Key takeaways

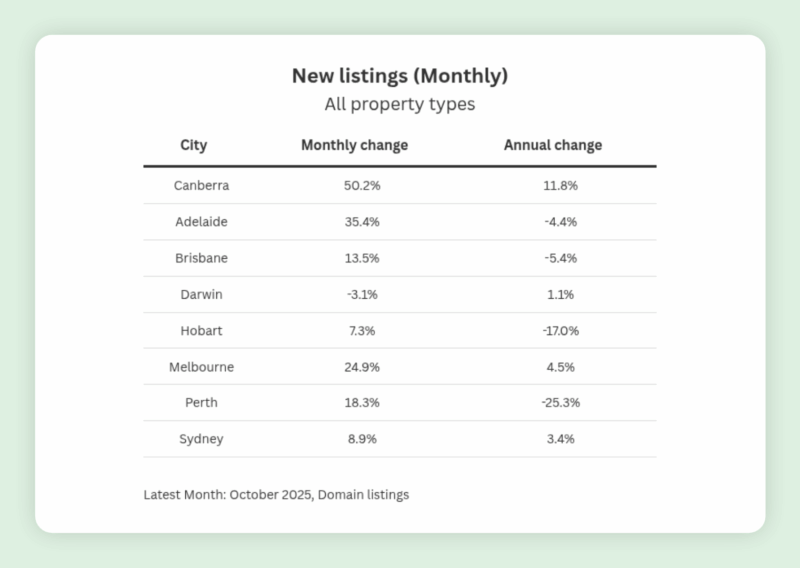

October saw the highest level of new listings in a year, with Sydney and Melbourne leading the surge.

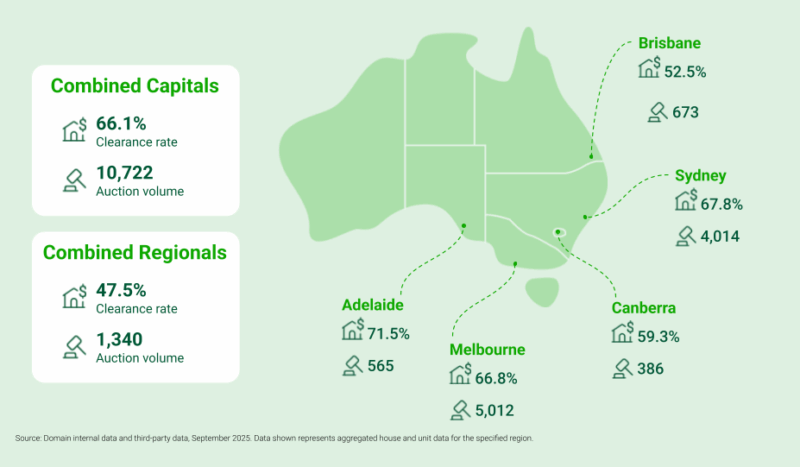

Strong auction volumes and steady clearance rates signal a market that’s regaining momentum heading into year-end.

Clearance rates held at a solid 66.1% even as listings jumped. This shows buyer demand remains resilient, though growing stock levels may gradually shift conditions toward buyers in early 2025.

Most capitals are still grappling with record-low vacancy rates, Hobart at 0.2%, Adelaide and Perth at 0.5%, and Sydney at 0.8%. This continues to underpin rental growth and add pressure to already-tight rental markets.

Across Sydney, Melbourne, Brisbane, Adelaide, and Darwin, distressed listings are at their lowest point in two to three years. This reflects strong household balance sheets and reduced forced selling.

Adelaide and Darwin are selling faster, while Sydney, Melbourne, Brisbane, and Perth are taking longer compared to last year.

Canberra is seeing the biggest slowdown, with days on market at a two-year high due to record supply.

Every so often, we see a shift in the housing market that feels less like a data point and more like a turning tide.

October was one of those months.

Across the country, sellers stepped forward in numbers we haven’t seen in many months, buyers kept competing despite higher volumes, and auction rooms buzzed with energy that’s been missing for a while.

According to Domain’s latest October Market Insights, Australia’s major capitals are showing signs of growing confidence — the kind of confidence that typically marks the early stage of the next upswing.

