Key takeaways

ATO data shows over-60s now account for 27 per cent of all landlords, owning almost 610,000 investment properties - up from around 170,000 in 1999-2000

Under-30s property ownership actually fell by 13 per cent over the same two decades, largely due to rising prices rather than policy changes

Boomer landlords built their portfolios over decades through patient, long-term investing - which is exactly the strategy that works

The structural housing shortage, driven by underbuilding and planning failures, is a bigger cause of affordability pressures than who owns rental properties

Proposed changes to negative gearing and CGT may reduce rental supply and push rents higher, potentially harming the younger Australians they're designed to help

The wealth gap is real, but the solution is more supply and earlier entry into the market - the investment fundamentals haven't changed

There's a headline doing the rounds right now that's being used to stir up generational resentment, and I think it deserves a more balanced read.

A recent article in The Age revealed some striking data from the Australian Taxation Office showing that older Australians - particularly those over 60 - have dramatically increased their share of investment properties over the past two decades, while younger investors have retreated.

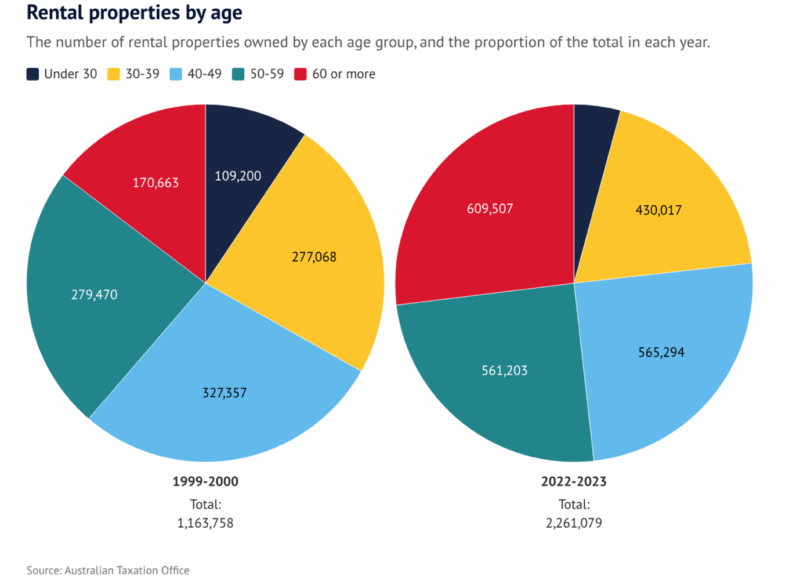

Back in 1999-2000, around 170,000 Australians over the age of 60 were landlords.

By 2022-23, that figure had grown to almost 610,000, representing 27 per cent of all landlords in the country.

Among the over-60s who own six or more properties, the growth was 400 per cent over that same period.

Meanwhile, under-30s ownership of rental property actually fell by 13 per cent over the same two decades.

Source: The Age

On the surface, this looks like an unfair story, but I'd encourage you to look at it differently.

This Is What Wealth Accumulation Actually Looks Like

The whole premise of long-term property investment is that you build your portfolio gradually, over many years, using equity, compounding growth, and time in the market to do the heavy lifting.

Of course, people who have been investing since their 30s and 40s now own more properties in their 60s. That's the entire point.

Boomers didn't wake up wealthy.

They started investing when they were young, held through multiple downturns, built equity patiently, and kept adding to their portfolios as their financial position improved.

Note: The wealth Boomers accumulated is a direct result of disciplined, long-term thinking - precisely the approach I've been promoting for decades.

This ATO data actually confirms something I've always believed: property investment rewards patience and persistence above all else.

The Tax Settings Helped - But They Weren't the Only Factor

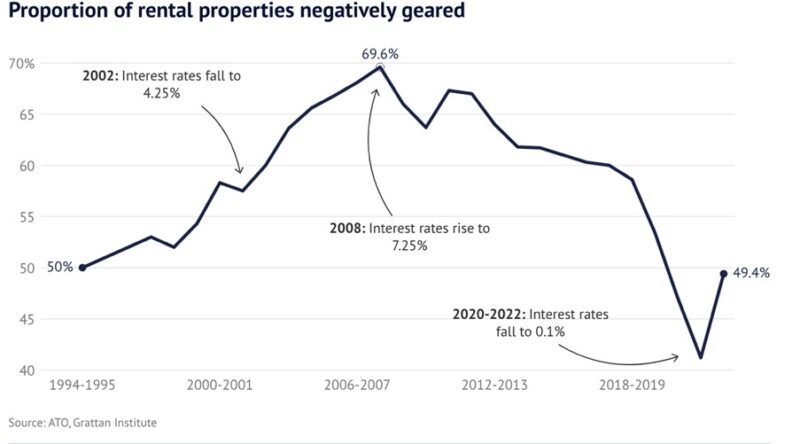

The article draws a line from the Howard government's 1999 capital gains tax changes - which introduced the 50 per cent CGT discount - to the surge in investor activity among older and wealthier Australians.

There's some truth to that.

The CGT discount did make property investment more attractive, particularly for those on higher incomes who stood to benefit most from the tax concession.

