Key takeaways

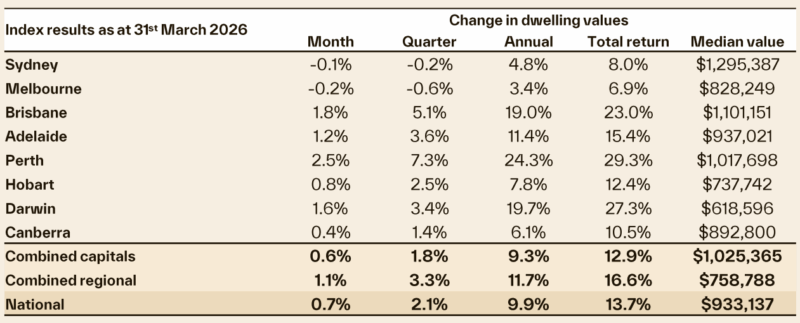

Cotality’s national home value index rose 0.7% in March, taking dwelling values 2.1% higher over the first quarter of the year.

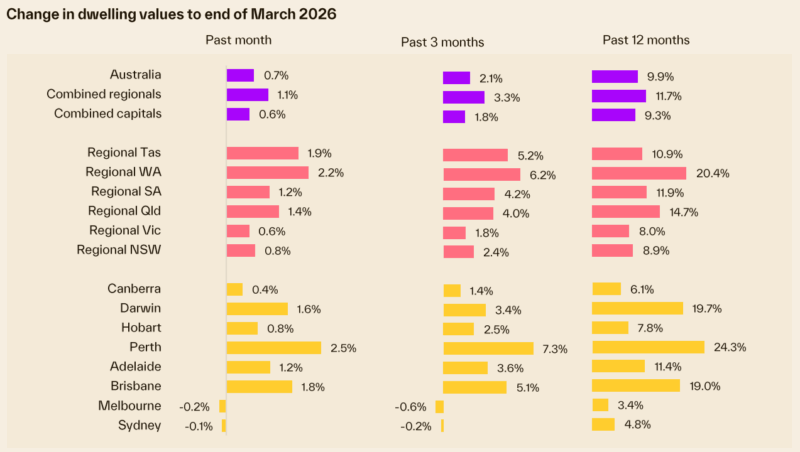

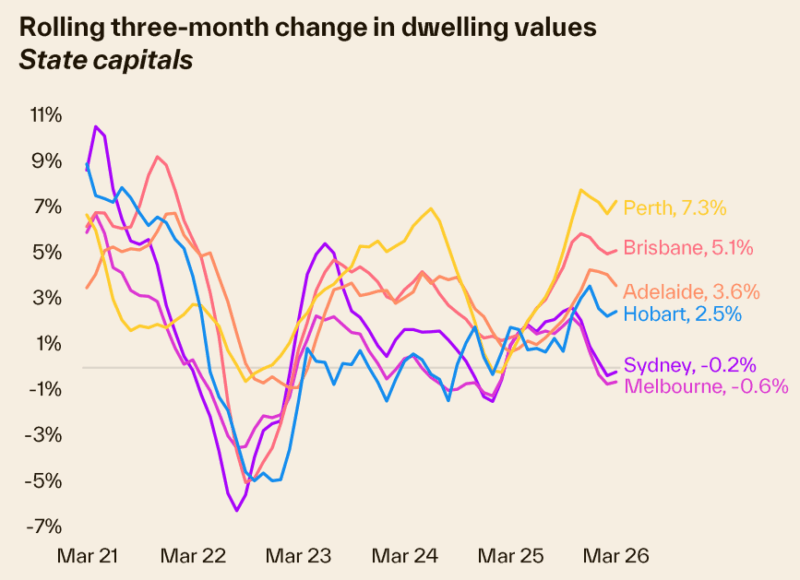

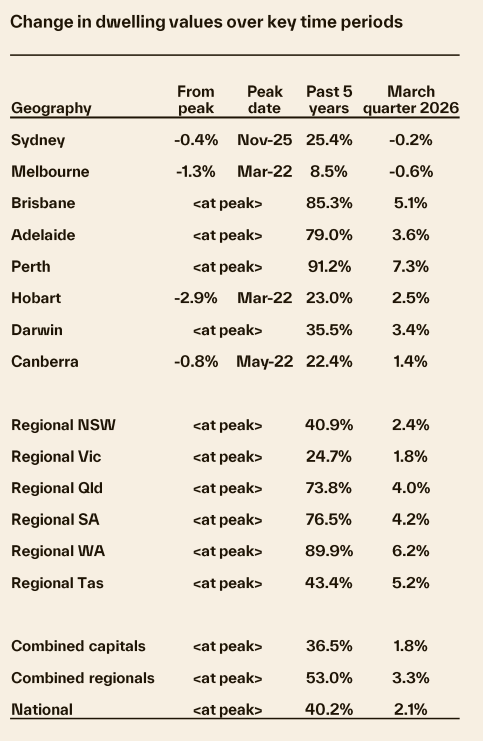

Perth surged 7.3% over the quarter, while Melbourne values are down -0.9% from the November high and the Sydney market is down -0.4%.

Sydney upper quartile values fell 1.8% through the March quarter, while lower quartile values are 1.8% higher.

Overall, early 2026 conditions are shaping up to be more cautious and sensitive to debt servicing shocks, as geopolitical uncertainty and cost-of-living pressures weigh heavily on consumer sentiment.

Cotality’s national home value index rose 0.7% in March, taking dwelling values 2.1% higher over the first quarter of the year.

At the national level, the pace of gains is easing, reducing from a 2.8% increase in Q4 last year, but housing outcomes are increasingly diverse from city to city and across the pricing spectrum.

The mid-sized capitals, as well as Darwin, are all recording growth of 1.2% or more on a month-to-month basis, while Sydney and Melbourne navigate a subtle decline trend that has been evident since December last year.

Since the end of November 2025, Melbourne values have retreated by -0.9% and the Sydney market is down -0.4%.

The softer trend in values coincides with falling auction clearance rates and a pickup in advertised supply, providing buyers with more choice and less urgency at the negotiation table.

