Key takeaways

Don't expect a rate cut from the RBA. The latest CPI figures have put a pin in that.

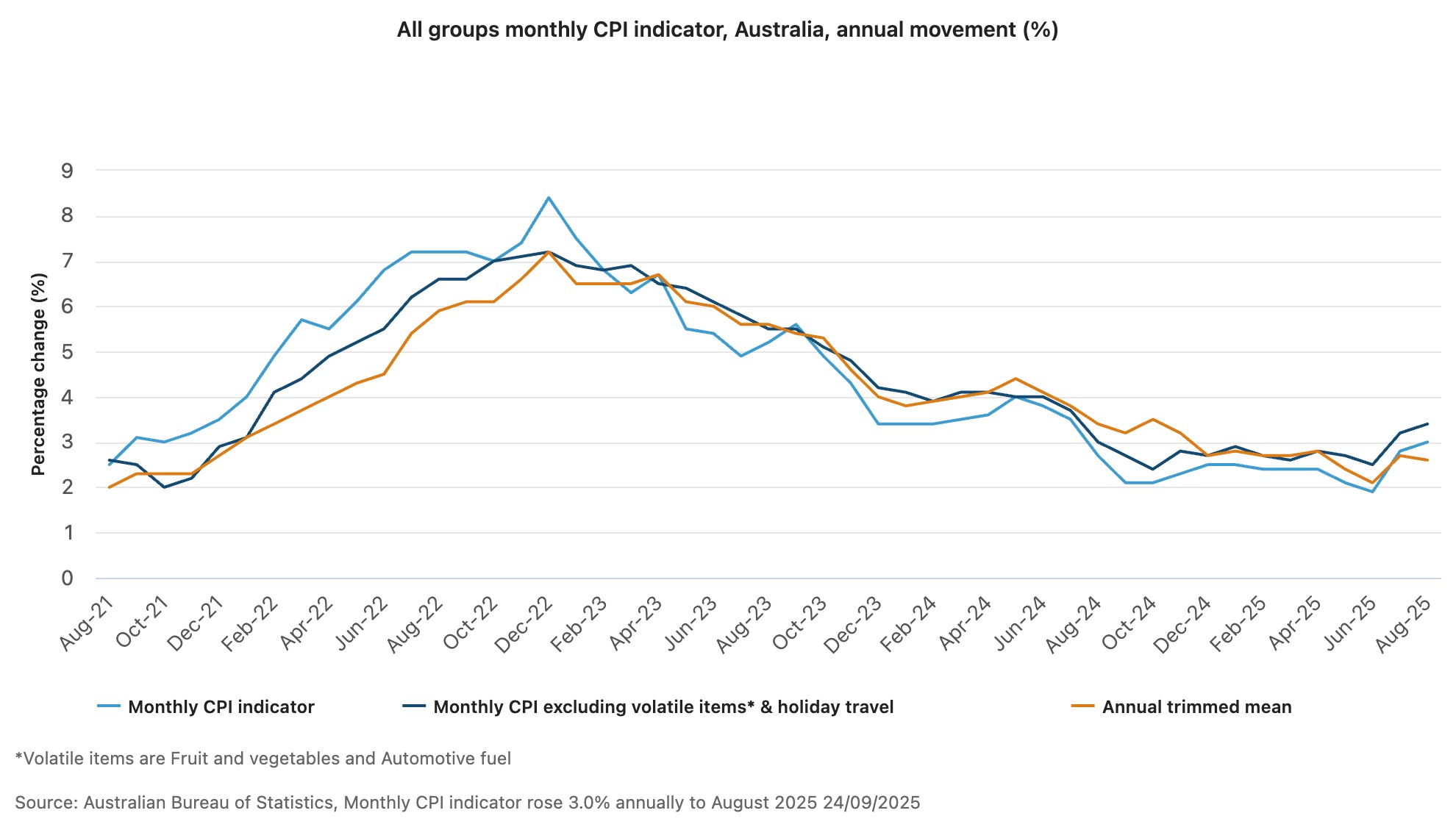

The monthly Consumer Price Index (CPI) indicator rose 3.0% in August, up from 2.8% in the previous month, to the highest level since July 2024.

While the monthly data can provide some insight into what’s happening with prices, it doesn’t yet measure a full basket of goods each month and can be volatile.

Knowing the Board’s strong preference for quarterly inflation data, it will likely wait until the 3-4 November meeting before cutting the cash rate again, provided the September quarterly CPI results, due out on 29 October, remain on track, which is by no means a given.