Renewed energy: more listings and still-strong clearance rates

Domain’s Senior Economist, Dr. Joel Bowman, summed up October beautifully: strong clearance rates, the highest level of new listings in a year, and clear evidence of renewed seller confidence.

Buyers, of course, are still dealing with the usual pressures: tight supply, evolving policy changes, and ongoing competition, but the landscape is subtly shifting.

As more properties come onto the market, we’ll gradually see conditions tilt toward buyers in some segments.

But for now? It’s still an active, fast-moving environment.

Auction clearance rates slipped slightly to 66.1%, but in context, that’s still very solid, especially considering auction volumes across the capitals hit a seven-month high.

More stock typically puts downward pressure on clearance rates, so holding at mid-60s tells you demand is still alive and well.

Capital city snapshots

According to Domain’s latest October Market Insights...

Sydney

Sydney led the charge in October with new listings hitting a record high.

This is exactly what you’d expect when confidence returns: sellers feel the wind at their backs.

A few notable points:

-

Prices remain strong.

-

Distressed listings have fallen to their lowest levels since late 2021.

-

Vacancy rates dropped back to a tight 0.8%.

Put simply, Sydney is still undersupplied, and even rising listings aren’t enough to cool things down meaningfully yet.

Melbourne

Melbourne’s new listings surged to their highest October level on record, a remarkable shift for a market that’s been lagging behind Sydney in recent years.

Vacancy rates held steady at 1.3%, and distressed listings are at their lowest since 2021.

The real indicator of improving seller leverage? House discounting is now at its lowest in over a year.

Sellers are starting to call the shots again.

Brisbane

Brisbane saw new supply rise to a one-year high, but overall levels are still below last year’s.

Clearance rates softened slightly but remain higher than in 2023 and the market’s underlying strength is clear when you look at distressed listings, which hit their lowest since January 2022.

Vacancy rates remain a major storyline too, holding at a lean 0.7%.

Adelaide

Adelaide continues to surprise on the upside.

New listings reached a one-year high, giving buyers a little more choice without easing competition much.

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

Clearance rates dipped, but they were still the second strongest we’ve seen since late 2023.

Vacancy rates held at 0.5%, showing the rental market remains exceptionally tight.

Canberra

Canberra is one of the few capitals where new and total supply hit record highs, a significant development.

More choice is great for buyers, but it’s clearly putting pressure on sellers.

Discounting reached its highest October level since 2016, and days on market rose to the highest point in nearly two years.

Still, vacancy rates dropped sharply to 1%, reflecting underlying stability.

Perth

Perth continued its streak of tight supply.

New listings rose for the second straight month to a seven-month high, but stock levels are still the lowest on record for this time of year.

Homes are taking a bit longer to sell, a natural cooling after the extraordinary speed of recent years.

Meanwhile, vacancy rates of 0.5% show the rental crisis is far from over.

Hobart

Hobart’s new listings also climbed to a seven-month high, but remain below last year’s levels.

The standout figures:

-

House discounting at its lowest since mid-2022

-

Vacancy rates at just 0.2% — the tightest in the country

Darwin

Darwin’s new listings fell monthly but remain up annually.

Distressed listings dropped back to record lows, supporting a steady, stable environment.

Vacancy rates remained tight at 0.4%, continuing Darwin’s recent trend of improving fundamentals.

Days on market: a split between fast movers and sluggish sales

Across the capitals, selling times painted two very different pictures in October:

-

Adelaide recorded its fastest selling pace of the year.

-

Darwin also saw days on market shrink.

-

But in Sydney, Melbourne, Brisbane, and Perth, selling times lengthened compared to last October, a sign that supply is finally starting to catch up with demand.

-

Canberra reached its highest days on market in almost two years, reflecting the pressure of record-high supply.

This divergence highlights a maturing cycle: markets that have been running hot are normalising, while others with stronger fundamentals continue to power ahead.

Final thoughts

What this data tells us is simple: confidence is returning.

More sellers are listing, buyers are still showing up, and the fundamentals remain strong across most capitals.

While higher supply over the next few months might cool certain segments, the bigger trend remains in place: Australia’s property markets are healing, normalising, and slowly shifting toward the next phase of the cycle.

For strategic investors who understand the long-term nature of property, this is the kind of market where opportunities quietly emerge.