Key takeaways

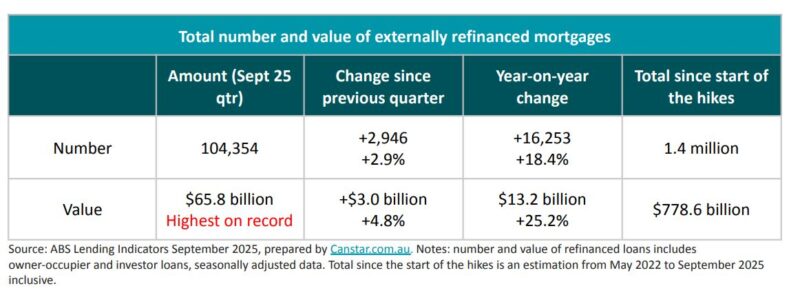

A record $65.8 billion in loans were refinanced in the September 2025 quarter, almost $500,000 every minute.

Borrowers are responding to recent RBA rate cuts and proactively lowering their mortgage costs, often saving over $12,000 in two years by switching to more competitive rates.

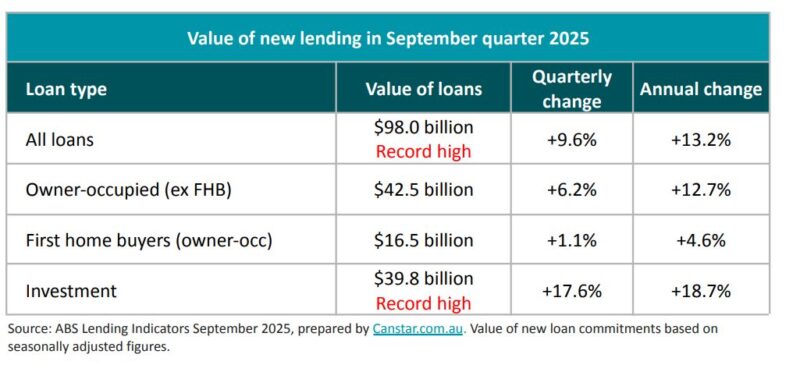

Total new housing loans hit a record $98 billion for the quarter, with investors leading the rebound (+17.6%).

This signals renewed confidence, rising borrowing capacity, and early positioning for the next stage of the property cycle.

The average new owner-occupier loan has climbed to $694,000, with several states reaching fresh records.

Larger loan sizes are a classic early-cycle indicator that buyers are stretching further, and price growth is likely to follow.

Every now and then, a statistic comes along that perfectly captures where we are in the property cycle, and where we’re heading next.

The latest analysis from Canstar, based on newly released ABS Lending Indicators, delivered one of those moments:

Almost half a million dollars’ worth of home loans are now being refinanced every single minute in Australia.

That’s not a typo, it’s a sign of the depth of the property market.

Let’s dig deeper into what this means for homeowners, investors, and the future direction of our property markets.

The Refinancing Boom: Australians are fighting back

Canstar’s breakdown of the ABS data shows a record $65.8 billion in mortgages were refinanced in the September 2025 quarter, the highest on record and up $3 billion from the previous quarter.

Why the rush?

The RBA’s cash rate cuts in February, May, and August have triggered a wave of borrowers reassessing their loans, recalibrating their household budgets, and searching for better deals.

After years of rising rates, Australians are taking back control.

Since rate hikes began in May 2022, an estimated 1.4 million mortgages have been refinanced, some more than once.

Note: All the loans being refinanced tells us loyalty to lenders is gone; value is what matters now.

