Key takeaways

Australia’s housing shortage remains the biggest driver of property values, with population growth and changing household patterns continuing to outpace new housing supply.

Property markets are becoming increasingly fragmented, meaning broad city-level predictions matter less than choosing the right suburb, property type, and location.

Tax changes and higher interest rates may slow growth, but they are unlikely to derail quality investment-grade properties in established suburbs.

The strongest long-term opportunities are still in scarce, well-located assets with strong owner-occupier appeal rather than new developments driven mainly by tax incentives.

Successful investors in 2026 will be those who stay strategic, manage risk carefully, and focus on long-term compounding rather than reacting emotionally to headlines or market noise.

There is more conflicting information about property right now than at almost any point I can remember.

Turn on the news and you will find someone warning that prices are about to fall. Scroll a little further and you will find someone else forecasting another year of growth.

Somewhere in the middle of all that noise is what is actually going on, and that is what I want to cut through today.

We have had interest rate rises that surprised many forecasters, a Federal Budget that rewrote the rules for investors, geopolitical uncertainty that has rattled confidence, and a cost-of-living squeeze that has made many Australians feel as if the economy is working against them.

Yet underneath all that noise, the structural case for quality Australian residential property remains very strong.

The foundation of the market has not moved

The single most important thing to understand about the Australian property market in 2026 is that the supply-demand imbalance has not been solved.

Population growth has continued to outpace the construction pipeline, and even if migration moderates from recent peaks, Australia still has to deal with the backlog already created.

At the same time, household formation is changing, with more single-person households, blended families and older Australians staying in place. So we need more dwellings, but also the right dwellings in the right locations.

Builders are still constrained by labour shortages, materials costs, finance, land availability and planning delays, so approvals and commencements remain well short of what is needed.

That is why I see the housing shortage as a structural condition rather than a temporary inconvenience.

It acts as a support under prices and rents in well-located markets, even when interest rates and household budgets are under pressure.

Prices are flatlining, but the market is uneven

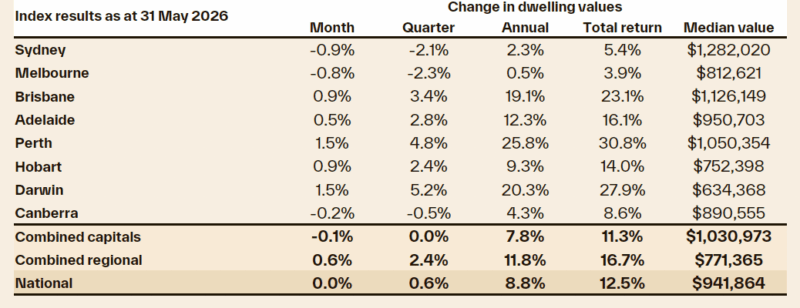

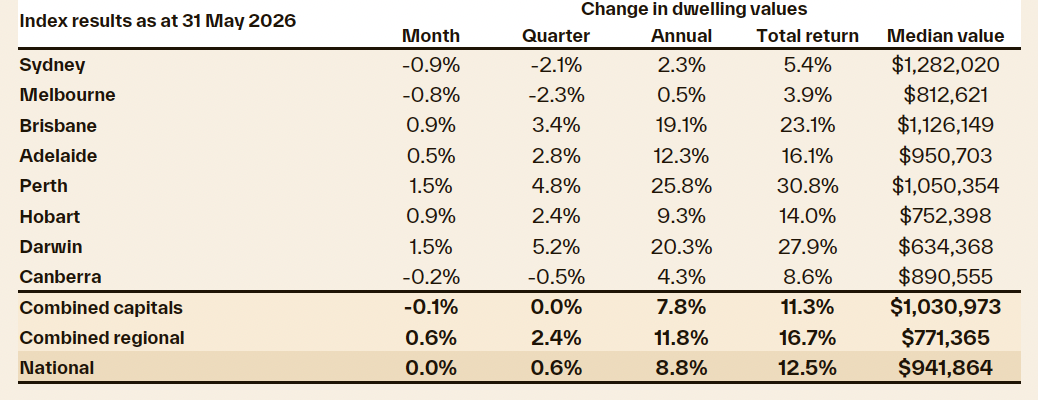

Over the last month, Cotality reported that "overall" property values flatlined around Australia, but values are still rising in many parts of Australia, although the pace has slowed.

