Key takeaways

PropTrack reports that flood risk isn’t a future concern; it’s a real, current drag on values.

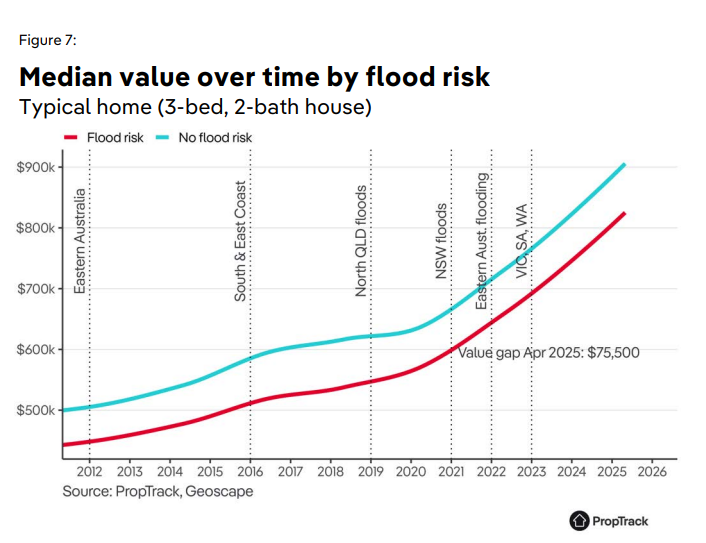

A typical flood-risk home is worth $75,500 less than a comparable flood-free property, and the discount persists for years.

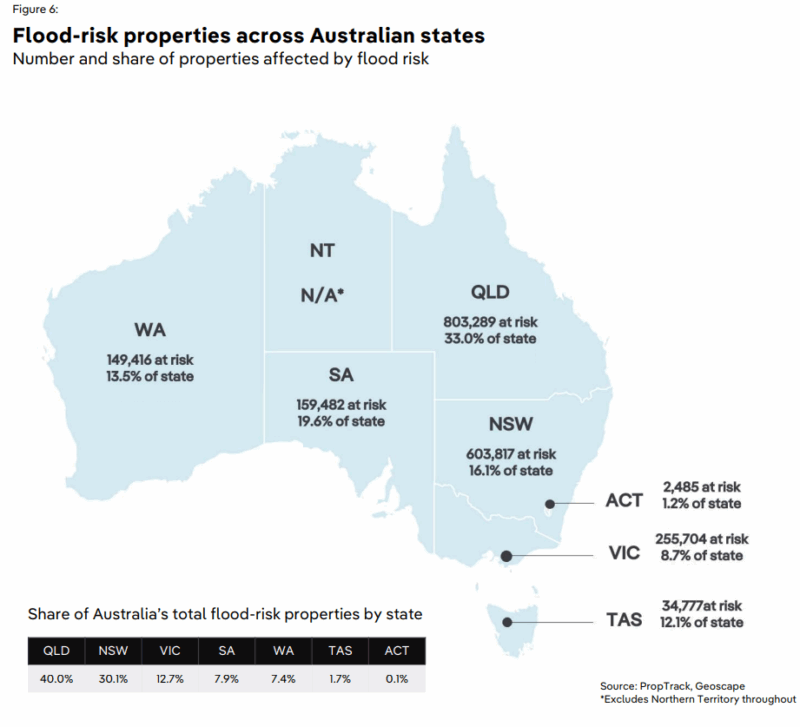

More than two million homes face flood risk, with QLD and NSW the most affected.

These high-demand lifestyle markets are experiencing the strongest repricing as insurance costs rise and extreme weather becomes more frequent.

It’s not just about how many homes in a suburb are flood-prone — it’s about perceived vulnerability.

Areas like Mermaid Beach–Broadbeach see value drops as high as 48%, despite relatively low exposure. Buyer psychology matters.

