Key takeaways

By the end of 2025, Domain expects house prices will have risen by 9% across the combined capitals.

Every city saw strong gains, led by Sydney (up 9% or $150,000), Brisbane (up 9% or $98,000), Adelaide (up 9% or $92,000), Perth (up 9% or $82,000) and Melbourne (up 7% or $70,000).

Units surged in the more ‘affordable’ capitals: Across the combined capitals, units will reach 7% growth by the end of 2025.

Unit markets in affordability-constrained cities outperformed houses. Units in Adelaide grew by 16% ($90,000), Brisbane 14% ($90,000), and Perth 12% ($61,000), as buyer demand concentrated on the search for value.

The RBA’s February, May and August cuts reignited buyer confidence, driving enquiries higher, and pushing clearance rates to multi-year highs. But the confidence boost fuelled price growth.

Australia’s median house price recorded its 11th straight quarterly rise as tight supply and strong population growth kept pressure on the market.

Investor lending surged more than 20% in the first two quarters of 2025, lifting their share of new housing finance above 40%, the highest in almost ten years.

This flood of investor activity intensified competition at the lower end of the market, where first-home buyers typically search. With the Government’s Home Deposit Guarantee now in play, this competitive environment is expected to roll into early 2026.

Rapid price growth in Brisbane, Adelaide, and Perth reshaped the affordability map. Adelaide joined the million-dollar club, Brisbane became the nation's second-most-expensive capital, and Perth is on track to hit the million-dollar mark by Christmas.

With prices climbing, buyers sought more flexible and affordable options.

Unit markets continued to soar, while Domain search data recorded big jumps in search terms like “dual,” “granny flat,” “duplex,” and “dual living” as households looked for multigenerational solutions or secondary income opportunities.

After two challenging years of high borrowing costs and fragile confidence, 2025 opened with a long-awaited turning point: the first interest rate cut in more than four years.

It was the moment homebuyers, investors, and even weary mortgage holders hoped would turn the tide.

And in many ways, it did, because it was more than a financial adjustment; it was a psychological shift.

The property market gained momentum, confidence rebounded, and buyers who had been sitting on the sidelines suddenly saw a path forward.

But as the Domain 2025 End-of-Year Wrap reveals, while the cash rate moved lower, affordability didn’t follow suit.

Instead, the relief of cheaper borrowing only reignited demand; and that pushed prices even higher, again creating affordability issues .

Cash rate reduction impacts on boosting power, compared to property price growth this year

| Cash rate | 2025 forecast

Annual price growth (% and $ change) |

|||

| Cumulative rate reduction | Additional borrowing power | City | Houses | Units |

| -25bp | 2.3% ($23,700) | Sydney | 9% ($150,000) | 5% ($39,000) |

| -50bp | 4.6% ($48,200) | Melbourne | 7% ($70,000) | 5% ($29,000) |

| -75bp | 7.1% ($73,800) | Brisbane | 9% ($98,000) | 14% ($90,000) |

| Adelaide | 9% ($92,000) | 16% ($90,000) | ||

| Perth | 9% ($82,000) | 12% ($61,000) | ||

| Canberra | 4% ($48,000) | -1% (-$9,000) | ||

| Combined capitals | 9% ($99,000) | 7% ($47,000) | ||

| Borrowing power is estimated for a hypothetical dual-income household earning a combined pre-tax income of $200,000 annually, assuming minimum living expenses. The 2025 price change reflects actual growth from January to September, combined with the forecast for the final quarter of the year. | ||||

As Dr Nicola Powell, Domain’s Chief of Research and Economics, observed:

“Rate cuts boosted confidence and activity, but they didn’t resolve the structural imbalance between demand and supply.

If anything, they intensified competition in a market already starved of new homes.”

A long-awaited turning point for rates

Domain reports that 2025 began with optimism, as after years of rising mortgage repayments and subdued sentiment, the Reserve Bank finally delivered cuts in February, May, and August, which were small but psychologically powerful moves that reset the tone of the market.

Each cut nudged borrowing costs down and confidence up.

Buyer enquiry levels rose, auction clearance rates improved, and the early months of 2025 were marked by a noticeable shift in sentiment.

The Domain 2025 End-of-Year Wrap calls this period a “turning point, not a resolution.”

The shock of the rate-hike cycle had passed, but the deeper affordability challenge remained.

Affordability: a stubborn, structural challenge

Despite improved confidence, affordability barely budged in 2025. Rate cuts reduced monthly repayments slightly, but the benefit was largely absorbed by surging home prices.

According to Domain’s analysis, Australia just recorded its 11th consecutive quarter of house price growth, the longest uninterrupted run since 2012–15.

Unit prices rose at more than twice the pace of the previous year, while combined capital city house prices are now roughly 50% higher than in 2019.

It’s not hard to see why.

Population growth continues to far outpace housing supply, with roughly 3.2 additional people for every new home built between 2023 and 2025.

That imbalance has created a powerful upward force on both property prices and rents — one that even lower interest rates can’t offset.

As Dr Powell put it:

“The fundamental issue is supply. Until we address how few homes are being built relative to demand, affordability will continue to deteriorate, even in a lower-rate environment.”

Faced with these realities, Australians adapted rather than withdrew and Domain’s buyer search data shows a surge in terms like “dual living,” “granny flat,” “duplex,” and “dual occupancy.”

This reflects a shift toward creative affordability solutions; buyers seeking multigenerational setups, income-generating options, or smaller dwellings that offer a toehold in the market.

Investors roared back

Note: One of the standout trends of 2025 was the resurgence of investor activity.

Once the February rate cut hit, investor lending accelerated dramatically, rising more than 20% in just two quarters, and accounting for just over 40% of new housing finance, the highest share in nearly a decade.

