Key takeaways

The 2026 budget makes new build properties the most tax-friendly residential option for investors, allowing negative gearing and a choice between the old 50% CGT discount or the new indexation model at sale time.

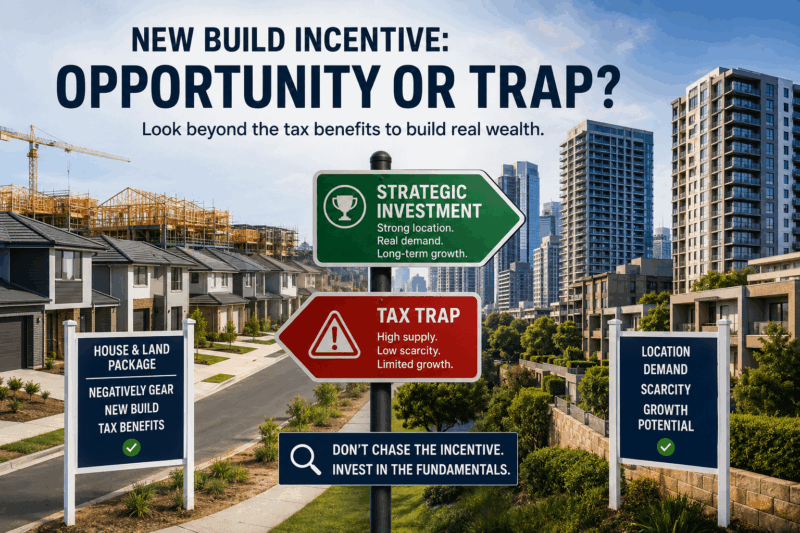

A tax concession can improve the outcome of a good investment, but it cannot turn a poor investment into a good one. The fundamentals - location, land content, scarcity and capital growth potential - have to stack up first.

House and land packages in outer greenfield estates are the most heavily promoted new build option, but competition from surrounding similar properties keeps a lid on resale prices, and distance from employment and infrastructure limits long-term tenant demand.

Off-the-plan apartments in high-density inner city precincts have historically been among the worst performers for capital growth, and adding more investor-targeted stock to already oversupplied precincts doesn't change that dynamic.

Urban infill townhouses in established middle-ring suburbs are the most credible new build option, but they are hard to find, priced accordingly, and not what most investors will end up buying in the rush.

Developers will price the tax premium into new build stock before you make an offer, meaning you could pay above market value on day one for a benefit that doesn't transfer to your buyer when you eventually sell.

When you sell, your exit buyer pool shrinks to owner-occupiers only, since future investors buying your property get no special tax treatment for purchasing a formerly new build.

The test for any purchase under the new rules is simple: would this property still make sense as an investment if the tax concession didn't exist? If the honest answer is no, the tax treatment is doing too much of the work.

Every time the government tinkers with property tax settings, a wave of investors ends up making decisions they later regret.

I'm worried we're about to see it happen again, and on a fairly large scale.

The 2026 federal budget has, quite deliberately, made new build properties the most tax-friendly residential option available to investors.

If you buy a newly constructed dwelling that genuinely adds to housing supply, you can still negatively gear it under the new rules.

You also get to choose at sale time between the old 50% CGT discount or the new inflation indexation model, whichever works out better for you.

On paper, that sounds attractive.

In practice, I think a lot of investors are about to confuse a tax concession with an investment strategy, and those are very different things.

New does not mean good

Over the last few decades, I have been watching investors chase the deal that looks best on a spreadsheet rather than the asset that will actually build their wealth.

The budget has just handed the property marketing industry a very powerful new sales pitch, and I'd encourage every investor to slow down before they respond to it.

Note: A tax benefit can improve the outcome of a good investment. It cannot rescue a poor one.

The fundamentals that determine whether a property builds your wealth - location, land content, owner-occupier demand, scarcity, long-term capital growth - don't change because the tax treatment has shifted.

Those fundamentals have to stack up first, and then you consider the tax outcome as a secondary benefit.

