Key takeaways

With no rate cuts expected from the RBA next year, homeowners shouldn’t hold their breath for relief.

Instead, those with strong equity, particularly 30–40% or more, can use their position to negotiate lower rates or refinance for better deals.

Canstar found that $621 billion worth of home loans are more than three years old, meaning many borrowers are sitting on valuable equity but paying above-market rates.

Refinancing from an average rate of 5.96% to around 5.14% could save roughly $8,000 over two years.

Borrowers should check their equity and current rate now, as competitive deals under 5.25% are still available, and waiting for the RBA could cost thousands.

It’s the end of another year, and while many Australians were hoping for some Christmas cheer from the Reserve Bank, there will was no interest rate relief under the tree this festive season.

The RBA has made it clear that interest rates are staying higher for longer.

But that doesn’t mean homeowners are completely out of options.

In fact, if you’ve built up a decent amount of equity, your bank might just see you as one of their favourite customers.

And that could mean you’re in line for a better deal, if you know how to ask for it.

The “equity advantage” few are talking about

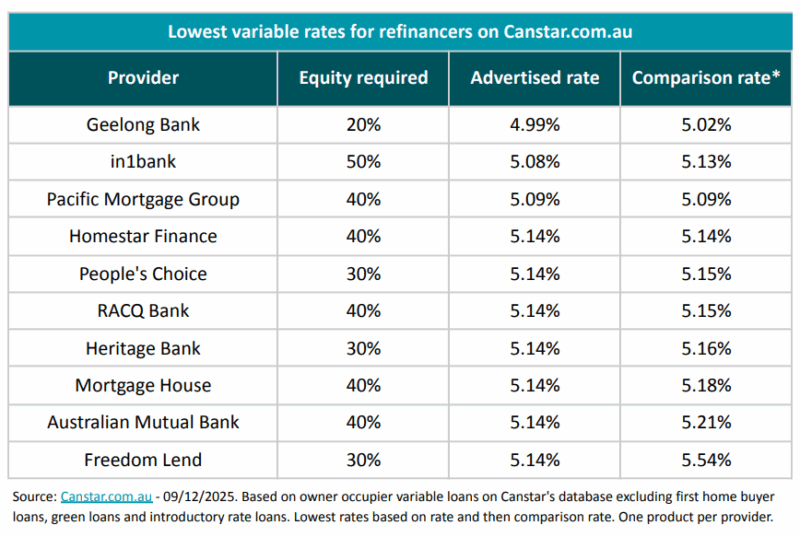

New research from Canstar shows that 62% of lenders reserve their lowest refinancing rates for borrowers who own at least 30% of their property.

Out of the ten lowest variable rates on the market, nine require that level of ownership, and six require 40%.

Tip: The message is clear: the more equity you have, the lower your potential rate.

And many Australians are already in that position without realising it.

The average borrower today owns more than half their property’s value, thanks to years of repayments and capital growth.

In fact, Canstar’s Consumer Pulse Report found borrowers estimate their home equity at around 65%.

That means millions of homeowners could be paying more than they need to simply because they haven’t reviewed their loan in a few years.

Sitting on a goldmine, but paying too much

Canstar’s analysis of APRA data found a whopping $621 billion worth of owner-occupier mortgages are more than three years old.

These borrowers are likely sitting on strong equity, but are probably paying uncompetitive rates unless they’ve been actively negotiating with their lender.

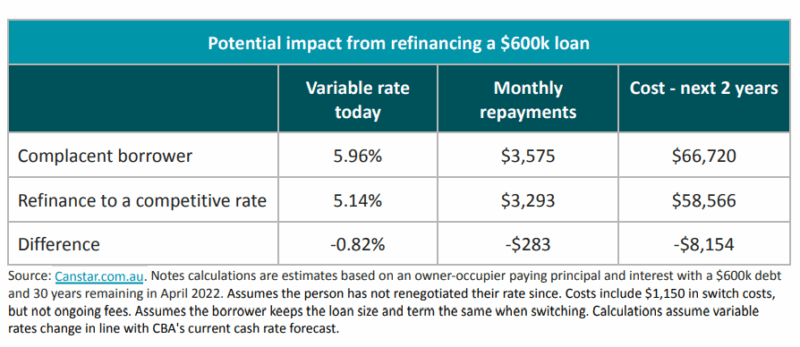

Take someone who took out a $600,000 loan back in April 2022, just before the RBA began hiking rates, and hasn’t renegotiated since.

That borrower is probably paying around 5.96%, compared with the lowest rates on the market of around 5.14%.

If they refinanced, they could save around $8,000 over two years, even after accounting for switching costs.

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

- Also read:National Weekly Auction Report – March 28th 2026 | Auction Clearance Rates Still Fading Over Super Week of Listings

- Also read:RBA raises interest rates again. Here’s what this means for property. | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

That’s not pocket change, that’s potentially next year’s holiday fund, or a buffer in case rates rise again.

How to turn your equity into a lower rate

If you’ve owned your home for several years, chances are your property’s value has climbed while your loan balance has gradually fallen, meaning your equity has quietly grown.

Here’s how to use it:

1. Find out your current equity position.

Subtract your loan balance from your home’s current estimated value, then divide by the value.

If you’ve got 30–40% equity or more, you’re in a strong position.

2. Check your current rate.

According to Canstar, a competitive owner-occupier variable rate is anything under 5.25%, while under 5.14% is considered highly competitive.

3. Shop around or renegotiate.

Don’t be afraid to approach your lender and ask for a better deal, or refinance if they won’t budge.

Many banks are still offering cash-back deals and sharper rates for loyal borrowers who are willing to move.

4. Act before rates move again.

The RBA isn’t expected to surprise borrowers, but if inflation proves sticky, a rate hike in 2026 is possible.

Locking in a better deal now could protect your household budget later.

Final thoughts

The message for homeowners this Christmas is simple: don’t wait for the RBA to deliver relief; create your own.

If you’ve built up solid equity, you’re already holding the key to better rates and lower repayments.

As Canstar's Research Director Sally Tindall says:

“Refinancing to a different lender might not be on the agenda for your summer holiday, but the short-term investment could end up paying for your entire summer holiday next year.”

In other words, you might not get a rate cut for Christmas, but with the right strategy, you could still unwrap a financial gift of your own.