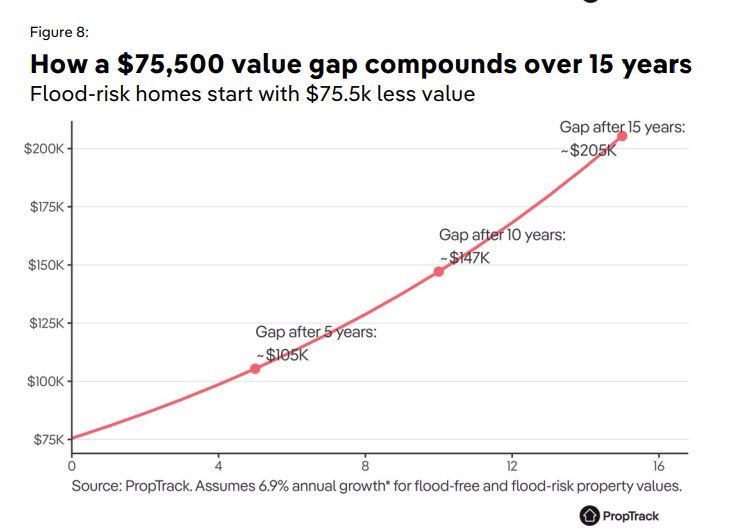

Flood-risk properties don’t just start at a discount; they grow more slowly.

Over 15 years, the long-term growth penalty can amount to hundreds of thousands in lost equity, creating a structural divide between resilient and exposed suburbs.

Flood risk isn't destiny; smart infrastructure can protect both homes and long-term capital growth.

After watching the property market evolve over a number of decades, I’ve learned that the biggest shifts often happen quietly, long before they show up in median price charts or in the headlines.

We talk endlessly about interest rates, supply shortages, migration surges and rental pressures.

But there’s another structural force now shaping values in ways most Australians still aren’t factoring in:

Note: Flood risk has become a live pricing signal—one that’s already wiping billions off property values nationwide.

The new PropTrack Climate Council Property Value Flood Risk Report is the first national analysis showing exactly how this risk is being capitalised into home values right now.

And for serious investors, the implications are profound.

The price of flood risk: $42.2 billion already gone

This isn’t a future projection or climate modelling exercise.

PropTrack’s analysis shows Australian homeowners have already lost $42.2 billion because of flood risk being priced into the market.

That loss shows up as reduced capital growth, lower valuations, and persistent discounts compared to comparable flood-free properties.

Here’s the key figure: A typical flood-risk home is worth $75,500 less than an equivalent flood-free home.

That’s an 8.5% discount in today’s market.

And here’s the part investors often underestimate: Flood-risk homes don’t just start lower, they grow slower over time.

When you compound that over 10–20 years, the wealth gap becomes enormous.

PropTrack demonstrates that underperformance of up to 48 percentage points has occurred over the past 15 years.

For an asset class built on compounding, this is no small thing.

One in six Australian homes faces flood risk, but the exposure isn’t even

More than two million Australian homes, roughly 17% of the national housing stock are exposed to some level of flood risk.

But the distribution is heavily skewed:

-

Queensland: 40% of all flood-risk homes

-

New South Wales: 30%

-

Victoria: 13%

-

Other states combined: 17%

Why does this matter?

Because QLD and NSW are also:

-

home to some of our strongest lifestyle markets

-

the states with the biggest population inflows

-

home to Australia’s most flood-prone catchments

-

the regions most affected by recent extreme weather

This combination of demand + exposure is already shifting market behaviour.

The market punishes perceived vulnerability more than actual exposure

One of the most interesting findings from PropTrack is that the size of the value discount doesn’t necessarily match the level of flood exposure.

Some suburbs with relatively small proportions of flood-prone properties suffer huge value penalties, while others with high exposure see little to no discount.

Consider these examples:

Mermaid Beach–Broadbeach, QLD

-

Only 16% of homes are flood-prone

-

But flood-risk homes are discounted by 48%

Palm Beach, QLD

-

Nearly 80% of homes are exposed

-

Value reduction: 26%

Why the mismatch?

