Key takeaways

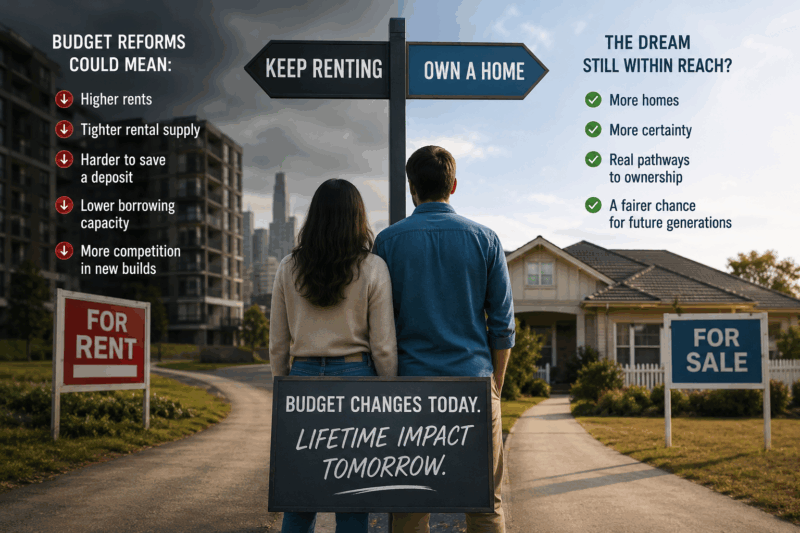

The budget reforms may sound helpful for first-home buyers, but they risk creating unintended consequences.

Many future home owners are renters first, so higher rents could make it harder for them to save a deposit.

If investors pull back from established properties, rental supply could tighten further giving tenants less choice and less bargaining power.

Rentvestors could be hit particularly hard because they often rely on investment property as a stepping stone into future home ownership.

The policy could push more investors into new builds, putting them in direct competition with first-home buyers in affordable new housing markets.

Slower price growth in some established markets may help a limited number of buyers, but the benefits are likely to be uneven.

The reforms do little to address the real issue - Australia’s shortage of well-located, suitable housing.

Changing tax rules may shift demand around, but it does not create more homes.

Future home owners need more supply, more certainty and more practical pathways into ownership, not symbolic attacks on property investors.

For years, young Australians have been told to work hard, save harder, sacrifice more and somehow find a way into a housing market that keeps moving faster than their wages.

And many of them have done exactly that.

They have stayed at home longer with their parents, taken second jobs, delayed having children, invested in shares, bought interstate, rentvested, and looked for creative ways to get a foot on the property ladder.

Now, just as some of them were getting close, the rules are being changed.

The federal budget’s proposed changes to negative gearing and capital gains tax are designed to reduce intergenerational inequality and improve housing affordability.

Under the reforms, investors will no longer be able to use negative gearing benefits on established homes, although those benefits will remain for newly built properties.

The current 50 per cent capital gains tax discount will also be replaced from July next year with an inflation-indexed system, with partial grandfathering for existing investors. (

On the surface, this sounds like a win for first-home buyers.

After all, if fewer investors are competing for established properties, surely that gives aspiring home owners a better chance.

But housing markets are rarely that simple.

In fact, my concern is that these budget changes could end up hurting many of the same people they are meant to help.

The first group likely to be affected will be renters trying to save a deposit

Domain’s chief of Research and Economics. Nicola Powell warns that the “paradox” of these reforms is that renters may face higher rents as investors pull back from established housing, reducing rental supply over time.

That matters because higher rents make it harder to save, meaning it will be harder to borrow and harder to escape the rental treadmill.

This is the part of the housing debate that is often missed.

Most first-home buyers are renters before they become owners.

So even if property price growth slows a little, that benefit can be quickly eaten up if rents rise, living costs remain high and deposits become harder to build.

The budget modelling suggests the tax changes could slow house price growth by about 2 per cent annually while lifting median rents by only $2 a week.

But Powell believes the rental impact could be larger, as does Michael Yardney in his insightful article here pointing to New Zealand’s experience after similar investor tax changes were introduced in 2021 and later reversed.

Of course, not everyone agrees, but even if rents do not suddenly surge, the policy still risks making the rental market tighter at a time when Australia already has a shortage of suitable accommodation.

