Make sure to ‘die with zero’ for optimal happiness - that's the idea behind Bill Perkins book - Die with Zero.

In short, Perkins wants to rescue you from over-saving and under-living.

So let's dive into a challenging yet enlightening perspective on retirement, personal finance, and life priorities, inspired by Simon Kuestenmacher's article in The New Daily about this book.

While it's particularly pertinent for the middle and upper classes, but even if you're under financial stress, there's valuable wisdom to be found.

The core argument: spend wisely, live fully

Perkins' fundamental argument is straightforward yet profound: to extract maximum joy and fulfilment from our finances, we shouldn't hoard all our money for retirement or fixate on leaving hefty inheritances.

He says:

Imagine if by the time you died, you did everything you were told to. You worked hard, saved your money, and looked forward to financial freedom when you retired.

The only thing you wasted along the way was . . . your life.

Perkins suggests we should use our wealth to enhance our lives while we're still around.

Money, in essence, is a means to fulfil basic needs, savour life's pleasures, assist others, and craft a legacy.

Perkins advocates for a 'die with zero' approach, implying we should aim to utilize our resources fully, rather than leave an excess untouched at life's end.

Accumulating wealth we never use is akin to missing out on the life experiences that wealth could have unlocked.

Life is for living: embrace the now

We often reminisce about the past - those unforgettable trips, early romances, or joyous family holidays.

These memories, or 'memory dividends' as Kuesentenmacher likes to call them, enrich our lives.

Therefore, prioritizing experiences and investments that bring immediate joy and fulfilment is crucial.

It's about front-loading life's significant experiences.

But caution - this isn't a green light for reckless spending. It's a call for strategic earning and spending, avoiding the pitfall of unused wealth accumulation.

The Australian Housing Market and intergenerational wealth

Here, we connect these ideas to the Australian housing market.

According to Simon Kuestenmacher the concept of the 'bank of mum and dad' becomes highly relevant, aligning with Perkins' views against merely amassing wealth for posthumous inheritance.

He said that the rationale is twofold:

- First, helping your children financially now, when it's most needed, is far more rewarding than post-death bequests.

- Second, early financial assistance, like aiding with home purchases, can significantly reduce their financial burdens.

Kuestenmacher explains:

Your kids need your money now (if you don’t have kids and plan to donate money once you die, the same logic applies) rather than later. Kids need a leg up in the housing market when they are raising a family in their 30s rather than when they moan your loss, are aged around 60, and their kids have moved out already.

- Also read:6 Lessons from Robert Kiyosaki’s Rich Dad Poor Dad to Build Wealth and Financial Independence

- Also read:Retirement might not be as enjoyable as you expect

- Also read:3 Lessons I learned at Wealth Retreat

- Also read:How does my super get taxed?

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

Assuming an interest rate of 5.3 per cent and a loan term of 30 years, a $400,000 mortgage will require your kids to pay a total of $800,000 to the bank. If you can afford to give your kids an early inheritance of say $100,000 they only need a $300,000 mortgage.

The total repayment would only be $600,000. You effectively gave your kids a $200,000 financial advantage by “only” giving them $100,000. That’s a very effective use of money.

Your legacy: a positive financial impact

Leaving a legacy should be about creating positive, lasting impacts, not just material inheritance says Kuestenmacher.

Mismanaged wealth transfer can lead to family conflicts and lasting rifts.

So consider downsizing and simplifying your estate to make the inheritance process smoother and to free up funds for enjoying life.

