Key takeaways

Strong full-time job growth is supporting housing demand. People with secure, full-time work are more confident to borrow and invest in property.

Australia’s low unemployment and high participation rate show a healthy economy. A broad income base is underpinning ongoing demand for housing.

Rising land costs are making new housing increasingly expensive. This creates a price floor under established properties and limits affordable supply.

Supply constraints mean new housing cannot be delivered cheaply or quickly enough. This imbalance continues to favour owners of well-located existing properties.

The market is becoming more fragmented rather than heading for a crash. Strategic investors focusing on quality assets are likely to outperform.

There's something many property investors completely overlook when trying to figure out where the market is heading.

It's not interest rates. It's not auction clearance rates.

It's jobs - and right now, the Australian employment market is sending a very clear signal that the property market has more underlying support than most people realise.

So in today’s Property Insiders chat Dr Andrew Wilson and I unpack three key themes that are quietly shaping the direction of our housing markets.

We’ll start by looking at Australia’s labour market, which remains more resilient than many expected, and why that matters for property.

Then we’ll turn to a factor that doesn’t get enough attention but is having a profound impact on housing affordability and supply - the cost of land which has surged and creates a meaningful floor under the value of established properties.

And finally, we’ll briefly touch on what’s happening at auctions around the country and what that’s telling us about buyer sentiment as listings rise.

The jobs market is telling a story that most investors are ignoring

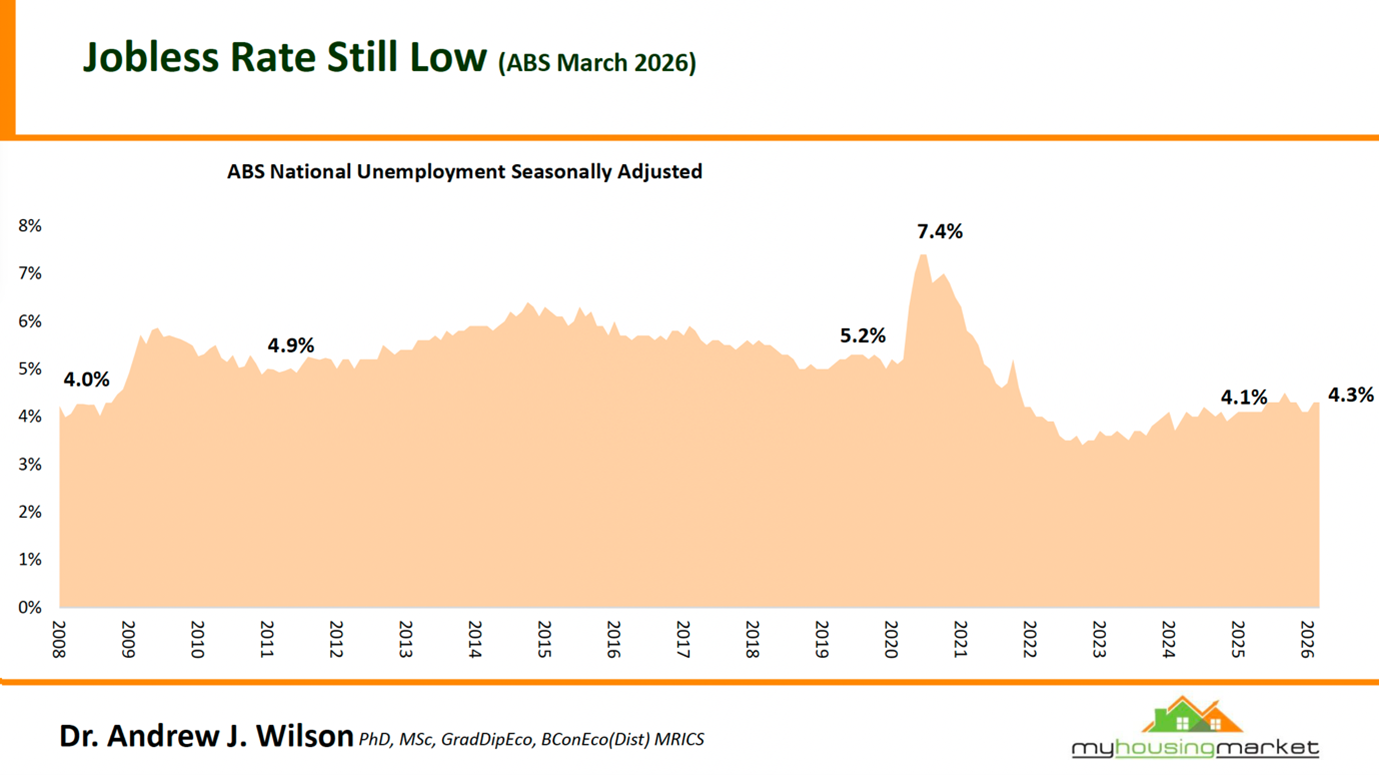

The ABS released the March labour force data last week, and the headline - unemployment holding at 4.3% - was almost universally treated as a non-event.

I think that's a mistake.