Because recent disasters, insurance challenges and the visibility of risk matter more than raw flood ratios.

Perceived vulnerability drives price outcomes. Not just exposure.

This is one of the most important insights for investors.

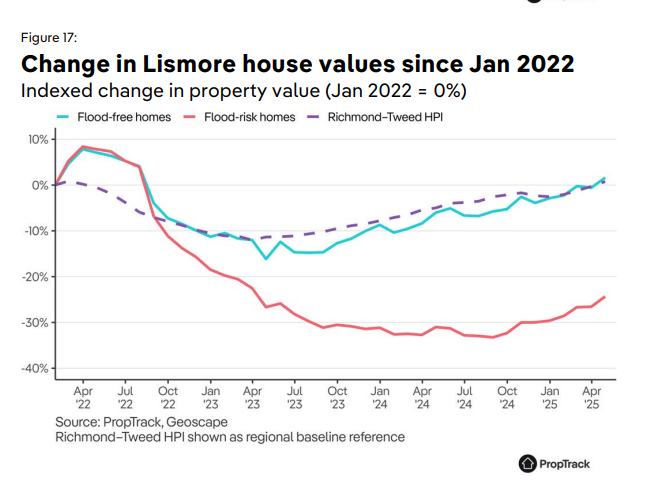

Lismore: a case study in permanent repricing

Lismore stands out as the most dramatic example of how a major flood can permanently reshape a market.

Before the 2022 floods:

-

Flood-risk homes were valued 17% lower than safer homes.

After the floods:

-

That discount widened to 38%.

-

Flood-risk homes have not recovered to their previous price peaks.

-

Buyer behaviour shifted sharply toward safer, elevated, and less exposed properties.

The report also shows that homes in the broader Northern Rivers region that weren’t in immediate flood zones still faced spillover effects: slower recovery, more discounting, and softer demand.

This is what structural repricing looks like.

- Also read:RBA raises interest rates again. Here’s what this means for property. | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:National Weekly Auction Report – March 21st 2026 | Auction Markets Down Again Following Latest RBA Rate Increase

- Also read:Perth housing market update | March 2026

The message for investors is clear:

Note: Markets don’t “bounce back” from every disaster, sometimes they fundamentally reset.

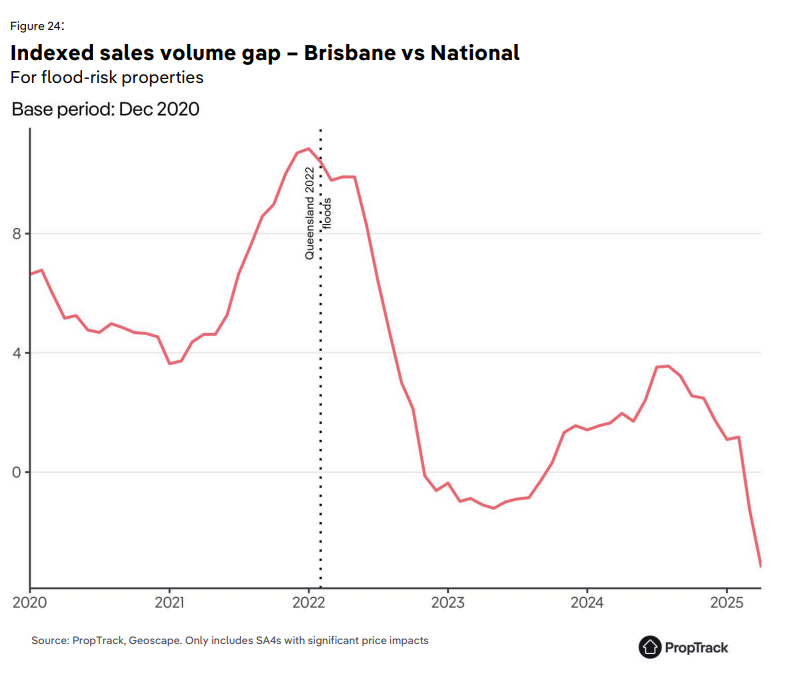

Brisbane: a city that loves the water but the market is starting to notice the risk

Brisbane is a fascinating market because it’s highly exposed, yet still heavily priced according to lifestyle factors like river frontage, breezes, and amenity.

