Key takeaways

Rents kept rising through July for both houses and units across most capitals, even though the usual quieter mid-winter period pushed vacancy rates up slightly in some cities.

Sydney continues to hold the title of Australia's most expensive rental market, with houses at $878 a week and units at $845, and both are still climbing.

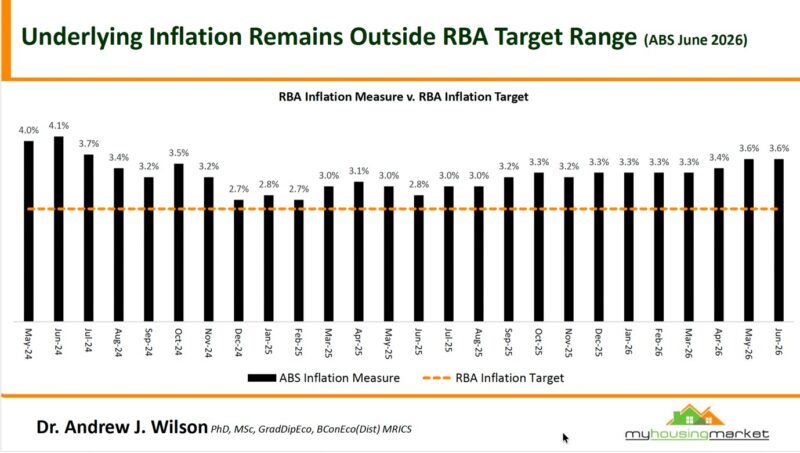

Headline inflation eased to 3.8%, but underlying inflation, the measure the RBA actually watches, held steady at 3.6%, the highest it's been since July 2024.

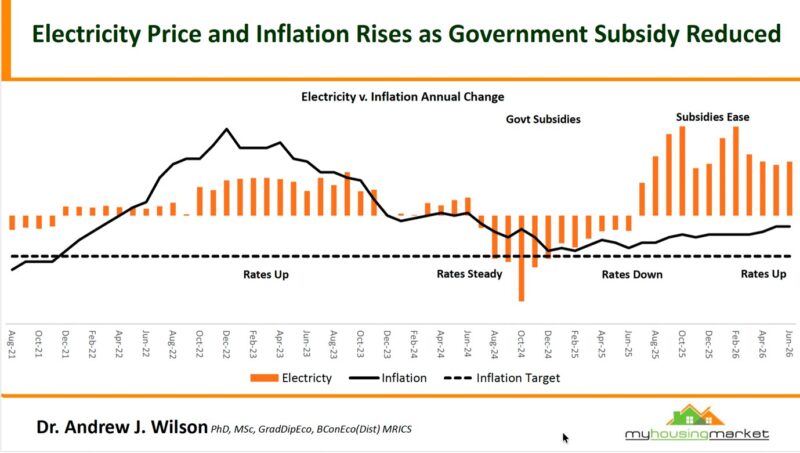

Electricity prices are surging again as government subsidies ease, up 22.4% annually, and that's a big part of why underlying inflation refuses to come down.

Persistent inflation and a resilient labour market leave the door open for another interest rate rise.

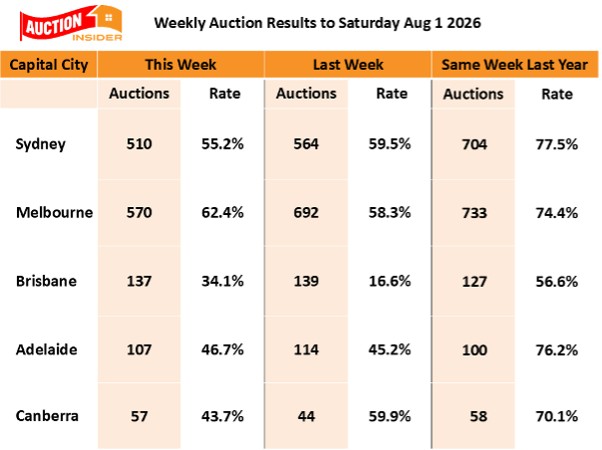

Auction markets opened August with a split result, Sydney clearance rates slipping to 55.2% while Melbourne improved to 62.4%, with no sign yet of the usual end of winter bounce.

The combination of weak buyer sentiment, rising rents and restricted housing supply creates opportunities for strategic investors with strong financial buffers.

Could Australia’s inflation problem be more stubborn than the latest headline figure suggests, and does that leave the door open for another interest rate rise?

Annual headline inflation eased from 4 per cent to 3.8 per cent in June, but the measure the Reserve Bank watches more closely remained stuck at 3.6 per cent, well above its 2 to 3 per cent target.

At the same time, new dwelling costs are rising faster, rents continue to climb, and electricity prices are still more than 22 per cent higher than a year ago.

For property investors, the rental figures tell an equally important story. Rental vacancies remain extremely tight across most capital cities, Sydney unit rents have surged almost 13 per cent over the year, and Darwin unit rents are up more than 18 per cent.

