Key takeaways

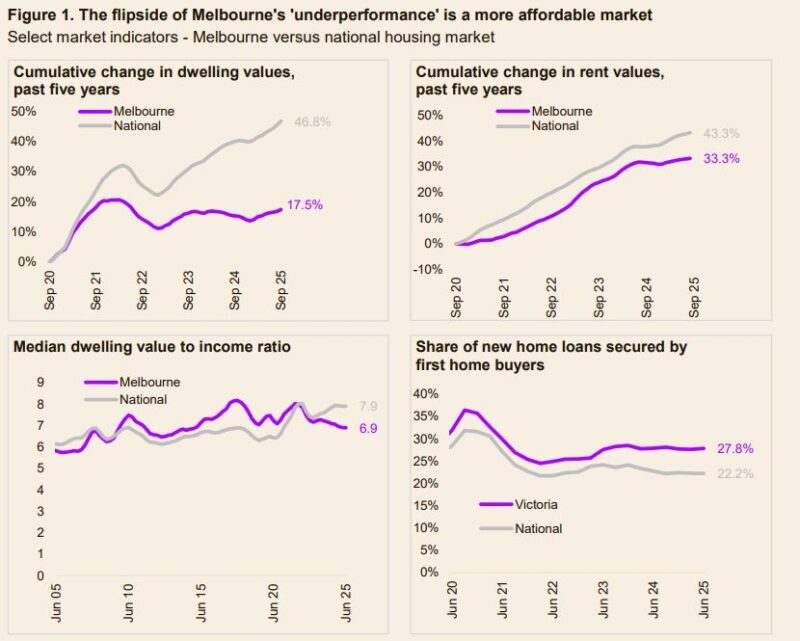

Affordability edge: Melbourne’s home values have risen just 17.5% in five years, well below the national 46.8%, keeping the median house value under the $1 million mark across the city. At $953,000, Melbourne's median house value is lower than Brisbane, Canberra, and far below Sydney.

Softer investor interest in Victoria and Melbourne: Recent tax changes introduced by the Victorian government in the May 2023 Budget may have dampened investor demand across the state, easing competition for homes and potentially creating more opportunities for renters to become first home buyers.

Weaker economy performance: Affordability gains reflect broader challenges, including population loss, low income growth and post-COVID recovery.

Supply warning: Another contribution to slower value increases and price falls may be the fact that Victoria has seen a higher number of dwelling completions than other states and territories. With 885,000 dwellings completed in Victoria over the past 15 years, that's 21.5% higher than the more populous state of NSW. However, lower rates of growth may affect feasibility of new projects.

Nationally, housing affordability has deteriorated badly since the pandemic.

Cotality data shows home values are up 46.8% in the past 5 years.

The median dwelling value has gone from 6.4 times, to almost 8 times median household income.

Median rent across Australia has reached $672 per week, with rent values up 43.8% in the past five years.

The Melbourne property market is a bit different.

Dwelling values across the city are up just 17.5% in the past five years.

At $953,000, the median house value remains under the million-dollar threshold (a milestone surpassed by Canberra and Brisbane this year, while Sydney’s median house value surpassed $1.5 million).

The dwelling value to income ratio in Melbourne is sitting at 6.9, down from a high of 8.2 in 2017 to be at the lowest level since December 2014, and while rents have risen a substantial 33.3% in the past five years, this is still among the lowest result of the capitals and well below the national figure.

This relatively affordable housing is clearly having an impact, with ABS housing finance data showing Victoria also leads on the share of new housing loans to first home buyers.

So what is different about the Melbourne market? And does it pose a lesson, or a warning, for Australia?

A tougher investment environment has likely cooled the market.

Recent tax changes may have dampened investor demand in Victoria, easing competition for homes.

In the May 2023 budget, the Victorian government introduced several investment property tax reforms effective January 2024:

- Lowered the land tax threshold from $300,000 to $50,000;

- Introduced a flat land tax increase of up to $975;

- Raised the absentee owner

For a tenanted property with a land value of $650,000, these changes equate to an estimated $1,300 annual increase in tax.

When combined with rising interest rates, maintenance, and compliance costs, the feasibility of holding investment properties may have declined.

These new or higher taxes come on top of other taxes including higher stamp duty rates relative to most other states, vacant residential land tax and short stay levy to name a few.

While comprehensive data is limited, some indicators suggest investment property ownership has weakened as a result of these properties.

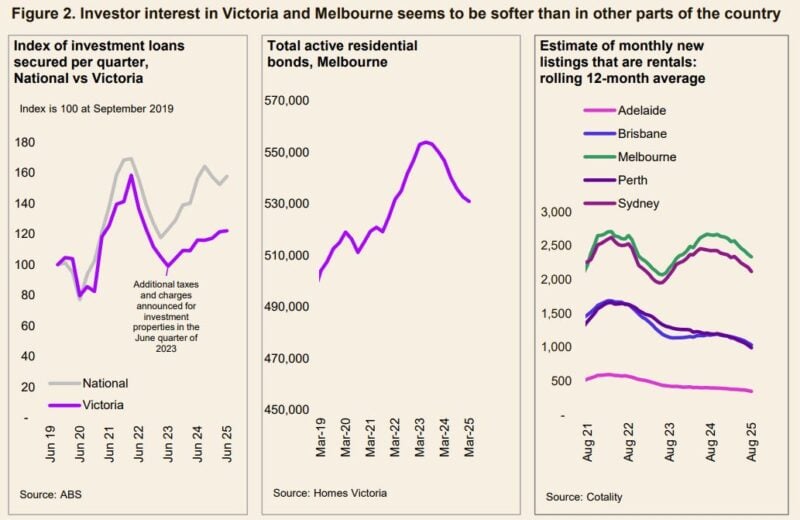

Figure 2 shows that new investment lending in Victoria has been rising since mid-2023, but at a slower pace than the national trend.

