Key takeaways

The Reserve Bank lifted the cash rate to 4.35% in May, its third hike in a row

Monetary policy is now well placed to monitor the impacts of the conflict in the Middle East on the Australian economy, according to the central bank

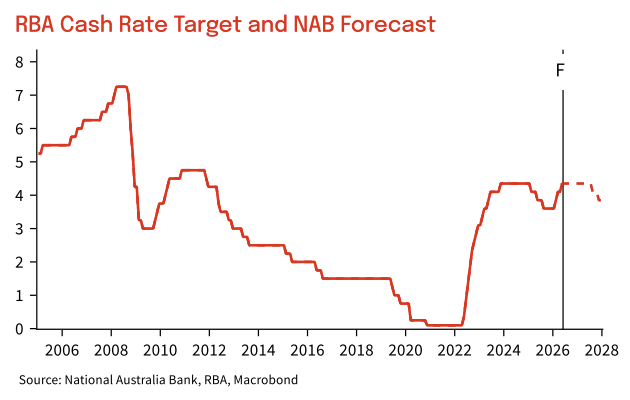

CBA economists’ now forecast for interest rates to be on hold for the remainder of 2026.

Similarly, the NAB now believes there will be no further interest rate rises, and the cash rate will fall next year.

After three consecutive rate hikes, Australia's largest bank is now saying the RBA is most likely done tightening - and that's worth paying attention to.

CBA economists expect the cash rate to remain on hold for the rest of 2026, following the RBA's decision in May to lift rates to 4.35%.

CBA Head of Australian Economics Belinda Allen said guidance from the RBA post their meeting reinforced the view that policy settings are likely to remain unchanged, though she noted the risks sit towards another rate increase if the data warrants it.

Similarly the NAB no longer expect the RBA to hike rates in August, and now see the cash rate peaking at the current rate of 4.35% for the cycle.

They forecast the next move in the cash rate is likely to be down, but the timing is uncertain.

In plain terms, the RBA has done most of its heavy lifting and is now in a watching brief.

The recent RBA statement and press conference signalled that interest rate settings are now high enough to give the Board scope to pause and monitor economic developments, particularly around the conflict in the Middle East and its impact on energy costs and inflation.

So what happens next?

CBA's central forecast is for the cash rate to remain on hold at its current level until early 2027, followed by rate cuts at the May and August 2027 monetary policy meetings next year.

The NAB report highlights shifting risks to the RBA outlook; and I believe interest rates will start falling in Q2 2027 and now see the cash rate end 2027 at 3.6%.

The nation's unemployment rate is rising faster than the RBA had forecast, and the economy appears to be entering another per capita recession following a 0.1% decline in per capita GDP in the March quarter - both signs that monetary policy is already doing its job, possibly more aggressively than intended.

- Also read:National Weekly Auction Report – July 25th 2026 | Chilly July Auction Market Concludes with Some Resilient Signs

- Also read:Perth housing market update | July 2026

- Also read:Adelaide housing market update | July 2026

- Also read:Brisbane housing market update | July 2026

- Also read:Sydney housing market update | July 2026

CBA economists expect economic growth to slow below trend through 2026 as higher interest rates and cost-of-living pressures weigh on household spending, with that cooling in demand expected to gradually ease inflation pressures.

At the same time, our housing markets are slowing down, weighed down by affordability issues and falling consumer confidence.

Fact is…rate hikes weigh on sentiment, tighten borrowing capacity, and create hesitation in the market.

If CBA's forecasts prove correct - and rates hold steady before easing in 2027 - we could be approaching one of those quiet windows that long-term investors tend to look back on as an opportunity.

CBA's data shows Australian consumers have remained relatively resilient to date, with limited evidence so far of a broad slowdown in spending despite weak consumer sentiment overall. That underlying resilience matters for the property market too.

I've always said that the investors who thrive are those who make decisions based on where the cycle is heading, not where it's been.

Rates rising sharply over the past months has created genuine affordability pressure - but that same pressure tends to compress supply, moderate new listings, and set the stage for the next growth phase.

Both NAB and CBA does acknowledge there is a degree of uncertainty around the cash rate outlook, and that the risks are tilted towards rates remaining higher for longer, so I wouldn't suggest anyone get ahead of themselves.

What I would suggest is this - if you've been sitting on the sidelines waiting for rates to peak before making your next move, the picture is becoming a little clearer. A pause is in place, and cuts are likely on the horizon.

The investors who position themselves during periods of uncertainty tend to do considerably better than those who wait for certainty before acting.

If you'd like to talk through how the current rate environment affects your property strategy, lock in a time for a chat with one of our wealth strategists at Metropole by clicking here.