At the other end of the spectrum, the trend in Perth home values is showing the opposite trend, accelerating in the face of higher interest rates and lower sentiment.

Housing values across the western capital were up 2.5% in the month of March to be 7.3% higher over the quarter.

In dollar terms, the 7.3% rise in Perth home values over the quarter has added approximately $69,000 to the median dwelling value.

Clearly this pace of growth is unsustainable, but continues to be supported by low supply, with advertised stock levels tracking about 40% below the five-year average for this time of the year.

Conditions are also diverging across the broad value tiers, with lower quartile markets leading the pace

This trend is evident across every capital except Hobart and Canberra, but most pronounced in Sydney where upper quartile dwelling values have fallen by 1.8% through the March quarter while lower quartile values are 1.8% higher.

Strength across the lower quartile value tier is tied to increased competition for lower priced housing.

Serviceability constraints are deflecting buyer demand towards the lower end of the market, competing with a pickup in first home buyers taking advantage of stimulus and elevated levels of investor activity.

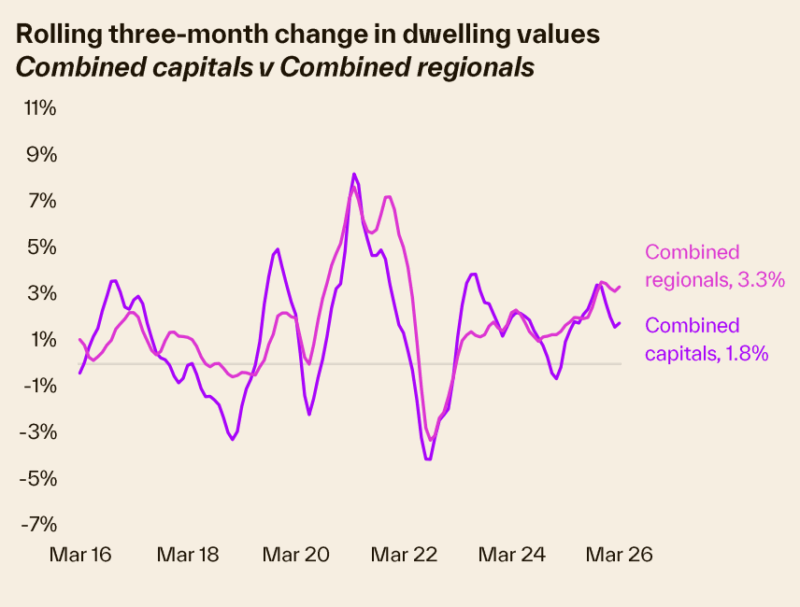

Regional markets are showing some resilience to the slowdown

Values rising 1.1% over the month and 3.3% over the quarter, compared with 0.6% month on month and 1.8% quarter on quarter rises across the combined capital cities.