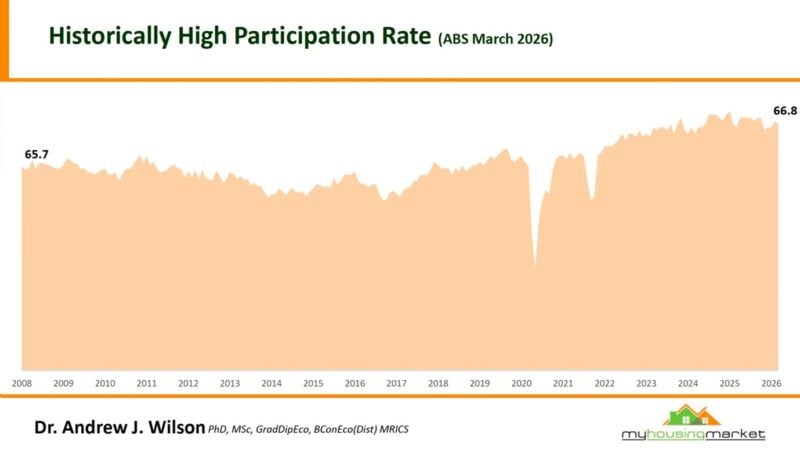

Employment rose by around 18,000 people and the number of unemployed actually fell by 4,000, while the participation rate came in at 66.8%.

But the number that really stands out to me isn't the unemployment rate itself. It's the composition of the jobs being created.

The growth in employment was driven by full-time workers, which rose by 53,000 people in March, partly offset by a fall in part-time employment of 35,000 people.

That distinction matters a great deal. Full-time employment is what gives people the confidence to take on a mortgage, upgrade a property, or commit to a long-term financial decision. Part-time work keeps people busy, but it rarely changes their property ambitions in the same way.

Hours worked also rose by 0.5% over the month, meaning people aren't just employed - they're actually working more. That points to genuine economic activity, not just statistical flattery in the headline figures.

And when you look at the longer trend, both trend employment and hours worked grew by 0.2% in March, while annually, hours worked grew faster at 2.0% than employment growth of 1.4% - which tells you the economy is running with real productive capacity behind it.

Why a low unemployment rate matters more than people think

Watch this week's Property Insider Chat as Dr Andrew Wilson explains how employment security is a critical factor driving sustained housing demand.

People don't buy property when they're worried about their jobs. They buy when they feel secure, when they can see a clear path ahead, and when they have the income to service debt.

Right now, the unemployment rate of 4.3% sits in deeply low territory by historical standards.

When you look at Dr Wilson's long-run chart, it puts today's rate in a different context than what we saw during the GFC, the mining slowdown, or the COVID years.

During COVID, unemployment briefly hit 7.4%. Through much of the 2010s, it sat above 5%. The current 4.3% reflects an economy that is, in labour market terms, genuinely healthy.

The participation rate of 66.8% adds another layer to this.

Back in 2008 it was sitting at 65.7%, and it spent most of the decade that followed either flat or drifting lower.

The fact that 66.8% of the working-age population is now either employed or actively looking for work means the income base supporting housing demand is broader than it has been at almost any point in modern Australian history.

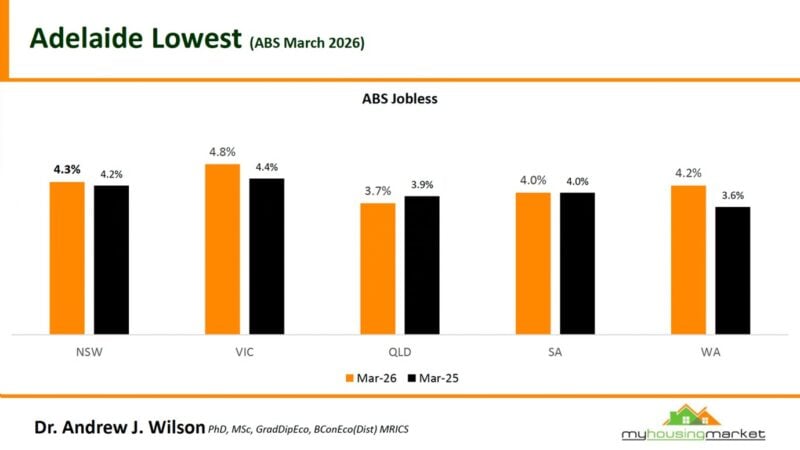

There are differences across the states worth noting.

- Also read:The Economic Signal Most Property Investors Are Completely Overlooking | | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State April 21st 2026

- Also read:Adelaide housing market update | April 2026

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane housing market update | April 2026

Victoria's unemployment rate is 4.8%, which is the highest of the major states, while South Australia sits at 4.0% and Queensland at 3.7%.

These state-level differences do influence local property market dynamics, and it's one more reason why understanding the specific fundamentals of the market you're investing in matters so much more than relying on national averages.