Sustainable markets are built on incomes, confidence, credit, scarcity and owner-occupier demand.

Some capital city markets will continue to record growth over the rest of the year, while others will see values decline.

Melbourne and Sydney housing markets are likely to remain subdued, but Melbourne remains particularly interesting to me.

It was the laggard of the last cycle, but its lower relative price base, deep employment market, education sector, population growth and cultural appeal are likely to attract buyers back.

The fundamentals were never really the issue. Melbourne has many of the ingredients long-term investors should look for, especially in established inner and middle-ring suburbs where land is scarce, and owner-occupiers want to live.

Sydney still has the deepest pool of high-income buyers in the country, but affordability bites harder there.

Brisbane, Perth and Adelaide have been strong performers, but investors should be careful about assuming yesterday’s growth will repeat tomorrow.

This is where investors get caught. They look at city-level headlines and assume the opportunity is broad, while in reality, every capital city contains multiple markets driven by different buyer groups, incomes, stock levels and lifestyle preferences.

The Budget changes are real, but they do not change the fundamental case

The 2026 Federal Budget introduced significant tax changes, especially to negative gearing and capital gains tax, meaning investors entering the market now need strategic advice more than ever.

My broader concern is that the Budget still misdiagnoses the housing crisis.

Australia’s affordability problem is mainly a supply problem. Tax settings influence behaviour, but reducing the financial appeal of investing in established properties does not build a single extra home.

The risk is that these changes reduce the pool of private rental accommodation just when tenants need more choice.

There may also be a lock-in effect, with some existing investors holding assets for longer.

Investors should also be careful about one conclusion that is already becoming popular. Just because the rules favour new dwellings does not mean you should rush into new apartments or outer-suburban estates.

A tax benefit can improve the after-tax return of a good asset, but it rarely rescues a poor one. Established, scarce, well-located assets still have what many new properties lack: proven demand and long-term capital growth.

Interest rates matter, but they are not the whole story

The RBA has been more aggressive in 2026 than many people expected, with inflation proving stickier and global uncertainty adding another layer of complexity.

Yes, rates matter. They affect borrowing capacity, sentiment, household cash flow and the number of buyers who can compete at auction.

But in my experience, rates are almost never the defining factor people assume they are.

Markets move on surprises, not on widely anticipated events. A gradual tightening cycle is very different from the shock rate hikes of 2022, and the property market has already absorbed much of the impact of the current environment.

More importantly, the cost of waiting can be very expensive. If a quality property grows by even 5% to 7% over a year, waiting can mean paying tens of thousands of dollars more for the same asset.

That does not mean investors should ignore borrowing risk. Buffers matter. Cash flow matters. Loan structure matters. A realistic view of holding costs matters.

But waiting for perfect certainty is usually fear dressed up as caution.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State July 28th 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:53 years of valid reasons not to invest

