Key takeaways

Compounding is the process of earning returns on both your original investment and past returns.

Over time, this creates a powerful “snowball effect,” where small contributions can grow into significant wealth.

Many investors get distracted by short-term market noise but overlook the power of long-term compounding—especially younger Australians, who have the most time to benefit.

If there is one financial principle every investor should understand, it’s compounding.

Albert Einstein supposedly called it the eighth wonder of the world, and for good reason.

Compounding is your best friend as a property investor and is simply the process of earning returns on both your original investment and the returns you’ve already earned.

Over time, this “snowball effect” can turn small contributions into significant wealth.

While many investors are obsessed with short-term growth, and the media keeps updating us on the day-to-day impact of the economy, interest rates, and politics, many people underestimate the importance of long-term compounding, particularly younger Australians, who are actually best placed to benefit from starting early.

Put simply, compound interest is the concept of earning interest on interest or getting a return on past returns.

Any interest or return earned in one period is added to the original investment, so it all earns a return in the next period.

And so on.

The three key drivers of compounding

Three simple factors determine how powerful compounding will be for you:

- Rate of Return – Higher returns mean faster compounding. Over the long term, growth assets like shares and property tend to deliver higher average returns than cash or bonds.

- Contributions – The more you put in, and the earlier you do it, the greater the snowball becomes. Even a modest upfront contribution can dramatically boost long-term results.

- Time – The longer your money is invested, the more compounding has to work its magic. Time also helps smooth out short-term market volatility.

Compounding in action

While the principle of compounding is important for property investors growing their portfolio, let's look at a simple example of how an investor can get started with small amounts to build up sufficient funds for either a deposit or just as an investment in general.

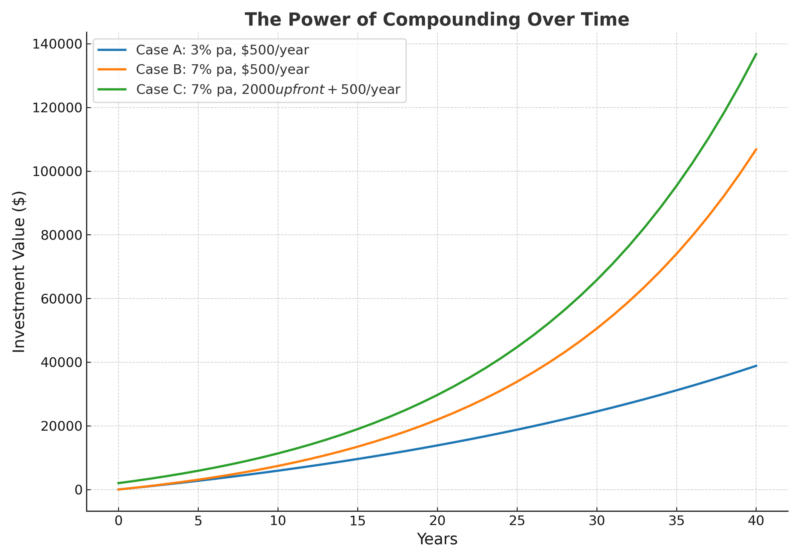

To illustrate the principle of compounding let’s say an investor makes regular contributions of $500 per year:

- Case A: Invests $500 per year at 3% per annum. After 20 years, the portfolio grows to $13,838. After 40 years, it’s worth $38,832.

- Case B: Invests $500 per year at 7% per annum. After 20 years, it grows to $21,933. After 40 years, $106,805.

- Case C: Starts with an upfront $2,000 plus $500 per year at 7% per annum. After 20 years, the portfolio grows to $27,737. After 40 years, $129,267.

Of course, these examples are pretty simple, but I want to illustrate the concept, and the chart below shows how each case grows over time.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

Notice how the lines begin to diverge more dramatically after about 15–20 years.

That’s the exponential power of compounding: returns building on top of returns.

The power of compounding in property

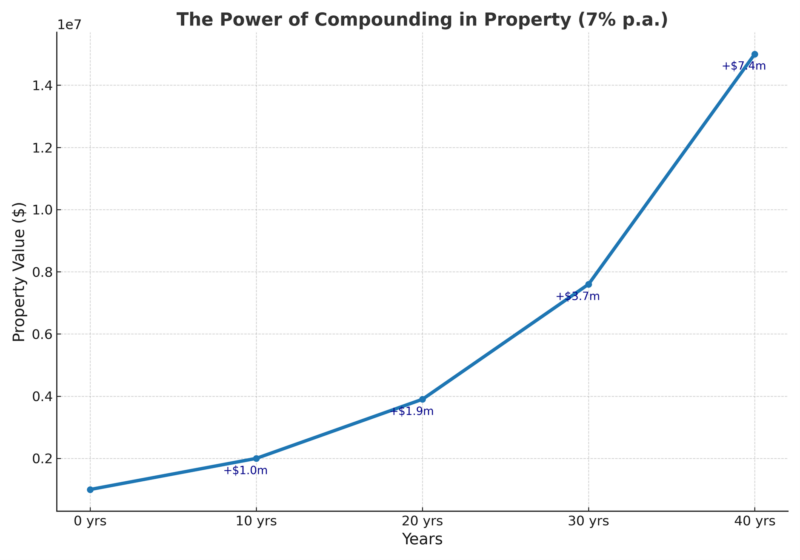

Over the last 40 years, well-located properties in our capital cities have delivered more than 7% per annum capital growth.

If you own an asset that delivers this level of compounding growth, it’s important to understand how that return plays out over time:

- First decade: The property grows from $1 million to $2 million — an increase of $1 million (around $100,000 per year).

- Second decade: It grows from $2 million to $3.9 million — an increase of $1.9 million (around $190,000 per year).

- Third decade: It grows from $3.9 million to $7.6 million — an increase of $3.7 million (around $370,000 per year).

- Fourth decade: It grows from $7.6 million to $15 million — an increase of $7.4 million (around $740,000 per year).

In the fourth decade, the average annual property growth is more than seven times higher than it was in the first decade.

Of course, property markets never move in a straight line - they are cyclical and unpredictable in the short term.

But this simplified example illustrates the extraordinary power of compounding over multiple decades.

Of course, as the value of their assets increase property investors can then refinance their investments, borrowing against their increasing equity and buy more properties - pyramiding the compounding principle.

Implications for property investors

There are clear lessons here for property investors wanting to harness the power of compounding:

- Think long-term – Property is a growth asset. A buy-and-hold strategy over decades allows compounding to work in your favour, while those who invest for the short term or try and flip properties miss out on the magic of compounding and end up paying more tax.

- Start early and add regularly – The sooner you begin your property journey, and the more consistently you add to your portfolio, the greater the compounding effect.

- Stay the course through cycles – Property markets have ups and downs, but understanding that short-term volatility is normal makes it easier to hold on and benefit from long-term growth. In my mind, market downturns are not a “fine” for being involved in property. They are a fee for having invested in property.

- Be selective – Avoid investments that seem too good to be true, and avoid short-term hotspots. Instead focus on quality growth assets with a proven long-term record.

By combining patience, consistency, and smart asset selection, property investors can make compounding one of the most powerful forces driving their wealth.