What's happening to land prices should keep investors alert

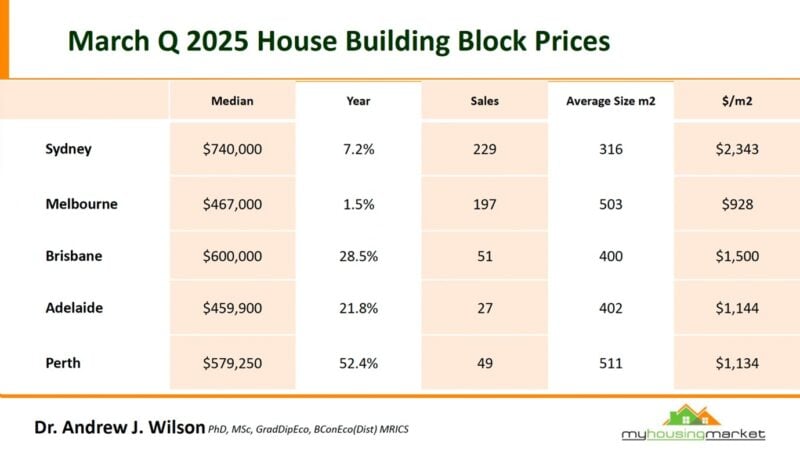

Watch this week's Property Insider Chat as Dr Andrew Wilson shares the latest data on house building block prices for the March quarter 2025, which paints a remarkable picture of just how constrained new housing supply has become.

Sydney remains by far the most expensive market, with a median block price of $740,000, up 7.2% over the year, at $2,343 per square metre for an average lot size of just 316 square metres. That's three-quarters of a million dollars before a single brick has been laid and on small blocks.

But the growth rates elsewhere are even more striking.

Perth's median land price has risen 52.4% in a year to $579,250. Brisbane is up 28.5% to $600,000. Adelaide has climbed 21.8% to $459,900.

Even Melbourne, which has been the most subdued of the major capitals on almost every measure, has seen land prices rise 1.5% to $467,000, though it offers the largest average block size at 503 square metres and the most competitive per-square-metre price at $928.

What these numbers tell us is that the cost of delivering new housing is only moving in one direction, and the idea of meaningfully boosting supply at prices that ordinary Australians can afford is becoming increasingly difficult to achieve.

When land alone costs between $460,000 and $740,000 before you've poured a concrete slab or framed a single wall, the total delivery cost of a new home in most of our capital cities is pushing well above $1 million.

Developers need to achieve prices that reflect that cost, which means new housing can't compete with established property on price, and the supply response that politicians keep promising simply cannot materialise fast enough to change the fundamental demand-supply equation.

For investors who already own well located established properties, this is a meaningful tailwind that doesn't get nearly enough attention.

The replacement cost argument - the idea that what you own would cost substantially more to replicate from scratch today - is as compelling as I've seen it in decades.

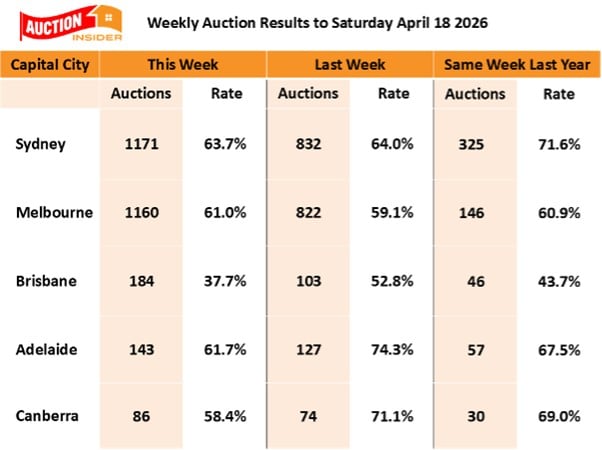

Auction Clearance Rates Generally Lower as Listings Surge

Capital city auction clearance rates were lower over the past week as the recent impact of school holidays diminished, resulting in a predictable surge in listings.

The national weekend auction market reported an average clearance rate of 56.5% over the past week, well below the 64.3% reported the previous week and lower than the 64.3% reported the same week last year, which coincided with the Easter break.

Auction results will continue to reflect the end of the school holiday period with another rise in listings offset by distractions from the upcoming ANZAC weekend.

What this means for property investors

When you put all of this together, a clearer picture emerges.

On the demand side, a strong labour market is continuing to support prices. On the supply side, rising land costs and development constraints are limiting the supply of new housing.

And in the middle, the market is recalibrating as higher interest rates reshape buyer behaviour.

To me, this reinforces a view I’ve held for some time.

We’re not heading for a property crash. We’re moving into a more fragmented market, where some properties will outperform, and others will underperform.

And that means strategy matters more than ever.

Investors who understand the underlying drivers - jobs, population growth, and supply constraints - and who focus on high-quality, well-located assets will continue to do well.

While those who rely on short-term trends or chase hotspots may find the next phase of the cycle a lot more challenging.

If you'd like to understand how the current market conditions affect your specific situation and investment strategy, I'd encourage you to have a conversation with one of the wealth strategists at Metropole. Click here to lock in a time that suits you.