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

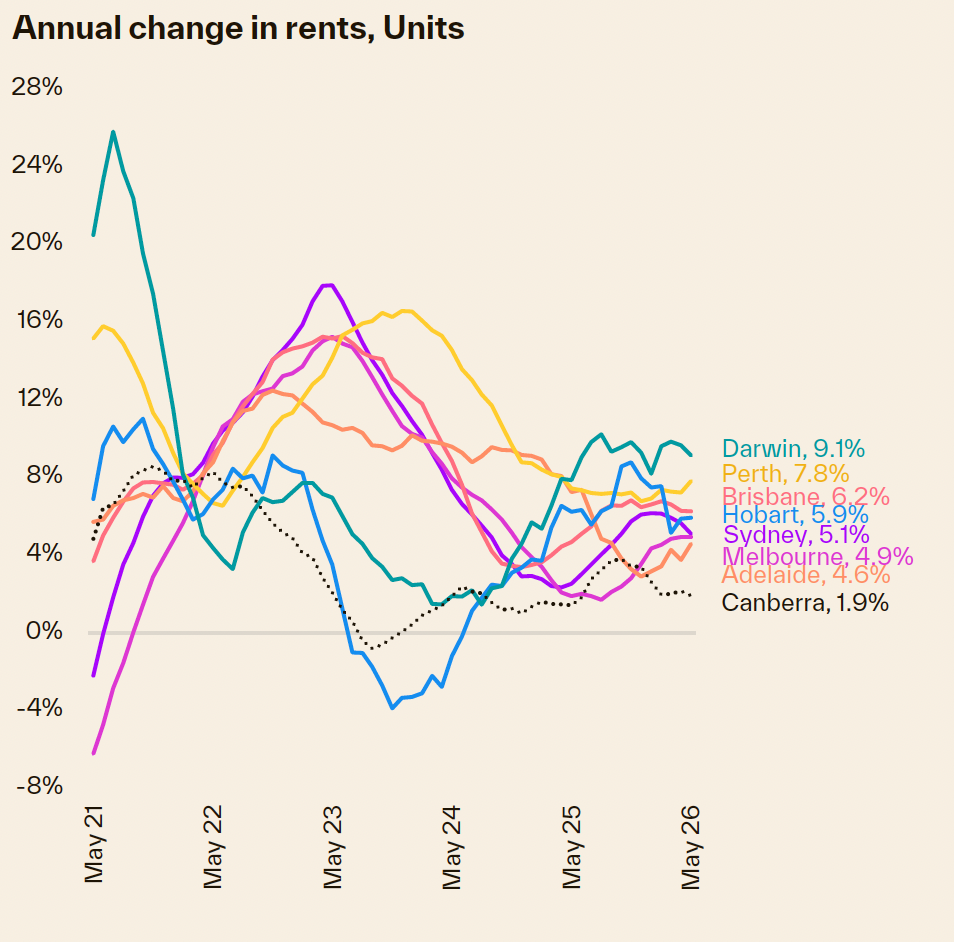

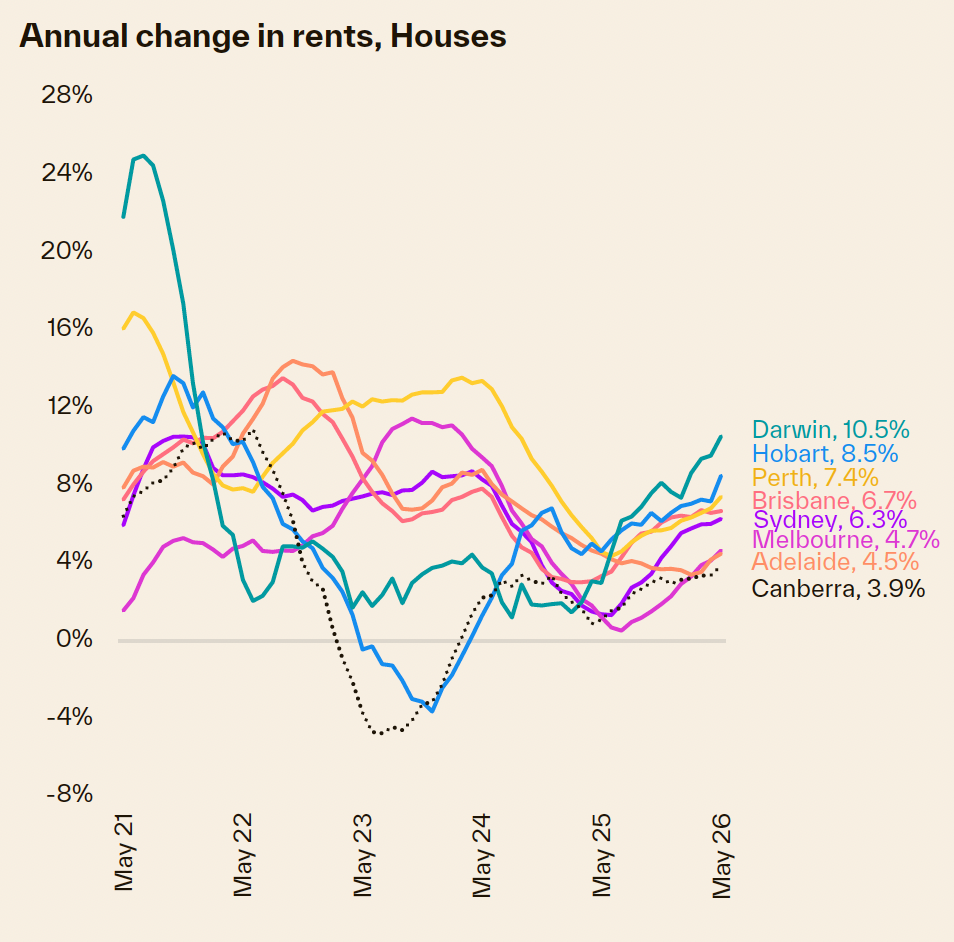

The rental market is sending a clear signal

The rental market is one of the clearest signs that Australia’s housing shortage is real.

