Key takeaways

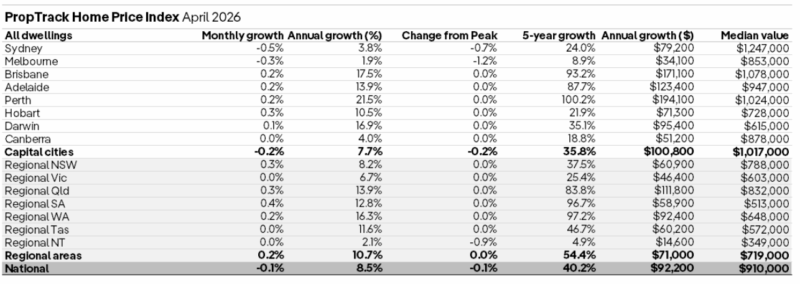

National home prices fell 0.1% in April according to Proptrack, marking the first monthly decline in 2026, and taking the national median home value to $910,000.

Prices remain 8.5% higher than a year ago adding around $92,200 to the value of the median home.

Capital city prices fell 0.2% over the month but remain 7.7% higher than a year ago, with the median home value now $1,017,000.

Hobart (+0.3%) recorded the largest monthly rise among capital cities, followed by Brisbane, Adelaide and Perth (+0.2%).

Sydney (-0.5%) and Melbourne (-0.3%) were the only capital cities to record price declines in April.

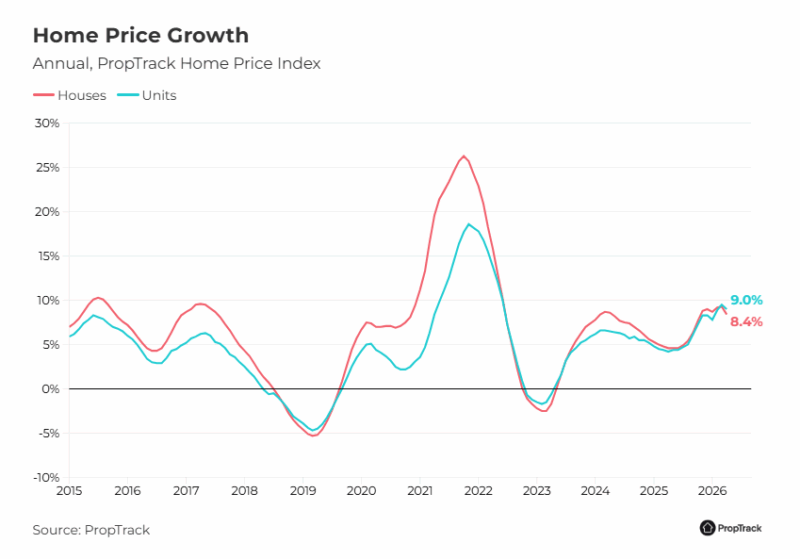

Price falls were driven by houses, with capital city house prices down 0.2% in April, while unit prices were flat, pointing to stronger demand for more affordable stock as borrowing capacity remains constrained.

Perth remains the fastest growing capital over the year (+21.5%), followed by Brisbane (+17.5%), Darwin (+16.9%) and Adelaide (+13.9%).

Regional prices rose 0.2% in April and were up 10.7% year-on-year. Regional growth continues to outpace the capitals over the past year (+10.7% vs +7.7%) and five years (+54.4% vs +35.8%), supported by relative affordability and lifestyle appeal.

National home prices in April marks a turning point in the housing cycle according to PropTrack, which reports that national home prices fell 0.1% in April, marking the first monthly decline in 2026, and taking the national median home value to $910,000.

However, prices remain 8.5% higher than a year ago, adding about $92,200 to the median home's value.

Ms Eleanor Creagh, PropTrack's Senior Economist said:

"Momentum has clearly slowed, marking a transition from broad-based growth to a more uneven, multi-speed phase.

Nearly half of SA4 regions recorded price declines in April, highlighting a clear and broad-based loss of momentum across the housing market."

Note: The latest Proptrack report highlights that rate-sensitive inner-city markets are leading the shift, particularly in Sydney and Melbourne, where price declines have emerged after back-to-back interest rate rises.

In contrast, more affordable markets, particularly across parts of Perth, Adelaide and regional areas continue to record strong annual growth.

However, even in these markets, short term growth momentum is beginning to ease, indicating that the slowdown is becoming more widespread.

Ms Creagh further said:

- Also read:Australian housing market update | June 2026

- Also read:This week’s Australian Property Market Update – Latest Data, State by State June 16th 2026

- Also read:Melbourne housing market update | June 2026

- Also read:National Vacancy Rate Holds at 1.2%| SQM Research

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

"Overall, the housing market is rebalancing as demand softens and growth momentum eases.

Auction clearance rates have softened, pointing to a growing mismatch between buyer and seller expectations.

At the same time, higher interest rates are reducing borrowing capacity, while uncertainty is weighing on confidence."

Outlook

According to the report, while price growth is expected to slow, a large correction remains unlikely.

Strong equity buffers, a resilient labour market and limited forced selling are helping to stabilise conditions and cushion price falls.

Population growth and ongoing supply constraints, exacerbated by higher construction costs and elevated interest rates, continue to place a floor under prices.

The adjustment is expected to be gradual, but slower growth and further price declines are likely.