Key takeaways

While there are frustrations, particularly among younger Australians, who liken the housing market to a Ponzi scheme, this analogy oversimplifies complex market dynamics.

A Ponzi scheme is a fraudulent investment setup that relies on continuous new investor money to sustain itself.

The Australian housing market is supported by several solid fundamentals that differentiate it from a Ponzi scheme:

*High Owner-Occupancy Rate: Nearly 70% of Australian homes are owner-occupied, which creates a stable demand for housing driven by genuine need rather than speculation.

*Low Debt Levels: Around half of owner-occupied properties have no mortgage, and Australia’s residential property market has a comfortable loan-to-value ratio of about 21%.

Australia’s strong economy, low unemployment rates, and stable financial environment support the housing market.

Mortgage default rates remain low, suggesting most Australians can manage their home loans even during challenging times.

Although the market isn’t a Ponzi scheme, housing bubbles can occur when speculative buying pushes prices higher without real demand for accommodation.

Past examples include the speculative property mining boom, which collapsed when the underlying demand vanished.

Australia’s housing market remains a stable and attractive investment for those with a long-term focus, as it is supported by genuine demand, low debt levels, and strong economic fundamentals.

It's a question that echoes through conversations among frustrated Australians, especially younger generations who find themselves priced out of the housing market: Is this all a Ponzi scheme?

The surge in property prices over the last few years has not only locked out many potential first-time home buyers but has also sparked a fiery debate about the sustainability and ethics of our housing economy, likening our housing markets to a speculative Ponzi scheme.

Is this really true?

So what is a Ponzi Scheme?

A Ponzi scheme is a fraudulent investment scheme where returns are paid to earlier investors using the capital contributed by newer investors rather than from legitimate profits generated by the scheme.

The scheme's operators typically entice investors with promises of high returns that are too good to be true and often use various tactics to create the illusion of a profitable investment opportunity, such as falsifying financial statements, creating fake investment portfolios, or using high-pressure sales tactics.

The Ponzi scheme typically collapses when it becomes impossible to find enough new investors to pay returns to earlier investors, or when investors start to withdraw their funds.

At this point, the scheme's operators may abscond with the remaining funds or face legal action.

This kind of scheme is named after Charles Ponzi, who in the 1920s, crafted a notorious plot based on redeeming postal stamps.

Ponzi promised investors high returns of 50% in 90 days, but in reality, he was using the funds of newer investors to pay off earlier investors.

The housing market through a frustrated lens

For many young Australians, the relentless climb of housing prices feels eerily similar to a Ponzi scheme.

They see a market that seemingly only rewards those who entered early, with latecomers paying increasingly higher prices for the same homes.

This perspective is fuelled by their experiences of being consistently outbid and priced out in a market that demands new buyers at ever-higher prices to sustain itself.

Economic growth vs. market sustainability

Critics, particularly from younger demographics, argue that the market's dependence on continuous population growth via immigration and the inflow of new buyers resembles the unsustainable "new money" reliance of a Ponzi scheme.

If these elements were to stall, they fear a catastrophic collapse akin to those that befall fraudulent financial systems.

However, while I can understand the frustrations, their analogies oversimplify complex market dynamics.

The truth is that the Australian housing market is underpinned by strong fundamentals.

1. Our housing markets are underpinned by a high proportion of owner-occupiers.

One of the key factors that support the Australian housing market is the high rate of owner-occupancy in the Australian housing market.

According to the Australian Bureau of Statistics, currently, just under 70% of all residential properties in Australia are owner-occupied.

This means that the majority of homes are owned by individuals and families who are living in them, rather than by investors who are purchasing properties for the purpose of speculation.

This high rate of owner-occupancy creates a stable base of demand for housing that is not driven solely by speculation.

In contrast, in some other countries, such as the United States and New Zealand, there is a much lower rate of owner-occupancy, which has led to higher levels of speculation in the housing market.