Rental bond data implies a contraction in the overall investment stock (though this has also been occurring in other states), and experimental data from Cotality also points to relatively elevated investment listings in the city over time.

If the sale of investment properties and decline in investor interest in the market allows renters to become first home buyers, this would ultimately be a good outcome in terms of home ownership rates, while slowing growth in housing values.

Between March 2023 and March 2025, residential bond numbers declined by around 22,000 across Victoria amid the announcement, and implementation of new investment property taxes.

However, first home buyer loans secured across the state were around 74,000 in the same period.

Updated data on the rate of home ownership, and more comprehensive insights into purchaser type and household composition would help evaluation of the housing outcomes from tax changes.

Figure 2 also shows Victoria was becoming less popular with investors even before the announcements from the 2023 state budget.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:Perth housing market update | March 2026

New investor home loans under-performed the national trend from September 2020, and implied investor listings overtook Sydney in 2021.

Clearly other factors have been at play, disincentivising investment in Victorian housing.

Historically there has been a close correlation between the rate of capital gain and investment activity.

Stronger capital gains outside of Victoria has been another factor in the lower level of Victorian investment.

Weak economic and demographic trends have also kept values

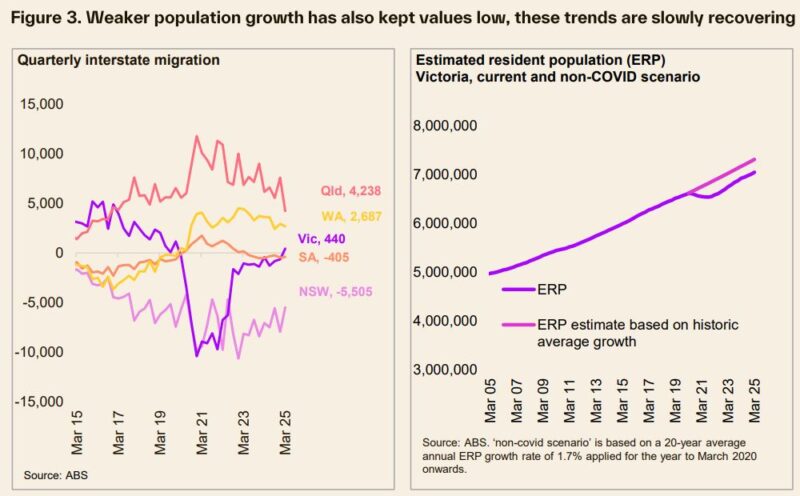

Victoria’s population fell by over 1.1% between March 2020 and September 2021, against a national increase of 0.3%, with a ‘double whammy’ of interstate and overseas migration plummeting.

The Victorian population has not quite caught up to what it would look like if growth had been uninterrupted and ran at the historic 20-year average of 1.7% (figure 3).

The interstate trend is looking more positive, with relative housing affordability potentially attracting more interstate migrants back to Victoria and creating fewer departures.

But this in turn, may be starting to put upwards pressure on home values once again.

Victoria’s economic performance was also challenged by COVID, where Melbourne had seen a world-record 262 days in lockdown.

Economists have also noted long-term structural challenges for the economy, including employment becoming more concentrated in low productivity industries, a relative decline in per capita household income and high government debt relative to gross state product.

While there are definite signs of strength and recovery in the state, weak economic performance is ultimately not how housing affordability should be achieved, because lower home prices are simply symptomatic of less purchasing power.

Victoria has historically seen more homes delivered…

Another contribution to slower value increases and price falls may be the fact that Victoria has seen a higher number of dwelling completions than other states and territories.

ABS data of building activity shows 885,000 dwellings have been completed in Victoria over the past 15 years, 21.5% higher than the more populous state of NSW.

… but the future pipeline of work has been fading

The Melbourne market currently has an ‘affordability advantage’, but like any market, lower prices create an incentive to restrict supply.

Whether it’s a home seller delaying a listing until prices go up, or developers struggling with feasibility.

Total listings in Melbourne are currently 15% lower than a year ago, and new dwelling approvals in Victoria have averaged 4,600 a month through the year to August, 12% below the decade average.

At the national level, the past 12 months have seen dwelling approvals running 5.7% below average.

The reality is that Melbourne offers both lessons and warnings for the broader Australian housing market.

More subdued price growth and reduced investor activity has clearly increased affordability and made room for more first home buyer activity.

But this may also be contributing to a reduction in new housing supply due to reduced feasibility for new construction.

Between tighter supply, rising interstate migration and lower interest rates, Melbourne home values have picked up 3.0% through the year to date (albeit lower than the 4.7% across the combined capitals).

Whether Melbourne can maintain its affordability advantage over the longer term is yet to be seen.