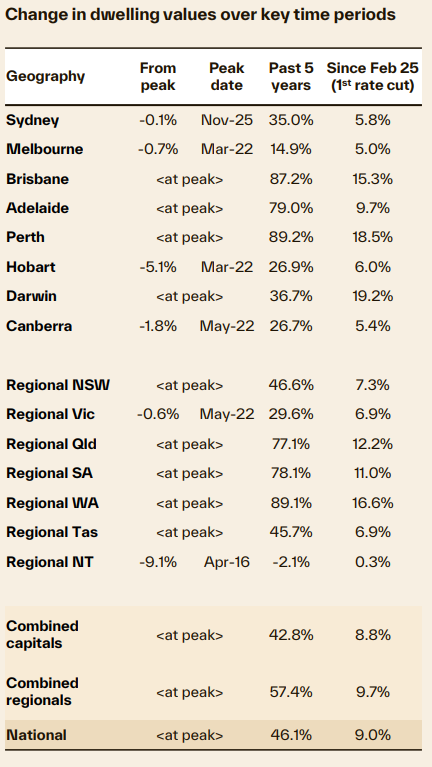

Both markets have values slightly down on their peak levels, with Sydney -0.1% below the November 2025 peak and Melbourne values remaining 0.7% lower than record highs recorded in March 2022.

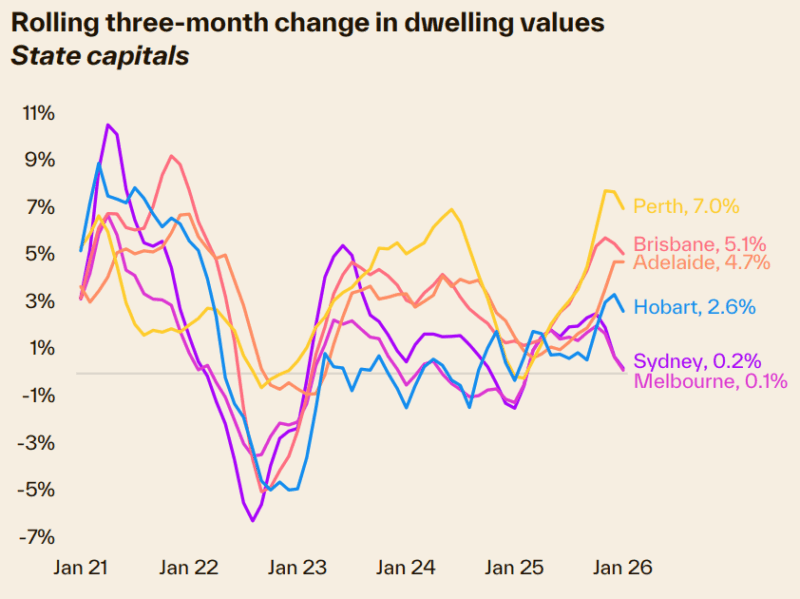

The mid-sized capitals have continued their solid growth run, however some momentum has left the upswing in these cities as well.

Perth values were 2.0% higher in January, the strongest gain across the capitals, but well below the cyclical high of 2.9% MoM growth recorded in November last year.

Similarly, Brisbane’s monthly gain has slowed from 2.0% in October last year to 1.6% in January, and Adelaide’s monthly increase dropped back to 1.2% from a 1.8% rise in December.

The market’s resilience, but suggests further momentum is likely to leave the market.

Despite the most unaffordable conditions on record in many cities, along with a rebound in cost of living pressures and prospect of a rate hike as early as this Tuesday, we are still seeing a broad-based rise in housing values.

The ongoing capital gains reflect persistently low inventory in the face of above average housing demand, however we are likely to see demand side pressures gradually ease in 2026.

Affordability and serviceability constraints are likely to naturally dampen demand, but also renewed cost of living pressures and a strong chance that interest rates will rise.

There is also slowing population growth to consider.

Cotality estimates the number of homes advertised for sale was 19% below levels at the same time last year, and 25% below the five-year average for this time of year.

At the same time, the rolling quarterly number of home sales was estimated to be 1% higher than a year ago and only 3% below the five-year average.

Most cities are continuing to see homes at the lower end of the value spectrum supporting growth

This is especially observed for houses.

Across the combined capitals, lower quartile house values were up 1.3% in January compared with a 0.3% rise across the upper quartile.

This trend of stronger growth conditions at lower price points is supported by intense competition for more affordable houses.

This is where first home buyers, investors and, progressively, mainstream demand is most concentrated.