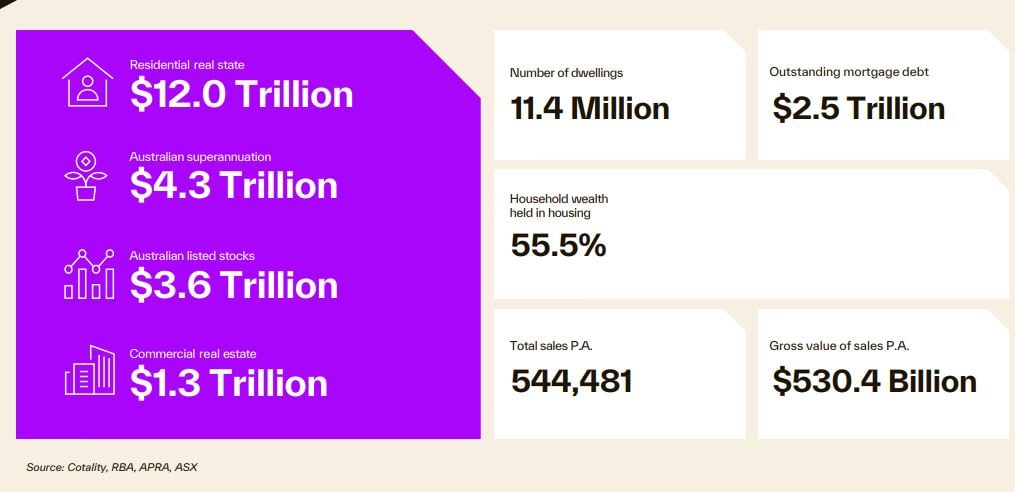

Another important factor that supports the Australian housing market is the low levels of debt held by owner-occupiers.

Note: Around half of all owner-occupied properties in Australia have no debt against them.

This means that a large portion of the housing market is not reliant on high levels of debt, which can be a major concern in discussions about Ponzi schemes.

In fact, it is estimated that the total value of the residential property market of 11.4 million dwellings in Australia is $12 trillion, and there is only $2.5 trillion in debt against this.

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:This week’s Australian Property Market Update – Latest Data, State by State February 24th 2026

That’s a comfortable 21% loan-to-value ratio.

2. Australia’s strong economy

Another key factor that underpins the Australian housing market is our country's strong economic growth and high employment rates.

Australia also has one of the lowest unemployment rates in the world, which creates a stable environment for the housing market and supports the demand for housing.

It also means that despite relatively high interest rates most Aussies can afford to pay their mortgage, and bank mortgage default rates are at extremely low levels.

3. Immigration

Finally, the Australian housing market is underpinned by a growing population, which is driven by both natural population growth and migration.

While migration can be a concern for some and has been cited as feeding “the Ponzi scheme”, it remains a fundamental driver of economic growth and demand for housing.

In particular, skilled migration has been a key factor in the growth of our economy.

Distinguishing between a bubble and a scheme

So if it’s not a Ponzi scheme, are we in a property bubble?

Just to make things clear…a "property bubble" implies a significant overvaluation of property prices, fueled by speculative buying and selling, which is unsustainable over the long term.

This is different from a Ponzi scheme, which is inherently fraudulent and designed to deceive.

In my mind, we are not in a property bubble because our housing markets are supported by demand driven by population growth and a shortage of supply, as well as our strong financial regulatory environment, which ensures that both homebuyers and investors can’t borrow more than they can handle.

More than that, most properties can be bought today below replacement value, since the construction cost of new dwellings, particularly apartments, has skyrocketed over the last couple of years.

But there have been housing “Ponzi schemes” in the past

Property booms usually start with a genuine rise in demand for housing, but sometimes they can turn into speculative bubbles driven by the expectation of higher prices, rather than being based on a genuine need for accommodation.

When this happens, we have the makings of a property market Ponzi.

This was clearly evident in the property mining boom over a decade ago which was based on speculation by investors for property in faraway places with the expectation of continually rising rents and prices.

Of course, when the mining boom finished the property Ponzi collapsed.

This type of crash can only occur in markets controlled by investors, and we are seeing the makings of this in a number of regional locations that have been the targets of inexperienced buyers agents placing their clients into secondary markets with limited stock and pushing up property values well above what locals would ever be prepared to pay.

That is why I only recommend investing in locations that have strong local economic fundamentals and are dominated by affluent owner-occupiers who don't sell up when the property market slows down.

In fact, they’d rather eat Maggi Noodles than sell up their homes.

The bottom line

It is encouraging to understand that Australia’s housing markets are underpinned by the stability of a large percentage of homeowners who have purchased a home to live in rather than chasing cash flow or capital growth.

Our housing markets are resilient because they are underpinned by strong fundamentals, including a majority of owner-occupied properties, low levels of debt, strong economic growth and employment, and a growing population.

As with any market, there are risks and concerns that need to be addressed, but overall, the Australian housing market remains a stable and attractive investment opportunity for strategic investors with a long-term focus.