Key takeaways

The Reserve Bank of Australia (RBA) has already delivered three cuts this year, but another cut in September is unlikely.

Australia’s economy grew 0.6% in the June quarter, with household consumption up 0.9% q/q, showing strong private demand.

Rising inflation, solid GDP growth, and strong consumption make further cuts less urgent.

ANZ Bank still forecasts a November Cup Day rate cut but warns stronger economic data could mean no more cuts at all from here.

Dwelling approvals: Fell 8.2% in July, driven by a sharp 22.3% drop in apartments/units, while private houses edged up 1.1%.

Limited new supply may further tighten the housing market and add upward pressure on prices and rents.

Australia is currently experiencing a rental and affordability crisis.

Population growth is surging, vacancy rates are at record lows, and property values and rents are climbing.

And yet, despite this overwhelming demand, we're not, just not, building enough new dwellings.

Have you ever wondered what the real fix for Australia’s housing crisis might be?

Well, it’s probably not what you think.

Here’s the surprising truth – the only way we’re going to solve this crisis is if house prices actually rise.

Sounds counterintuitive, doesn’t it? Maybe even a little controversial. But unless prices climb high enough to make new developments viable, we simply won’t get the apartments and new homes we so desperately need.

According to CBRE, Australia will complete just 52,500 new apartments in 2025, down from more than 64,000 last year. That’s 30,000 fewer homes than forecast only two years ago

The reason is simple: the economics don’t stack up. Developers can’t sell apartments at prices high enough to cover today’s construction costs. Feasibilities remain about 20% underwater, which means that if developers build now, they’ll lose money.

The gap between what it costs to build and what people can pay has never been wider.

In this week’s Property Insiders chats Dr. Andrew Wilson and I discuss why we’re not building enough, what’s really driving this shortage, and what it all means for property values and rents moving forward.

Why the numbers don’t work

The gap between what it costs to build and what people can pay has never been wider.

- Construction costs jumped 38% in just three years to mid-2023.

- Land costs and government levies remain high.

- Banks still demand 70–75% of presales before financing new apartment developments, but buyers are reluctant to commit to off-the-plan.

- Developers traditionally expect 20% margins – margins that are impossible to achieve right now.

Even looking out to 2030, international property consultants CBRE expect total completions to undershoot earlier forecasts by around 50,000 apartments. That’s a massive shortfall at a time when demand is only intensifying.

The problem is demand isn’t slowing down – it’s accelerating.

- Immigration is expected to add over 2 million people by 2030, primarily to Sydney, Melbourne, and Brisbane.

- Household incomes are projected to rise from $110,000 to $140,000 by 2030, boosting borrowing power.

- Median apartment rents are tipped to grow another 24% by 2030 by CBRE, pushing Sydney two-bedders past $1,000 a week.

- Vacancy rates that are already at record lows are forecast to fall further.

Put simply, more people with more income are chasing fewer homes.

The geography of the shortfall

The supply gap isn’t evenly spread across Australia – but every major city faces challenges:

- Sydney: CBRE forecasts that deliveries will average 17,000 new apartments per year from 2025–30, while demand exceeds 20,000 annually meaning vacancy rates could fall to 1.2%.

- Melbourne: CBRE forecasts that supply will average just 30,000 new apartments per year over the next five years, 25% below Sydney, despite similar demand.

- Brisbane: CBRE forecasts delivery will average 6,000 fewer apartments annually than required.

What this means for investors

If you’re an investor, the message is clear.

- Also read:Brisbane housing market update | September 2025

- Also read:Sydney housing market update | September 2025

- Also read:National Vacancy Rates Hold Steady at 1.2% in August | SQM Research

- Also read:The Surprising Fix for Our Housing Crisis: Property Prices Must Rise | Property Insiders

- Also read:Melbourne housing market update | September 2025

- Rents will keep rising: Scarcity guarantees upward pressure.

- New apartments will need to command premium prices. Interestingly new stock already rents for 10–20% more than older stock.

- Existing stock will gain value: As replacement costs climb, established apartments will look cheaper by comparison, pushing up property values.

The surprising solution: prices must rise

And this brings us back to the uncomfortable truth that I mentioned at the beginning of this article.

Our housing system is market-led. Developers won’t build unless it’s profitable. An right now, it isn’t.

So the solution is that property prices must rise.d

Only when established apartment values climb closer to construction costs will more projects stack up. Only then will banks finance them, developers commit, and builders break ground.

It’s a bitter pill, because higher prices make affordability worse in the short term. But without it, supply will keep shrinking, and the crisis will get worse.