Similar to the strength in Perth, Regional WA stands out with the strongest capital gains.

Values are up 2.2% in March to be 6.2% higher over the quarter.

WA’s Bunbury is leading the pace of gains, with values jumping 8.4% through the March quarter to be 22.2% higher over the past 12 months.

There are some early signs of an easing in purchasing demand, with Cotality’s estimate of quarterly home sales tracking 1.9% lower than a year ago and 5.6% down on the five-year average.

Given the likelihood of a further rise in cost-of-living pressures and interest rates, alongside a drop in confidence as conflict in the Middle East extends, it’s likely that purchasing demand will continue to reduce over the coming months, supporting a further slowdown in housing values.

Outlook

The housing market is facing a worsening mix of cyclical and external headwinds which are set to weigh on housing demand.

Prior to the Iran conflict, affordability was already stretched, sentiment was easing and higher interest rates have reduced borrowing capacity.

More recently, higher energy costs and a sharper fall in confidence have added to the caution, particularly for discretionary and higher priced purchases.

On affordability, dwelling values relative to household incomes are at record levels, and higher mortgage rates are increasingly weighing on borrower serviceability assessments.

Factoring in the three-percentage point serviceability buffer, most borrowers effectively need to show they can service a new loan with a mortgage rate around 9.0%.

- Also read:Australia’s jobs boom raises the risk of another interest rate rise | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:National Weekly Auction Report – July 25th 2026 | Chilly July Auction Market Concludes with Some Resilient Signs

- Also read:Perth housing market update | July 2026

In our view, that combination of affordability and serviceability constraints is shrinking the pool of buyers who can comfortably transact, with the impact most visible across the higher price points of the market.

At the same time, wage growth is not keeping pace with inflation, so real incomes are under downward pressure.

That reduces households’ ability to absorb any further lift in repayments and reinforces a ‘wait and see’ approach to high commitment financial decisions like purchasing a home.

Higher energy prices are an added downside risk. Higher fuel and utility bills squeeze discretionary income and amplify cost of living pressures at a time when mortgage repayments are already elevated.

Demographics are also less of a tailwind than they were.

Population growth has largely normalised after the post COVID catch up.

While population gains still add to underlying housing demand, they are increasingly being offset by affordability constraints, tighter credit conditions and uncertainty around future household expenses.

Confidence has deteriorated through the month as cost of living pressures and geopolitical uncertainty have intensified.

Consumer sentiment surveys have weakened materially.

Historically, housing activity has followed trends in consumer sentiment.

Softer selling conditions can be seen in auction clearance rates, which have eased to below average levels, while advertised stock levels have been lifting, particularly in Sydney and Melbourne, implying less urgency from buyers and a gradual shift toward more balanced conditions.

On the flipside, supply remains tight in aggregate, which should help limit the risk of a sharp price correction.

That said, there are early signs of some easing at the margin; new listings have picked up, and construction activity has improved modestly in a number of states.

A sustained supply recovery still looks difficult.

Construction costs remain elevated and are set to face renewed upward pressure via higher fuel and material costs, which will weigh further on feasibility.

Even a small lift in supply, however, reduces the sense of scarcity that has been supporting price growth.

The labour market remains a key stabiliser. Employment is still high and conditions are tight, which supports income security and reduces the risk of forced selling, even as real incomes are squeezed and sentiment is weaker.

Also, policy support is still present for first home buyers.

The deposit guarantee scheme can help first home buyers clear the upfront deposit hurdle in lower priced segments, however, strong price growth in those segments, together with higher interest rates and living costs, means stimulus is likely to have diminishing impact from here.

Overall, early 2026 conditions are shaping up to be more cautious and more sensitive to debt servicing and cost of living shocks.

With inflation and interest rate uncertainty still front of mind, confidence weaker and listings rising, the near term balance of risks is tilted to the downside.

Tight supply and labour market resilience should provide a floor, but the scope for broad based price gains looks limited.

We expect outcomes to remain uneven through 2026.

More affordable segments may hold up better as demand concentrates where serviceability still works, while higher value markets face larger headwinds from borrowing constraints and cost pressures.

The key watch points from here are the path of inflation and rates, the extent of any further lift in listings, and whether confidence stabilises.