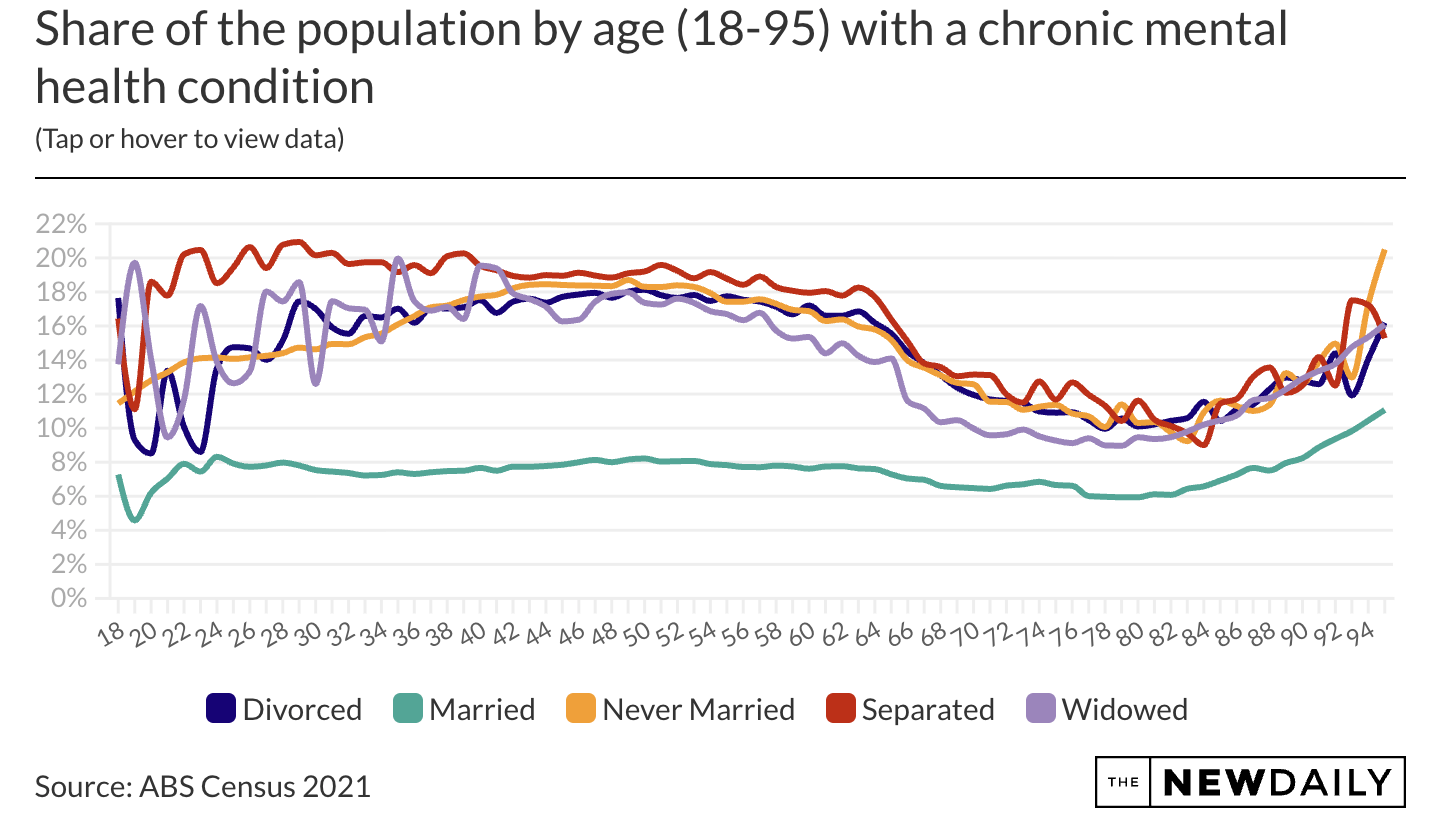

Loneliness in old age: a critical factor

A significant risk for the elderly is loneliness, especially for the surviving partner in a couple.

\

Source: ABS Data Simon Kuestenmacher The New Daily

Kuestenmacher explains:

A huge risk in old age is loneliness.

This is most severe for the last surviving member of a couple. Your partner of many years just died. Obviously that not good for your mental health. You now live alone in the large family home.

If your home is in a car dependent location, loneliness gets even more severe.

You will receive fewer social visits, stay isolated for longer stretches of time, and your mental health slowly deteriorates.

To mitigate this, he suggests considering downsizing to a more manageable living space in your 70s.

This move not only frees up financial resources but also helps in building a supportive social network, crucial for mental and physical well-being in later years.

The bigger picture: society and wealth

While the 'bank of mum and dad' is beneficial on a personal level, it does raise concerns at a societal level.

Kuestenmacher said this highlights the disparity between families with access to such resources and those without.

This leads us to consider broader policy implications, like wealth taxation, to address these inequalities.

Keeping an eye on emerging policy trends, especially from influential individuals in their 30s and 40s, can offer insights into future directions.

In conclusion, Perkins' philosophy of 'Die with Zero' encourages a more balanced, fulfilling approach to wealth and life.

It's not just about accumulation but about strategic, meaningful use of our resources to enrich our lives and those of others, now and in the future.