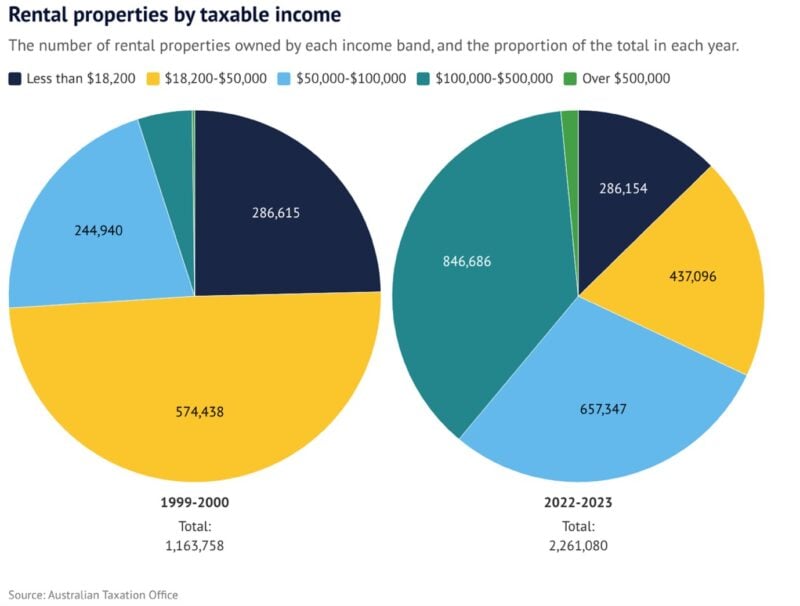

And the data does show that people earning between $100,000 and $500,000 went from holding less than 5 per cent of all rental properties in 1999-2000 to more than 37 per cent two decades later.

Source: The Age

But let's be honest about what else happened over that period.

Sydney's median house price climbed fourfold to $1.5 million. Melbourne's rose by 260 per cent to around $900,000. Average mortgages in both cities nearly tripled.

So this wasn't just about tax. It was about decades of sustained capital growth in Australia's major cities.

Those who got in early and stayed in were rewarded by the market itself, while those who sold too soon, or never started, missed out.

Is It Unfair to Younger Generations?

I understand why young Australians look at this data and feel frustrated.

The barriers to entry in our capital cities are genuinely steep.

But I do want to push back on the idea that boomer landlords are the cause of younger people's challenges.

The real culprits are more structural: chronic underbuilding of new housing stock over decades, planning systems that have consistently blocked density, and a construction industry struggling to keep pace with population growth.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:53 years of valid reasons not to invest

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

The government itself acknowledged this when Treasurer Jim Chalmers told Channel Seven that boosting supply remains "the main game" for helping younger Australians into the market.

The National Housing Supply and Affordability Council has projected that Australia will build around 980,000 homes by mid-2029 - more than 200,000 short of the government's own 1.2 million target.

Removing boomers from the investment market doesn't build a single new home. Reforming the planning system does.

What About Negative Gearing and CGT Changes?

The article raised the prospect of changes to both negative gearing and the capital gains tax concession in the budget next week, with some economists and commentators arguing these reforms would free up properties for younger buyers.

I'm sceptical, and the evidence backs up that scepticism.

When Labor proposed similar changes back in 2019, analysis consistently showed the effect on prices would be modest at best.

The bigger risk is that investors exit the market, reducing the supply of rental properties, and pushing up rents - making things worse for the very people these policies are meant to help.

Treasurer Chalmers has already signalled that any changes would likely grandfather existing investments, recognising that people have made decisions in good faith under the existing tax settings.

I think that's the right instinct - you don't pull the rug out from under people who invested legally under the rules that applied at the time.

Source: The Age

The Right Lesson From This Data

If I were a younger Australian reading that Age article, here's how I'd think about it.

The boomers who now own six or more investment properties didn't get there because the system was rigged in their favour.

They got there because they started early, invested in quality assets in the right locations, used leverage wisely, and held through the tough periods when sentiment was weak and others were selling.

Sure, that path is harder today than it was in 1990 - there's no point pretending otherwise.

Entry prices are higher, borrowing costs are steeper, and the first property is a genuine stretch for most people under 35.

But the underlying strategy is exactly the same.

You start with what you can afford, in the best location you can manage, and you hold it. You build equity. You leverage that equity into a second property. You repeat the process.

Note: The boomer landlords aren't the problem to be solved. They're the proof of concept.

What You Should Do Now

If you're a property investor looking at this data and wondering whether the window is closing, I'd argue the opposite.

Markets like Melbourne are currently undervalued relative to their long-term fundamentals, and that won't last forever.

The investors who look back in twenty years and feel satisfied with where they ended up will be the ones who made clear-headed decisions now, when the media was focused on generational division rather than market opportunity.

At Metropole, we help our clients cut through exactly this kind of noise.

We're much more than just another buyer’s agent.

We build long-term property strategies around the assets and locations with the strongest structural drivers of growth - and we help our clients hold them through the cycles that others find so unsettling.

If you'd like to have a conversation about building a portfolio that still works in the decades ahead, have a chat with one of the Wealth Strategists at Metropole – just click here and find a time that suits you.

You can contact us at metropole.com.au or call 1300 20 30 30.