What are borrowers saving? A lot more than you’d think

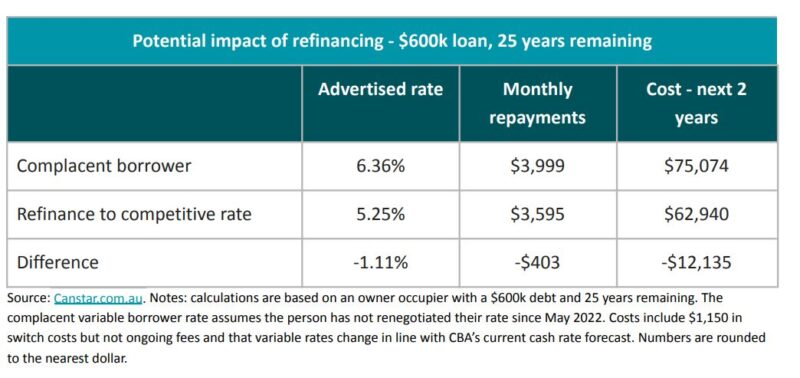

According to Canstar, owner-occupiers who haven’t touched their mortgage in the last few years are typically sitting on a variable rate of around 6.36%.

But competitive lenders are offering 5.25% or lower, and that gap is where the opportunity lies.

For a household with a $600,000 loan:

-

Their monthly repayment could drop by about $403

-

Their two-year savings could exceed $12,000 even after factoring switching costs

In today’s cost-of-living environment, an extra $400 back in the household budget isn’t just helpful, it can be transformative.

Refinancing has effectively become a modern “pay rise” for families who take the initiative.

New lending is surging too

Refinancing isn’t the only part of the market heating up.

The value of new housing loans climbed to $98 billion in the September quarter, a record high.

Investors led the way with a 17.6% jump in new borrowing, followed by upgraders (+6.2%) and first-home buyers (+1.1%).

This rise suggests:

-

Borrowers are feeling more positive

-

Investors are positioning early

-

Rate cuts are flowing through to sentiment and borrowing power

It’s the classic pattern you see when the market transitions from a flat period into its next growth phase.

Canstar’s analysis also highlights that the average new owner-occupier loan has reached a record $694,000, up $16,000 in just one quarter.

- Also read:National Vacancy Rate Falls to 1.1% | SQM Research

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Something strange is happening in Australia’s housing market right now | Property Insiders

- Also read:National Weekly Auction Report – March 7th 2026 | Auction Clearance Rates Ease as Listings Fall Over Holiday Weekend

- Also read:Latest Property Asking Prices State by State | National Listings Rebound Strongly in February as New Supply Surges

Across the states, borrowing capacity is stretching:

-

NSW: $828,000 (record high)

-

VIC: $647,000 (record high)

-

QLD: $687,000 (record high, fastest growth at 4%)

-

SA & WA: also at record highs

This is the predictable result of falling interest rates:

- buyers can borrow more

- competition increases

- prices rise

- loan sizes follow

But it’s also a timely reminder: borrowers should still stress-test their numbers.

Even if rate hikes seem unlikely today, a 30-year mortgage is a long time, and prudent planning matters.

What it all means for property investors

For seasoned investors, three trends stand out:

1. Refinancing reduces market vulnerability

When hundreds of thousands of borrowers shift from high rates to lower ones, it eases financial pressure and reduces forced sales, supporting price stability.

2. Investor borrowing is a forward indicator

A 17.6% jump in investor lending is not random.

Historically, investors move early, well before the broader public realises a new cycle has started.

3. Record loan sizes point to future price growth

Borrowing capacity drives prices. When loan sizes rise sharply, values typically follow, usually with a 6–12 month lag.

All three trends suggest 2026 is positioning itself as a strengthening year for well-located, investment-grade properties.

Final thoughts

The Canstar figures paint a clear picture: Australians are more proactive, more financially aware, and increasingly willing to move lenders if it means improving their financial position.

And the fact that new lending and loan sizes are climbing at the same time tells us buyers are gearing up for the next phase of the property cycle.

This is exactly what we expect in the early stages of a recovery:

-

interest rates come down

-

confidence returns

-

investors strike early

-

buyers stretch further

-

prices follow

For investors, the message is straightforward: Prepare now, act strategically, and focus on quality assets in proven locations.

The next upswing is already forming beneath the surface.