The problem is that the properties most likely to be aggressively marketed as "budget-friendly new builds" are often the very ones that have historically underperformed in capital growth.

The three types of new build you'll be offered - and what to watch for

The new build category covers a range of property types, and they are not all equal.

House and land packages in outer suburban greenfield estates will be the most heavily promoted.

They're easier to sell in volume, the marketing is polished, and the numbers look reasonable on a yield basis.

But these properties sit in estates full of similar homes, which means lack of scarcity and lower socioeconomic demographic keep a lid on prices at resale.

They're typically a long way from employment centres and established infrastructure, which limits both tenant demand and long-term price growth.

The new home in that estate will always be competing with the next new home being built down the street, and that's not a dynamic that favours the investor who bought in early.

Off-the-plan apartments in inner city precincts are the second category, and these concern me most.

Melbourne and Sydney’s CBD apartment markets is the cautionary tale here - thousands of units built through the 2010s in a wave of investor demand, and many of them have barely moved in value since.

High-rise apartments in high-supply precincts tend to attract investors rather than owner-occupiers, which means the buyer pool at resale is narrow, body corporate costs are significant, and you're always competing with new stock entering the market above you.

The fact that you can negatively gear it doesn't change the supply dynamics in the building next door.

The third category - urban infill townhouses and smaller developments in middle-ring suburbs - is genuinely more interesting, but also much harder to find.

- Also read:Melbourne housing market update | July 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Australian housing market update | July 2026

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

These properties attract owner-occupiers as well as investors, they have real land content, and they sit in established neighbourhoods with existing demand drivers.

If you can find one of these at a sensible price with good bones, the investment case may be sound.

But unfortunately, they're not what most investors will end up buying in the rush.

There's a pricing issue with new builds that doesn't get enough attention.

Developers price new stock to cover land acquisition, construction costs, marketing, margin, and now - increasingly - the tax premium that buyers are willing to pay for the concessional treatment.

That premium gets built into the price before you even make an offer.

So you're potentially paying above what the property would fetch on the open market from day one, in exchange for a tax benefit that diminishes over time and doesn't transfer to the next buyer when you sell.

Then, if ever you want to sell your property, it is now an established property meaning your exit buyer pool shrinks to owner-occupiers, and the property has to perform well enough on its own merits to justify the premium you paid at entry.

Construction costs are also running at levels that make rental yields on new builds tight at best.

After body corporate fees, insurance, property management and maintenance, the cash flow position can be uncomfortable even with negative gearing working in your favour.

What the budget is actually trying to do - and why it may not work

I understand the logic behind the policy.

The government wants to channel private investment into new housing supply rather than have investors compete with first home buyers for established stock.

That's a reasonable goal. The execution is the problem.

Most of the new supply that will actually get built in response to this incentive will be in locations and formats that don't address the undersupply of housing where people actually want to live.

Greenfield estates on the urban fringe don't relieve pressure on the inner suburbs. More high-rise apartments in already oversupplied CBD precincts don't help the families who need a home in a middle-ring suburb near good schools.

The investors who respond most enthusiastically to this incentive will likely end up in properties with limited growth potential, while the locations that have always driven genuine wealth creation - established suburbs with strong owner-occupier demand and scarce land supply - continue to do exactly that, with or without the tax concession.

The question to ask before you buy anything

I keep coming back to this, because I think it's the clearest way to think about the decision in front of you.

Before you buy any property under the new rules, ask yourself whether it would still make sense as an investment if the tax concession didn't exist.

Would you buy it based on its location, its growth potential, its rental demand and its scarcity?

If the honest answer is no, the tax treatment is doing too much heavy lifting, and that's a fragile position to build your wealth from.

The investors who will look back on this period with satisfaction are the ones who kept asking the right questions while everyone around them was dazzled by the wrong ones.

Buy the asset first. Let the tax outcome follow.

If you'd like help thinking through what the right purchase looks like for your situation under the new rules, the team at Metropole is ready to work through it with you. We're much more than just another buyer's agent. We help our clients safely grow, protect, and pass on their wealth.

Click here now to organize a chat with one of our wealth strategists.