Key takeaways

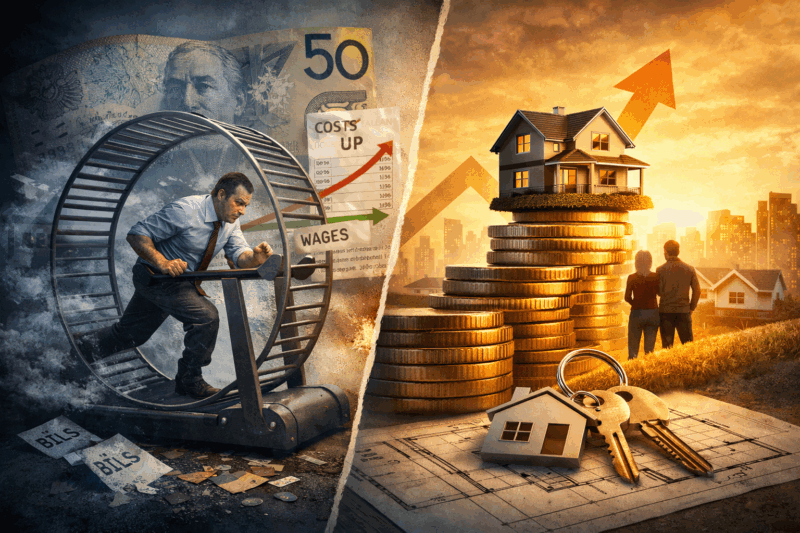

Australians are realising that despite working harder, getting educated, saving diligently, and paying off debt, they’re still falling behind financially.

That’s not due to personal failure, but because the traditional formula no longer works in a system where fiat money has eroded purchasing power over decades.

When the gold standard was abandoned in 1971, money was no longer tied to anything tangible. This ushered in an era where governments could create money freely, devaluing savings and income.

Rising prices are just a surface-level symptom of inflation. The deeper effect is the steady erosion of what your money can buy. While your salary might increase on paper, real-world purchasing power often decreases, meaning your savings are silently being diluted over time.

Property remains one of the most reliable inflation hedges. Unlike money, land can't be printed. That’s why residential real estate in Australia has outpaced both wages and inflation over the long term.

Strategic investors understand how to leverage property for capital growth, income, and tax benefits—all while protecting against inflation.

In today’s economy, income covers expenses—but assets build wealth. The middle class squeeze isn’t accidental; it’s systemic.

Those who focus on ownership, not just effort, will pull ahead. To succeed, Australians must stop playing by outdated rules and start building a portfolio of appreciating, income-producing assets like well-located residential property.

Here’s the uncomfortable truth many Australians are starting to realise - you can work harder than ever, do everything “right”, yet still fall behind financially.

It’s not due to buying too many lattes or smashed avocado sandwiches, and it’s certainly not due to a lack of ambition.

It’s because the rules of money quietly changed a few decades ago, meaning that today hard work keeps you busy, but it doesn’t automatically make you financially free.

The treadmill problem

I’ve noticed a growing frustration echoing across Australia.

People are doing exactly what they were told would lead to security: get a good education, work long hours, save diligently, and pay down debt. Yet somehow, they’re still running just to stand still.

Wages haven’t moved much in real terms for years, but housing costs, groceries, insurance, education, and energy bills just keep climbing.

Young couples have difficulty saving a deposit for properties that feel perpetually out of reach.

Families with solid incomes wonder why life feels tighter than it did for their parents.

And it’s not because Australians became irresponsible. It’s because the financial system quietly shifted beneath our feet.

The game changed a few decades ago

You see…back in 1971, the world rewrote the rules of money.

The US removed the gold backing from its currency, and with that decision, money stopped being tied to anything tangible.

Other countries, including Australia, had little choice but to follow. We entered the era of what is called “fiat money”, where the currency is backed by government decree rather than a physical asset like gold.

While that shift sounded technical and harmless at the time, it had long term consequences that still define wealth today.

Once money could be created freely, every new dollar diluted the value of existing dollars.

Over time, savings lost purchasing power. Wages struggled to keep up. Meanwhile, real assets began pulling away from incomes.

This is how the gap between those who earn money and those who own assets really began.