Yet the sales market is sending mixed signals. Auction clearance rates remain subdued across most capitals, with Sydney falling to just over 55 per cent, while Melbourne was the standout, improving to more than 62 per cent.

So, are we seeing the early stages of a rental market becoming even tighter while property prices remain under pressure? And could persistent inflation force the RBA to make life more difficult for borrowers before conditions improve?

That's what we discuss in this week's episode of Property Insiders, with Dr Andrew Wilson.

Rents are still rising despite the winter slowdown

Home rents continued to rise for both houses and units over July, although the typically quieter mid-winter period did contribute to higher vacancy rates in some capitals.

Watch this week's Property Insider chat as Dr. Andrew Wilson discusses his latest My Housing Market Rental Report.

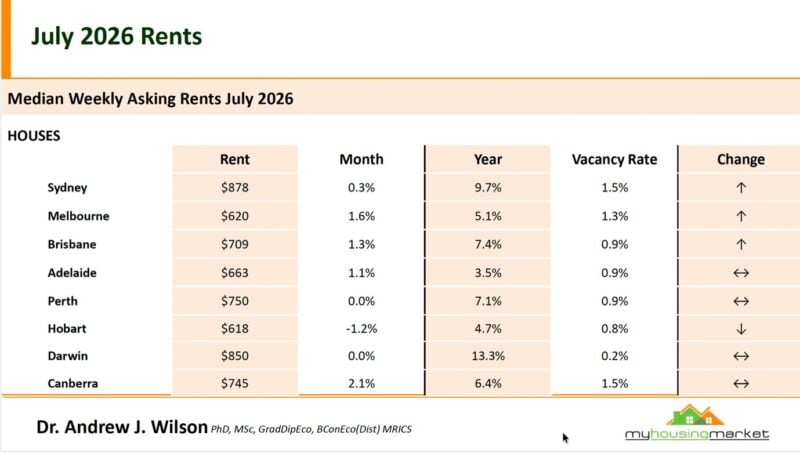

Canberra was the strongest performer for house rents this month, up 2.6%, followed by Melbourne at 1.7%, Brisbane at 1.3%, Adelaide at 1.1% and Sydney at a more modest 0.3%. Perth and Darwin held steady over the month, while Hobart was the only capital to see house rents fall, down 1.2%.

Sydney remains the most expensive capital for house rents by a wide margin, now at $878 a week, while Hobart is the most affordable at $618.

Most capitals continue to post solid to strong annual house rent growth, and Darwin is leading the pack, up 13.3% over the year, with Sydney close behind at 9.7%.

The pressure on unit rents is even more pronounced

What's this week's Property Insider chat as Dr Andrew Wilson explains how the unit rental market produced some particularly strong results during July.

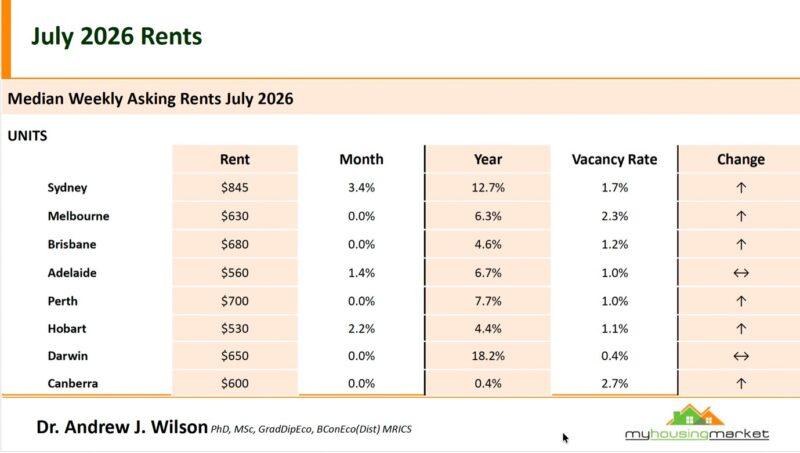

Sydney unit asking rents jumped by 3.4% in a single month and have now increased by 12.7% over the year.

The median weekly asking rent for a Sydney unit has reached $845, only $33 below the median asking rent for a house.

That narrow gap tells us something important about affordability.

Many tenants who would once have rented a house are competing for apartments because they can no longer afford the higher weekly cost of a detached dwelling. At the same time, strong population growth and the return of overseas students are placing additional pressure on unit markets in inner and middle-ring suburbs.

Hobart unit rents increased by 2.2% during July, while Adelaide rose by 1.4%. Unit rents were steady over the month in Melbourne, Brisbane, Perth, Darwin and Canberra.

Darwin recorded the strongest annual unit rental growth at 18.2%, followed by Sydney at 12.7%, Perth at 7.7% and Adelaide at 6.7%.

Melbourne unit asking rents were unchanged during July at $630 a week but were still 6.3% higher than a year ago.