And when rental markets are tight, tenants have less bargaining power.

They stay longer in properties that no longer suit them. They delay saving. They delay buying.

Some even delay starting families.

That is hardly a recipe for improving home ownership.

Rentvestors

There is another unintended consequence, and it affects rentvestors.

Rentvesting became popular because many young Australians could no longer afford to buy where they wanted to live. So instead, they rented in a location that suited their work and lifestyle, then bought an investment property in a more affordable market.

It was not perfect, but it was a pathway, allowing younger Australians to get into the market, build equity and give themselves a fighting chance of upgrading into a home later.

Dr.Powell believes these reforms could reduce cash flow for rentvestors, tighten borrowing capacity and make property and share investing a less tax-effective way to build a home deposit.

That is important because today many aspiring home owners no longer follow the old path of buying their first home, living in it for years, then upgrading later.

The modern pathway is messier.

Some buy an investment first. Some buy interstate. Some buy with siblings. Some stay at home and invest in ETFs.

Some rent in Melbourne or Sydney while buying an investment in cheaper regional markets.

By making wealth-building harder for younger Australians, the budget may reduce one of the few remaining stepping stones into home ownership.

First home buyers will compete with the investors.

The reforms may also shift more investor demand toward newly built properties because negative gearing benefits will remain available there.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Australian housing market update | July 2026

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

Again, that sounds sensible in theory because Australia needs more housing supply.

But there is a catch….First-home buyers are often active in the same new housing markets, particularly outer suburban house-and-land estates and more affordable new apartments.

This could create a “friction point” where investors and first-home buyers end up competing in the very markets first-home buyers can still afford.

This could push up prices at the affordable end of the new-build market.

In other words, the Budget may reduce investor demand in one part of the market, then increase it in another.

And that other part may be exactly where many first-home buyers are trying to buy.

This is where the debate becomes frustrating

Politicians keep talking as if investor demand is the main reason housing is unaffordable.

But the deeper problem is that Australia has not built enough of the right type of housing in the right locations for a very long time.

We have high population growth, shrinking household sizes, rising construction costs, slow planning systems, infrastructure bottlenecks, high taxes on development and a private rental market that is expected to do much of the heavy lifting.

Changing tax settings may move some demand around, but it does not magically create more well-located homes.

In fact, if the policy reduces investor confidence, it may discourage some of the private capital Australia needs to provide rental accommodation.

And remember, most rental properties in Australia are provided by everyday mum-and-dad investors, not billionaires.

They are teachers, nurses, tradies, small business owners and PAYG taxpayers trying to build some financial independence.

Punishing them may be politically popular, but it does not automatically help the next generation buy a home.

Then there is also a bigger psychological issue.

When governments keep changing the rules, people lose confidence.

Property investment is a long-term game.

People take on large debts, accept short-term cash flow pain and commit to holding assets for decades because they believe the rules will remain reasonably stable.

Once future buyers believe the goalposts can be shifted whenever housing affordability becomes politically uncomfortable, they become more cautious.

That caution can show up in fewer investors, fewer rental properties, tighter vacancy rates and higher rents.

And again, the person who suffers first is often the renter trying to become a home owner.

Some will benefit.

Now, to be fair, there will be some aspiring buyers who benefit.

Some first-home buyers looking for established homes may face less competition from investors.

Some may get into the market a little sooner.

Some established home prices may grow more slowly than they otherwise would have.

But I suspect the gains will be uneven.

A first-time buyer with help from the Bank of Mum and Dad may still buy, as will many dual-income professional couples.

But the renter with limited savings, rising living costs and no family support may find the ladder has been pulled a little further away.

And that is the real risk.

The budget may make it look as if the government is helping future home owners, while quietly making their journey harder through higher rents, reduced borrowing power, fewer wealth-building options and more competition in the new-build markets.

Good housing policy should increase supply, encourage long-term investment, support renters, help genuine first-home buyers and provide confidence for those trying to build their financial future.

These Budget reforms may tick some political boxes, but I am not convinced they solve the problem.

Future home owners do not need more symbolic attacks on investors.

They need more homes, more certainty, more pathways into ownership and a rental market that does not consume their deposit before they can save it.

Until governments deal with the supply side properly, we will keep rearranging the chairs while young Australians are left wondering why the dream keeps moving further away.