However, as the Domain report highlights, most of that capital flowed into existing properties rather than new builds.

Over 80% of investor loans were used to purchase established homes, intensifying competition for first-home buyers and doing little to expand supply.

This has been a long-running structural issue in the Australian property system; government policy continues to favour investment in existing housing stock through tax incentives and depreciation benefits, while new construction remains mired in cost pressures, planning delays, and labour shortages.

As a result, investor confidence returned faster than affordability did.

A new market hierarchy emerges

The combination of cheaper money and tight supply reshaped Australia’s market rankings.

Adelaide joined the million-dollar club, alongside Sydney, Melbourne, Brisbane, and Canberra.

Perth is expected to hit that milestone by the end of the year after a remarkable multi-year run.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

Brisbane leapfrogged Melbourne to become Australia’s second-most expensive capital city for the first time on record, a symbolic moment that reflects long-term demographic and economic shifts.

Meanwhile, the traditional “tier-one vs tier-two” distinction is breaking down.

As Dr Powell explains:

“We’re seeing a fundamental realignment of value. Cities once considered affordable alternatives like Perth, Adelaide, and Brisbane, are now established high-demand markets in their own right.”

Domain’s data illustrates this clearly. By late 2025, combined capital city house prices were up 9%, with unit prices rising 7%.

In some cities, such as Adelaide and Brisbane, unit prices jumped as much as 14–16%, the strongest growth rates in the nation.

But here’s the paradox: lower rates made borrowing easier, yet rising prices absorbed nearly all the benefit.

Domain calculated that a 75-basis-point cumulative cut increased borrowing power by around 7.1%, but most of that extra capacity was quickly priced into the market through higher values.

Australians are adapting, not retreating

One of the most revealing insights from the Domain's report is how Australians are adapting their aspirations.

Rather than giving up on home ownership, buyers are reshaping what it looks like, opting for smaller homes, new locations, or dual-purpose spaces that balance affordability and lifestyle.

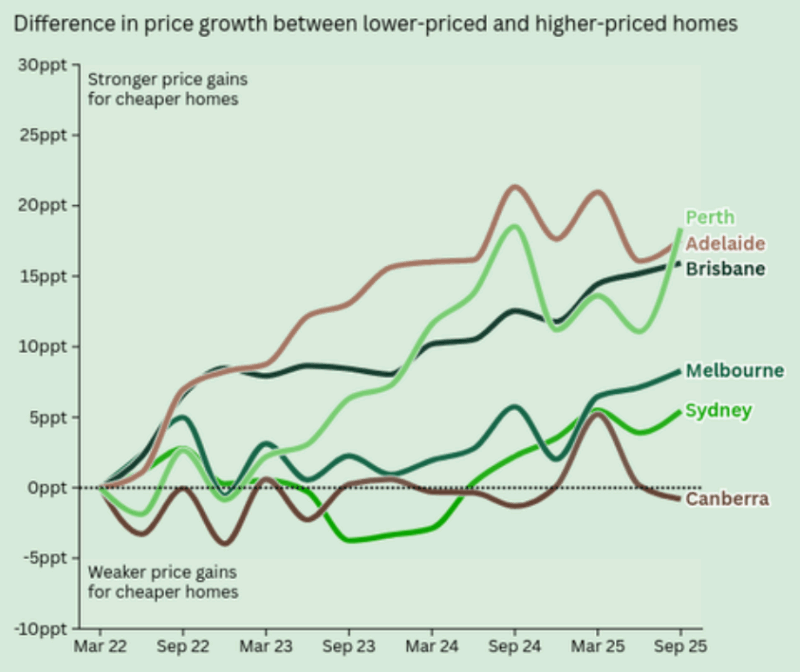

This trend has been especially strong in the lower price brackets, where homes have consistently outperformed premium properties since 2022.

In markets like Perth, Brisbane, and Adelaide, lower-priced housing has become the fastest-growing segment, driven by population growth, limited supply, and constrained borrowing power.

It’s a reminder that while the market evolves, Australians’ determination to own property remains unshakable. They’re just finding new ways to do it.

A late-year shift, but the momentum held

By the final quarter of 2025, the property market faced another twist according to the Domain report.

Inflation, which had been easing for much of the year, unexpectedly ticked up again. That forced the RBA to pause further cuts, quashing hopes of another reduction before year-end.

Yet, the market didn’t stall.

Momentum held firm, supported by policy changes like the expanded Australian Government 5% Deposit Scheme, which now offers unlimited places and higher price caps.

This prompted more first-home buyers to enter the market and, interestingly, encouraged many investors and upgraders to act quickly before new demand intensified competition.

Dr Powell summarised it well:

“The shock of rising rates has passed, but the challenge of rebuilding affordability remains. Supply continues to be the missing piece of the puzzle.”

Looking ahead: the affordability conundrum continues

The Domain 2025 End-of-Year Wrap can be summarised as follows: 2025 was a year of renewed optimism, but not of resolution.

The property market proved its resilience, again, but affordability remains the great Australian paradox.

Interest rates may have turned, but without a structural uplift in housing supply, the affordability gap is likely to widen further in 2026.

Population growth, investor confidence, and a deep-seated cultural attachment to property ownership are all combining to sustain demand, even in the face of high prices.

For seasoned investors, this highlights the enduring fundamentals that make real estate a cornerstone of long-term wealth creation.

But for policymakers, it’s a warning bell; rate cuts alone can’t fix affordability.

As I’ve said many times before, property prices are a reflection of human behaviour, not just interest rates.

And in 2025, Australians showed once again that when confidence returns, the property market moves fast, even if affordability doesn’t.

And this trend will continue into 2026.