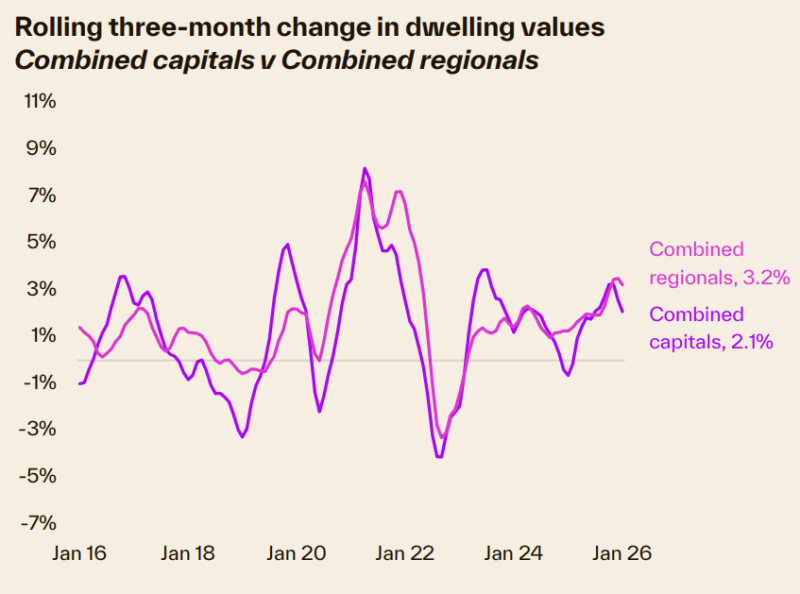

Regional markets have delivered a stronger growth outcome, with the combined regionals index up 1.0% in January compared with a 0.7% rise across the combined capitals.

Outlook

Australia’s housing market is set to navigate an increasingly complex mix of headwinds and tailwinds over the coming year.

While supply side constraints and a resilient labour market continue to support values, housing demand is likely to be tempered by a range of headwinds.

On balance, its likely housing conditions will remain diverse around the country but lose some momentum.

That said, a material downturn seems unlikely unless economic conditions weaken more than expected or more rigorous credit controls arise.

Demand side headwinds are becoming more evident

1. Higher inflation and the potential for further rate hikes.

With inflation above the RBA’s target range, and ticking higher in December, the chance of at least one rate hike is high.

Even without a lift in the cash rate, the expectation of higher rates is likely to erode confidence, while any actual increase will flow through quickly to borrowing costs and less purchasing power.

- Also read:Rents Surge Again as Interest Rates Bite – What Happens Next?| | Property Insiders

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

- Also read:National Weekly Auction Report – March 28th 2026 | Auction Clearance Rates Still Fading Over Super Week of Listings

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

2. Affordability and serviceability constraints remain acute.

Home values have risen significantly relative to incomes, and interest rates are a full percentage point above the pre-COVID decade average.

As a result, both the deposit hurdle and ongoing serviceability assessments continue to present substantial barriers for prospective buyers.

3. Normalising population growth.

After several years of exceptionally strong net overseas migration, the ‘catch up’ phase of population growth has moderated back toward longer-run averages.

While still positive for underlying housing demand, the step-down removes some of the extreme pressure on housing demand.

4. A more cautious credit environment

Credit conditions are tightening at the margin. APRA’s introduction of limits on high debt-to-income (DTI) lending from February 1 set the tone for a more cautious lending environment in 2026 but aren’t likely to have an influence on the headline trends.

With investor credit growth tracking close to record highs, speculative activity could be another area of focus if credit growth across this segment doesn’t moderate.

Additionally, the three-percentage point serviceability buffer remains a formidable barrier for borrowers, especially if rates move higher.

5. Consumer sentiment remains fragile

Household confidence has been subdued for an extended period, with a renewed downtrend in December and January reflecting cost-of-living pressures and uncertainty around the economic outlook.

Weaker sentiment typically correlates with softer housing demand as buyers defer major financial commitments.

Tailwinds likely to support prices despite softer demand

1. Persistently low supply levels

Both advertised stock and new housing completions are expected to remain well below average.

Construction costs are elevated and rising, making it hard for residential projects to stack up from a feasibility perspective.

Established supply is also constrained, with listings in January almost 25% below the five-year average for this time of the year.

Even if listings rise, particularly if selling times extend, supply is still likely to sit below underlying demand.

2. Attractive incentives for first-home buyers.

State and federal schemes remain supportive for eligible buyers, helping offset some of the affordability challenges and channeling demand into the lower quartile of the market.

These incentives, along with broader affordability and serviceability constraints, tend to amplify demand around mid-range to entry-level segments, even when broader demand is softening.

3. Ultra-tight rental markets nudging renters toward ownership.

Vacancy rates remain historically low, and rental growth has outpaced wage growth for several years.

For some households, the additional cost of paying down a mortgage relative to paying a landlord is likely to be increasingly attractive, especially if they can take advantage of government schemes aimed at supporting first time buyers.

4. Labour market resilience and steady economic growth

Unemployment is expected to remain low by long-run standards, and the economy is forecast to grow around 1.9% in 2026.

While not strong, this level of economic activity is generally supportive of housing, providing a buffer against distressed selling and broader market weakness.

5. Overall, the year ahead is shaping up to be one of softer, more uneven growth

Demand is likely to be dampened by affordability and credit headwinds, while supply constraints and a still-resilient labour market will act as important stabilisers.

In this environment, a slowdown in value growth, rather than a sharp reversal, appears the more probable path, unless economic or credit conditions deteriorate more than expected