Interestingly, the median asking rent for a Melbourne unit is now slightly higher than the median asking rent for a house. This partly reflects the concentration of apartment demand in well-located inner suburbs and the very different types of properties included in each median.

It is another reminder that citywide averages can conceal substantial differences between individual locations and properties.

What strikes me most about these figures is just how broad based the rental growth has been.

This isn't one or two capitals doing the heavy lifting. It's happening almost everywhere, and that tells you something important about the underlying supply and demand imbalance that continues to define our rental markets.

Government policy is discouraging the rental supply we need

Dr Wilson makes an important point in this week's episode that I think every investor needs to hear. Australia’s rental crisis is often discussed as though rents can be controlled independently of housing supply.

In reality, rents ultimately reflect the balance between the number of households looking for accommodation and the number of properties available.

The public sector will never be able to provide enough rental accommodation to meet the needs of Australia’s growing population. Most tenants rent their homes from private investors, many of whom own only one investment property.

- Also read:National Weekly Auction Report – August 8th 2026 | Home Auction Markets Rising

- Also read:National Property Listings Surge to Highest Level in Over a Year | Latest SQM Listing Data

- Also read:Rents keep climbing while inflation and auctions send mixed signals | Property Insiders

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:July Home Prices Sharply Down as Winter Freeze Bites | Latest Property Market Stats

Yet these investors are facing higher interest costs, rising insurance premiums, increased maintenance expenses, additional taxes and increasingly restrictive rental legislation.

When governments make property investment less attractive, fewer investors enter the market and some existing owners eventually sell. The property is often purchased by an owner-occupier, meaning one less home is available to rent.

That may help one household become a homeowner, but it does little for the tenants still competing for the remaining rental properties.

If policymakers genuinely want to ease rental pressure, they must encourage more rental supply while improving the viability of constructing new homes.

Inflation is easing on the surface, but the number that matters isn't moving

What's this week's Property Insider chat, as Dr. Andrew Wilson explains that headline inflation fell again in June, down from 4.0% to 3.8% annually, and on the surface that looks like good news.

But the Reserve Bank doesn't set interest rates based on the headline number. It watches underlying inflation, and that measure was steady at 3.6%, the highest it's been since July 2024, and still sitting well outside the RBA's target range of 2 to 3%.

A big part of the problem is electricity. Annual electricity price growth jumped from 21.1% in May to 22.4% in June, as government subsidies that had been keeping a lid on power bills continue to ease.

Fuel prices did move in the other direction, swinging from a 7.7% annual rise to a 7.3% fall, which took some heat out of the headline figure. But rental growth held steady at 3.6%, and new dwelling prices rose again, up from 5.6% to 5.8%.

This combination matters a great deal for property investors. When underlying inflation stays stubbornly above target while headline inflation drifts lower, it becomes harder for the Reserve Bank to justify further rate cuts, and it keeps the door open to another rise if the numbers don't improve.

I'd encourage you to watch this week's episode, where Dr Wilson walks through exactly why electricity subsidies have become such a significant swing factor in our inflation numbers, and what that could mean for the RBA's next move.

Of course, another rate rise is far from certain because there are also signs that households are under significant pressure. Underemployment has increased, discretionary spending remains subdued and many mortgage holders are already devoting a much larger proportion of their income to repayments.

However, borrowers should remain prepared for interest rates to stay higher for longer, and the possibility of another increase cannot be dismissed.

Auction markets open August with a split result

Capital city auction markets began August with mixed results. Most capitals continued to report subdued clearance rates, with the notable exception of Melbourne, while listings fell over the week in every capital except Canberra.

The national weekend auction market reported an average clearance rate of 48.4% over the past week, which was slightly higher than the 47.9% reported over the previous week and again well below the 71.0% reported over the same week last year.

Auction markets have commenced August with continuing subdued results – except perhaps Melbourne, with no sign yet of the usual end of winter seasonal revival.

What this means for property investors

The current market presents investors with an unusual combination of conditions.

Property prices and auction results are under pressure in many locations, borrowing capacity remains constrained, and another interest rate rise is possible.

Meanwhile, rents continue to increase because population growth and household formation are outpacing the delivery of new housing.

This divergence between the sales and rental markets won’t continue indefinitely.

Periods of softer buyer sentiment can give strategic investors more time to conduct due diligence, negotiate favourable terms and purchase quality assets without the intense competition seen during boom conditions.

However, rising rents alone don’t make a property investment grade.

Investors still need to concentrate on locations with strong and diverse employment, rising household incomes, limited future supply and a deep pool of affluent owner-occupiers.

They should also maintain substantial financial buffers and allow for interest rates to remain elevated for some time.

In my view, the biggest long-term risk facing well-prepared investors is losing perspective because of short-term uncertainty.

Australia will continue to add people, households will continue to need somewhere to live and the construction industry will struggle to provide enough homes at an affordable price.

That provides a strong foundation for carefully selected, well-located residential property, even though the next stage of the market cycle is likely to remain uneven.