Inflation isn’t just rising prices; it’s theft by dilution

We often talk about inflation as “prices going up”, but that’s only half the story.

The deeper issue is currency debasement.

When governments create more money, each dollar becomes slightly weaker. Your bank balance doesn’t shrink in numbers , but it shrinks in what it can buy.

Think of it like owning a slice of a pizza. If more slices keep getting added without the pizza getting bigger, your share is worth less. That’s what’s happened to money over the last 50 years.

Wages rise on paper, but purchasing power quietly erodes.

Savings accounts may look safe, but in real terms they’re often going backwards.

And that’s why so many Australians feel like they’re doing everything right yet still losing ground financially.

Why hard work alone no longer works

You’ve probably noticed how, over the years, wages have largely flattened after tax and inflation.

You can see it in everyday life. Pay rises disappear into higher rents, mortgage repayments jump, and childcare and insurance costs surge.

Even with dual incomes, many households feel squeezed.

The old formula - work hard, save steadily, retire comfortably - worked when money held its value and asset prices moved slowly. It doesn’t work in a world where money is printed faster than wages rise.

[note] Today, income pays the bills, but assets shape your future. [/notes]

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

That’s the disconnect many people haven’t fully grasped yet.

Property: the inflation hedge most Australians overlook

Here’s the key difference between money and property: money can be printed, land cannot.

That fact explains why residential property has been such a powerful wealth builder over the last half-century.

As more money enters the system, the value of tangible, scarce assets rise in comparison.

Australian property has comfortably outpaced inflation and wages over the long term and that’s because it sits on the right side of monetary reality.

When inflation rises, rents tend to rise. When money is diluted, replacement costs increase. When population grows and land remains finite, well-located property becomes more valuable.

Sure, the property market cycles, but the long-term trend for well-located residential property has been up and will continue to be so.

Why investors keep “winning” (and it’s not luck)

People often look at property investors and assume they were lucky, well-timed, or privileged.

In reality, most simply understood the rules of money.

These strategic investors know that cash sitting in the bank is guaranteed to lose value over time, while using leverage (other people’s money sitting in the bank) to control an appreciating asset quietly compounds your asset base.

A well chosen investment property does four things at once:

- It grows in value over time; over the last 40 years, capital city residential real estate has appreciated by an average of 6.8% per annum.

- It allows you to leverage long-term growth with borrowed money, which significantly magnifies the return on your funds.

- It produces income (rent) that tends to rise with inflation.

- And you can take advantage of legal tax incentives like negative gearing and depreciation benefits.

Sure, property values don’t rise consistently and occasionally falter. And yes, things not only can go wrong; they will go wrong, but this combination of advantages of property means it is a financial shield against inflation and the slow erosion of purchasing power.

The middle class squeeze isn’t accidental

Fact is, the system is stacked in favour of those who own appreciating assets.

Young people are living with their parents longer. Couples are delaying having kids, and working longer into “retirement years” isn’t an ambition; it’s become a necessity for many.

The “system” increasingly rewards ownership over effort.

Those who own appreciating assets pull further ahead, while those relying purely on income fall behind, no matter how hard they work.

This isn’t about greed, it’s about understanding the environment you’re operating in.

Stop playing by outdated rules

Maybe your parents could trade effort for security. Many bought a home on one income, raised a family, and paid off the mortgage within 20 years.

That world no longer exists. Today, working harder doesn’t guarantee progress. Thinking smarter does.

That means shifting your mindset from “how do I earn more?” to “how do I own more of what grows faster than inflation?”

This is why thinking like an investor matters. Investors play a different game.

They plan for the long term, focus on fundamentals and use assets to do the heavy lifting rather than their labour.

Final thought: don’t hate the game, learn the game

The financial system didn’t become unfair overnight, and it’s not going back to what it was.

Money will continue to be created. Inflation will continue to erode savings. And real assets will continue to protect those who own them.

There is no benefit in resenting that reality, if you want to get ahead you need to adapt to it.

Hard work still matters, but it’s no longer enough on its own. In a world of fiat money, ownership is the real path to financial freedom.

Your future won’t be determined by your salary or job title. It will be shaped by whether you build assets that grow while you sleep.

The earlier you start playing the right game, the better the outcome.