RBA Governor Philip Lowe recently gave his views on the year ahead.

He started by reflecting on what has happened over the last year,none of which was predicted...

A pandemic, the biggest contraction in output in generations, the closure of the borders, a very large physical stimulus, new zero interest rates and quantitative easing.

But his outlook was positive, and he made three significant observations.

like to offer 3 observations on the year we have just been through.

- Australians respond well in a crisis.

- The economic downturn was not as deep as was initially feared and the bounce-back has been earlier and stronger than the RBA were expecting.

- As we start 2021, there is still quite a way to go before we reach our goals of full employment and inflation consistent with the target.

Here's a some other points from his speech to the National Press Club

An earlier and stronger bounce-back

"Despite the pandemic having very significant economic costs, the downturn was not as deep as we had feared and the recovery has started earlier and has been stronger than we were expecting.

Employment growth has been strong, as have retail sales and new house building.

Across many indicators, including GDP, the outcomes have been better than our central forecasts and often better than our upside scenarios as well.

As an illustration, in August our central forecast was that the unemployment rate would end 2020 at close to 10 per cent and still be above 7 per cent at the end of 2022.

In our upside scenario, the unemployment rate was expected to end 2020 a little lower than 10 per cent, but still be around 7 per cent later this year.

Thankfully, the actual outcome for the unemployment rate has been much better than this, with the peak now looking to be behind us and the unemployment rate ending 2020 at 6.6 per cent.

Unemployment did not reach the levels initially forecast because of three factors:

- Success in containing the virus

- Very significant physical policy support

- Australians adapted and innovated - For example online spending surge 70% over the past year.

Still quite a way to go

"... despite the positive economic news over recent months, we still have quite a way to go.

There is still very substantial spare capacity in the Australian economy.

The unemployment rate is higher today than it has been for almost 2 decades and many people can't get the hours of work they want.

And in terms of output, we remain well behind where we thought we would be when I spoke here in February last year (Graph 4).

When the National Accounts are published for the December quarter, they are likely to show that the level of GDP is 4 per cent lower than where we thought it would be a year ago. This is a big gap.

"....Given the spare capacity that currently exists, these low rates of inflation and wage increases are likely to be with us for some time."

The year ahead

In my view, we can draw some comfort from the year just passed.

Our ability to pull together and the earlier-than-expected bounce-back are both positive developments and provide a basis for confidence about the future. Yet even so, the path ahead is likely to be bumpy and uneven and it will be some time before we are back to full employment and have inflation back to the target.

As was the case in 2020, much depends upon the path of the pandemic.

The development of vaccines in record time is clearly good news.

It has reduced one of the big uncertainties and could provide the foundation for a vigorous and sustainable recovery in the global economy.

- Also read:Latest property price forecasts for 2024 revealed. What’s ahead in our housing markets in the next year or two?

- Also read:This week’s Australian Property Market Update – Latest Data, State by State April 23rd 2024

- Also read:Melbourne property market forecast for 2024

- Also read:Brisbane’s property market forecast for 2024

- Also read:Sydney property market forecast for 2024

But this outcome is not assured – the global rollout of the vaccines faces challenges and there are a range of other uncertainties about the global economy, including trade tensions.

We hope for the best here, but we also need to be prepared for further setbacks in what remains a highly uncertain world.

....Our central scenario is for the upswing in the Australian economy to continue, with above-trend growth over the next couple of years.

GDP is expected to increase by 3½ per cent over both this year and 2022.

Given the recovery we have seen so far, we are expecting the level of GDP to return to its end-2019 level by the middle of this year, which is 6 to 12 months earlier than we previously expected.

In the labour market, we are expecting the rate of unemployment to continue to decline. In the central scenario, it is expected to reach 6 per cent by the end of this year and around 5¼ per cent by mid 2023

"...inflation in underlying terms is also forecast to stay below 2 per cent over the next couple of years: the central forecast for 2021 is 1¼ per cent and for 2022 it is 1½ per cent.