Vacancy rates remain tight in many locations, rents have risen strongly, and many tenants are paying a record share of their income just to secure accommodation.

Rental growth will support some investors’ cash flows, but not all properties equally. Tenants want transport, jobs, schools, lifestyle amenities, security and a floor plan that fits the way they live.

In a tight market, almost anything may rent, but over the long term, better properties attract better tenants, lower vacancy risk and stronger capital growth.

This is why I keep coming back to investment-grade assets with multiple layers of demand.

The market is fragmenting

One of the most important shifts I have been writing about is the fragmentation of the Australian property market.

Talking about our housing markets as one unified market is genuinely misleading.

The gap between capital city house and unit values widened after COVID, although affordability constraints are now pushing more buyers toward townhouses, villa units and well-located apartments.

That makes the right medium-density accommodation more attractive as buyers trade land size for liveability.

I have always favoured boutique apartments, villa units and townhouses in established suburbs where the land component, scarcity and owner-occupier appeal are stronger.

My consistent position has been to focus on inner and middle-ring gentrifying suburbs of Sydney, Melbourne and Brisbane, particularly locations with proven demand drivers, walkability, established infrastructure and scarcity that cannot be solved by releasing another paddock on the fringe.

I remain wary of regional markets, cheap properties on the outskirts, and data-driven hotspot narratives that encourage investors to chase yesterday’s growth. Boring and proven still beats exciting and speculative.

What actually determines whether you win

After all the analysis of rates, policy, supply data and forecasts, I keep coming back to one point: the investor matters more than the investment.

Many people who struggled through the past few years were undone by emotional decisions. Some panicked when rates rose, some sold quality assets too early, some waited for certainty, and others chased markets after they had already moved.

The framework that works is process over prediction, quality over quantity, and time in the market over timing the market.

None of that has been undermined by Budget changes, the rate cycle or geopolitical noise.

The investors who thrive from here will act deliberately, structure their portfolios carefully, buy assets with genuine scarcity, protect their cash flow, manage risk, and hold long enough for compounding to do the heavy lifting.

So, what is really ahead for property in 2026?

I expect 2026 to be a year of slow and uneven growth, tight rental markets, more policy noise, and greater separation between good assets and average ones.

I do not expect a broad-based collapse in quality established property, because the supply-demand imbalance is too strong and the buyer pool in many desirable suburbs remains too deep.

I do expect some investors to be shaken out by higher holding costs, tax changes and fatigue. Others will make poor choices by chasing tax-favoured new stock without understanding the long-term fundamentals.

That will create opportunity for strategic investors.

CBA have recently updated their forecasts. Dwelling price growth is expected to slow to 3% over the year to December 2026, a step down from their previous estimate for growth to be 5%. Growth over the year to December 2027 remains unchanged at 3%.

The slowdown over the coming year primarily reflects the effect of higher mortgage rates, with the three cash rate hikes this year to date adding to borrowing costs and cooling buyer sentiment. These three hikes have subtracted 1.5 percentage points from the banks’ 2026 price growth forecasts.

The restriction of negative gearing for established housing and the replacement of the CGT discount with indexation and a 30% minimum tax rate will also weigh on prices according to the CBA. They estimate this policy change will subtract 0.6 percentage points from annual price growth by the end of this year and just under 1 percentage point from growth over 2027.

That's an overall figure, and some markets will perform better than others. But it's really not moving the needle, is it?

As I see it, the best opportunities are unlikely to be found in the headlines. They will be found in established suburbs where incomes are rising, infrastructure is already in place, land is scarce, and aspirational buyers want to live.

The right move in 2026 is to be informed, selective and prepared. Stress-test your finances, get strategic advice before you buy, understand the new tax rules, avoid speculative locations, and focus on assets with long-term owner-occupier appeal.

Property will keep rewarding patience, perspective and discipline. I do not see 2026 changing that.

If you're concerned about how the tax changes or high-interest-rate environment could affect your property portfolio, speaking to one of our Metropole Wealth Strategists is a good starting point.

At Metropole, we're much more than another buyer's agency. We help our clients grow, protect, and pass on their wealth through strategic property and wealth advice.

Why not book a complimentary chat with one of our wealth strategists by clicking here? To us, property is the vehicle, but strategy is the driver.