The solution to our housing crisis isn’t more supply, as many commentators suggest, because at current economics, we simply won’t build enough.

Instead, the only way to unlock more supply is for prices of established properties. to rise, closing the gap between costs and values.

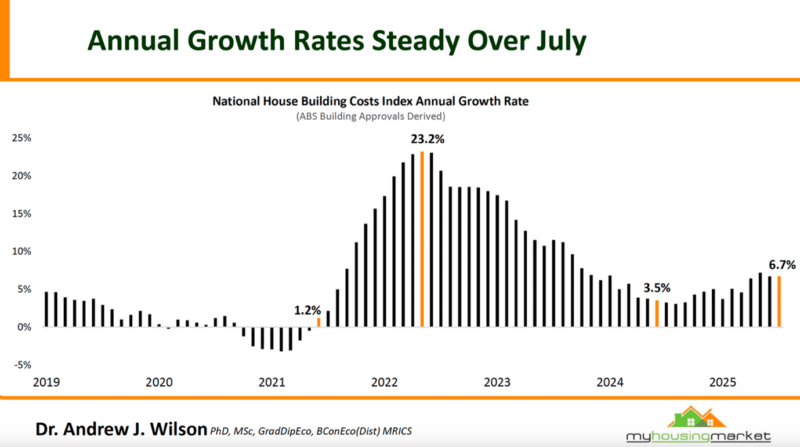

Watch this week’s Property Insiders chat as Dr. Andrew Wilson explains how house building costs rose by around 6.7% over the last year.

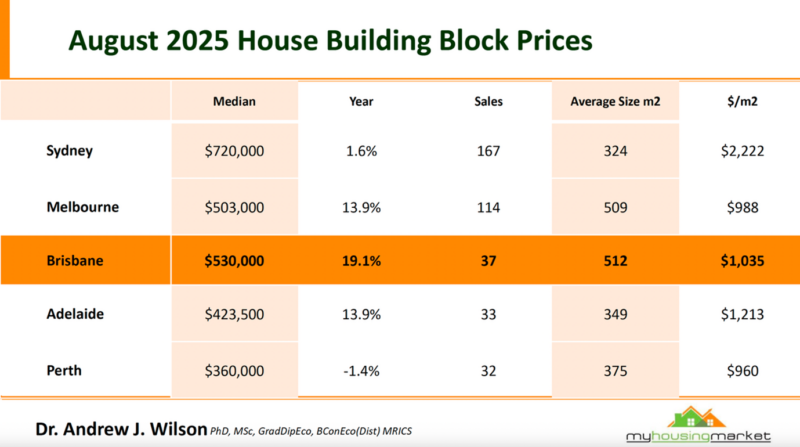

Land prices soar

Watch this week’s Property Insiders chat as Dr. Andrew Wilson explains how much the cost of land in new housing estates has risen over the last year.

We discuss how red tape, green tape and development levies at all levels of government have pushed up the cost of developing new estates.

The table below highlights two interesting things:

- The average new building block is much smaller than the old days when we expected a “quarter-acre block.”

- The cost of new land has soared, particularly in Brisbane, where only 37 new building block sales occurred last month..

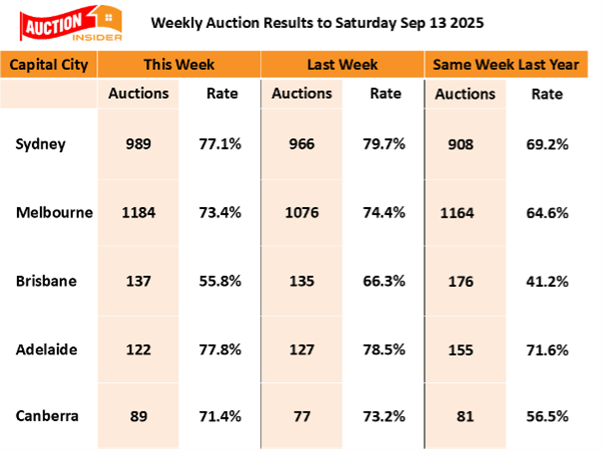

Auction numbers surge into Spring – strong clearance rates steady

Watch this week’s Property Insider chat as Dr. Andrew Wilson reports that auction numbers have surged over the early weeks of spring, with strong clearance rates remaining steady despite more choices for buyers.

The national weekend auction market reported an average clearance rate of 71.1% over the past week, which was lower than the 74.4% reported over the previous week, but well ahead of the 60.6% reported over the same week last year.

Auction listings will continue to rise over the next week, with another surge expected before a lull for the football grand finals weekend.