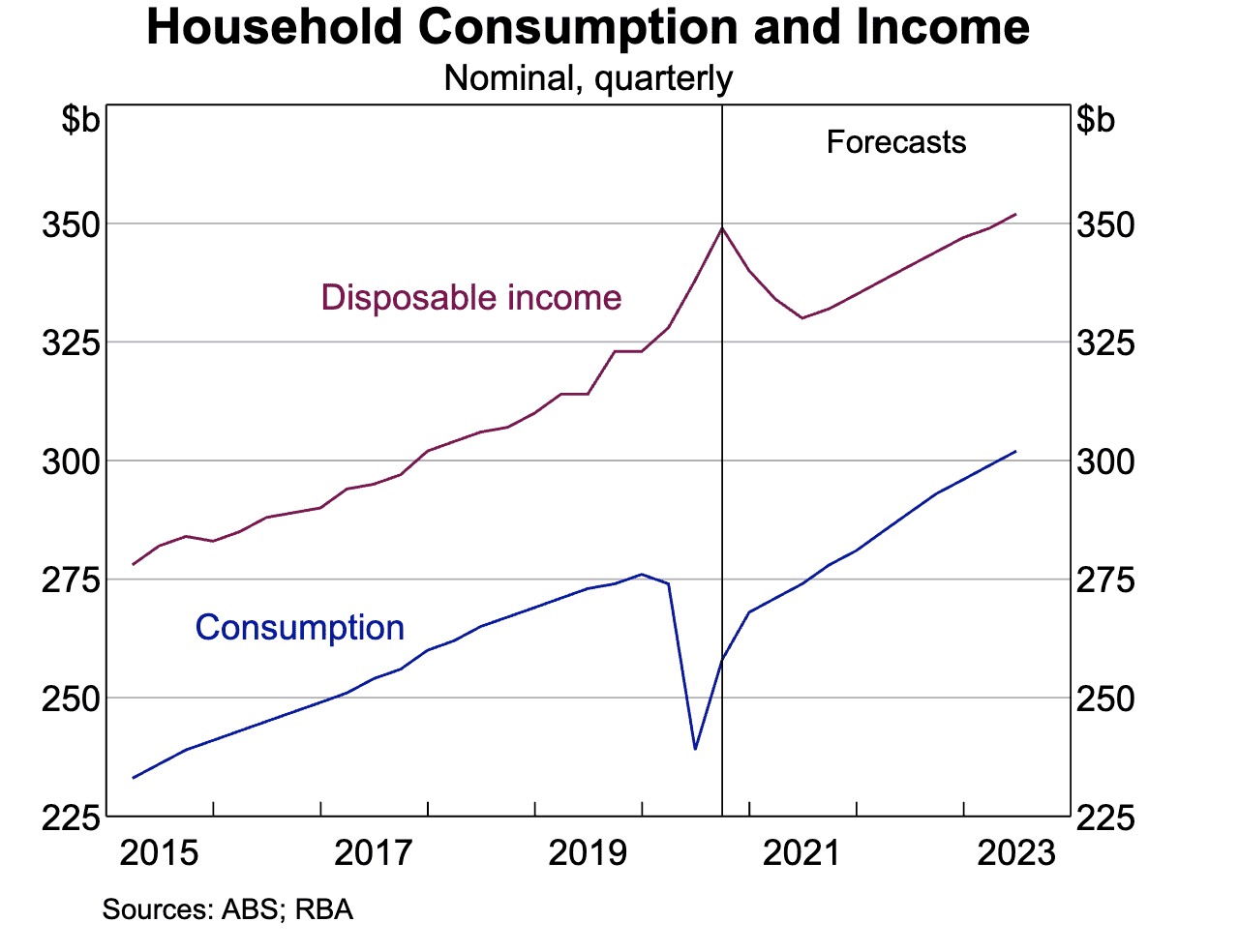

Unusually for an economic downturn, growth in household income has been quite strong, largely reflecting the support provided by fiscal policy.

Much of this extra income has been saved, with the household saving rate surging to 22 per cent in the June quarter.

This largely reflects the limited spending opportunities during the lockdowns, but it is also a response to the uncertainty that people felt about the future.

These extra savings have strengthened household balance sheets and mean that many people now have bigger financial buffers than they had previously.

One other important factor bearing on household spending is the housing market.

When I spoke here last year I discussed how falling housing prices was one of the factors that had contributed to sluggish growth in 2019.

The dynamics in the housing market now look to be in a different phase, with prices rising across most of the country recently.

It remains to be seen how long this will continue, but sustainable increases in asset prices support household balance sheets and encourage spending through positive wealth effects.

Higher housing prices can also encourage additional residential construction.

But as housing prices rise again, we will be monitoring lending standards closely.

We would be concerned if there were to be a deterioration in these standards, but there are few signs of this at the moment.

Source: Address to the National Press Club of Australia by RBA Governor Philip Lowe

Source: Address to the National Press Club of Australia by RBA Governor Philip Lowe