Some Brisbane SA4 regions have flood exposure rates of:

-

53%

-

50%

-

41%

In other words, in some pockets, one in every two homes is flood-risk.

For years, many buyers barely blinked. Waterfront homes still attracted premiums.

But after the 2022 floods, this changed quickly:

-

Flood-risk property prices softened

-

In several suburbs, flood-risk homes that previously enjoyed a premium flipped to a discount

-

Sales volumes for flood-risk homes fell more sharply than the national trend

The city is finally pricing in risk, slowly, unevenly, but unmistakably.

The long-term growth penalty: the biggest risk for investors

Here’s what should concern investors the most:

Note: Flood-risk isn’t just a one-off discount — it’s a long-term growth drag.

PropTrack’s modelling shows flood-risk homes have underperformed flood-free homes by up to 48 percentage points since 2010.

Consider this in practical terms: If a $1 million flood-free home compounds at a typical rate over 15 years, it might grow to $2.5 million.

A flood-risk home growing 48 percentage points less might end up closer to $1.6 million. That’s an $890,000 difference in equity, purely due to risk exposure.

This is the type of compounding divergence that defines who wins and who falls behind in property.

Not all flood-exposed markets are losers: resilience changes everything

PropTrack’s analysis also highlights something very important:

Note: Suburbs with strong flood mitigation infrastructure often show no value penalty at all.

The best example is Grafton, NSW, where:

-

61% of homes are technically flood-prone

-

Yet flood-risk homes have historically been valued higher than flood-free homes

-

Long-standing levees and upgrades have repeatedly prevented widespread flood damage

-

Benefit-to-cost ratios for mitigation investments exceed 2:1

This is the resilience dividend: A flood-exposed suburb with high-quality infrastructure can outperform flood-safe suburbs with no mitigation.

For investors, this means:

Risk is not just about hazard. It’s about preparedness.

What smart investors should do now

1. Integrate flood mapping into every purchase decision: Cross-check multiple sources — not just the council’s flood overlay.

2. Prioritise elevated land and natural topography: Elevation is becoming a new form of scarcity.

3. Scrutinise insurance availability and premiums: Insurance has become a powerful driver of long-term capital growth.

4. Watch for government-funded resilience upgrades: These areas may see a future uplift as risk reduces.

5. Adjust long-term growth assumptions for exposed suburbs: Underestimating the compounding penalty is the biggest financial risk.

6. Don’t overreact, but don’t ignore the structural shift: Markets evolve gradually until they move suddenly. This is one of those shifts.

Final thoughts

The PropTrack findings confirm what many experienced investors have sensed: We’re entering a new era where climate resilience influences long-term value just as much as location.

Flood-safe homes are already:

-

selling faster

-

discounting less

-

enjoying stronger long-term capital growth

-

compounding wealth more reliably

Flood-risk homes, on the other hand, face:

-

bigger discounts

-

slower recovery

-

higher insurance costs

-

and long-term underperformance

Not everywhere. Beyond major levees and government works, effective local stormwater management also plays a role in reducing flood impact. Well-maintained pits, drains, and runoff systems can materially limit surface water build-up during heavy rainfall, particularly in urban catchments.

Not immediately. But consistently enough that investors ignore it at their peril.

The goal is not to avoid flood-risk markets altogether, it’s to understand how the next decade of capital growth will increasingly favour resilient locations over exposed ones.

As always, knowledge and foresight compound just like capital.