Don't expect a rate cut any time soon. The latest CPI figures have put a pin in that.

The monthly Consumer Price Index (CPI) indicator rose 3.0% in August, up from 2.8% in the previous month, to the highest level since July 2024.

This figure suggests there is meaningfully more inflation pressure in the domestic economy than the RBA had expected.

However, the policy-relevant trimmed mean inflation moderated to 2.6% in August, down from 2.7% in July.

Michelle Marquardt, ABS head of prices statistics, said:

‘The largest contributors to annual inflation were Housing (+4.5 per cent), Food and non-alcoholic beverages (+3.0 per cent), and Alcohol and tobacco (+6.0 per cent).

When prices for some items change significantly, measures of underlying inflation (like the annual trimmed mean and CPI excluding volatile items and holiday travel) can give more insights into how inflation is trending.

‘Annual trimmed mean inflation was 2.6 per cent to August 2025. This is down from 2.7 per cent to July 2025.

CPI excluding volatile items and holiday travel rose 3.4 per cent in the 12 months to August, compared to a 3.2 per cent rise in the 12 months to July.

Source: ABS

What does this mean for the RBA meeting next Tuesday?

NAB now see the RBA on hold at 3.6% until May - they previously forecast cuts in November and February

NAB Reported:

Today’s CPI data point to a 0.9%-1.0% qoq outcome for Q3 trimmed mean, which would be a 0.3ppt upside surprise to current RBA forecasts.

The detail shows that market services inflation is significantly hotter than we expected. For the RBA, this means considerably less certainty that inflation has settled near 2.5% and highlights the likelihood that it will take a period of modestly restrictive policy for inflation to settle at 2.5%.

Canstar.com.au data insights director, Sally Tindall is a little more optimistic and believes that this CPI results certainly don’t further the case for a cash rate cut next week, however, this data is unlikely to cause the central bank to hit the panic button either.

While the monthly data can provide some insight into what’s happening with prices, it doesn’t yet measure a full basket of goods each month and can be volatile.

Knowing the Board’s strong preference for quarterly inflation data, it will likely wait until the 3-4 November meeting before cutting the cash rate again, provided the September quarterly CPI results, due out on 29 October, remain on track, which is by no means a given

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 14th 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

For a borrower with a $600,000 mortgage at the start of the cuts, a rate cut in November would see their minimum monthly repayments drop by a further $87.

However, with three cuts already in effect, the total drop across the February, May, August as well as a November cut would be $359.

This assumes banks pass this next cut on in full to their variable customers.

| Impact of RBA rate cuts on minimum monthly repayments | ||

| Loan size at start of cuts | Cut in November | Across all 4 cuts (Feb, May, Aug, Nov) |

| $500,000 | -$73 | -$299 |

| $600,000 | -$87 | -$359 |

| $750,000 | -$109 | -$449 |

| $1m | -$145 | -$598 |

| Source: Canstar.com.au. Notes: based on an owner-occupier paying principal and interest with 25 years remaining in Feb 2025 at the RBA average existing customer variable rate. Calculations assume the banks pass on each cut in full to existing variable customers the month after. | ||

Canstar.com.au data insights director, Sally Tindall says,

This latest set of numbers has put a pin in what little hope there was for a September rate cut.

The RBA will look beyond the wild swings in electricity costs driven by state and federal rebates, but it won’t gloss over the recent price hikes, which are likely to be exacerbated when the rebates start drying up over the next few months.

Inflation has got the wobbles and while the RBA gives little weight to this monthly dataset, it’s likely to push the Board to hit the pause button for now.

With the economy picking up pace and unemployment still at a relatively low 4.2 per cent, there’s no urgency to cut.

The Board’s dual mandate is to keep prices in check and Australians in jobs, with the latter gaining prominence in their decision-making.

Keeping the cash rate on hold gives the RBA the chance to review one more round of Labour Force data to better understand how the jobs market is holding up.

A hold next week doesn’t mean we’ve reached the end of the cutting cycle.

There’s still a chance the RBA will cut rates in November, if inflation plays ball. This, however, is by no means a given.

A cut in November, if it materialises, would shave another $87 off the monthly repayments of a $600,000 loan.

That might not sound like much in isolation, but across what would then be four cuts this year, the savings add up to almost $360 a month.

The one rate cut you can bank on is the one you negotiate yourself, either by switching to a lower rate lender or haggling with your current bank.

If you’re an owner-occupier paying down your debt, know that the average variable rate is currently sitting at around 5.53 per cent. If you’re not under this mark, ideally well under, then it’s time to ask yourself why.