Key takeaways

97% of experts expect the RBA to hold the cash rate at 4.35% in June.

More than half of panellists expect at least one more hike this year.

61% would advise a new borrower to choose a variable rate over fixed.

The RBA will finally give mortgage holders a breather this Tuesday, according to the majority of experts in this month’s Finder RBA Cash Rate Survey, in which 38 experts and economists weighed in on future cash rate moves and other issues relating to the state of the economy.

Almost all panellists (97%, 37/38) expect the RBA to hold the cash rate on Tuesday, keeping it at 4.35%.

Tomasz Wozniak from the University of Melbourne is the only panellist confident the RBA will choose to hike the rate in June.

However most panellists say the pause may be temporary – 55% (21/38) expect at least one more hike before the end of 2026. Of those, 62% (13/21) see it coming as soon as August.

Richard Whitten, home loans expert at Finder, said a cash rate hold would be welcome news for exhausted homeowners.

“After three hikes in a row, a pause will feel like a win for borrowers who've watched their repayments climb all year.

"But the cash rate is still at its highest level in years, and more than half of our experts think there's another hike still to come,” Whitten said.

Michael Yardney, founder of Metropole Property Strategists is expecting a hold.:

"With unemployment edging higher, inflation continuing to ease, and global trade tensions keeping business confidence fragile, the case for another rate rise has essentially disappeared.

The RBA will almost certainly hold in June, because the combination of a softening labour market, cooling property prices, and ongoing geopolitical uncertainty means the board has every reason to stay patient.”

Brodie Haupt from WLTH agreed, but pointed to potential further hikes this year.

“After three rate hikes within the first half of the year, the RBA board could keep the cash rate on hold in June as evidence of an economic slowdown and a cooling job market begins to show.

“However, the worst may not be over for homeowners as global political tensions could mean uncertainty later in the year,” Haupt said.

Almost 2 in 5 experts (37%, 11/30) who weighed in* tip the cash rate to finish 2026 at 4.60%. 1 in 3 (30%) expect it to hold at 4.35%.

Aussie homeowners feeling the pinch

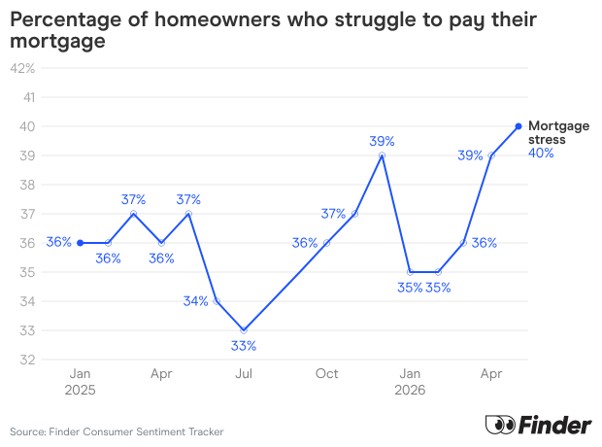

Finder reports that a significant 40% of homeowners said they struggled to pay their mortgage in May, according to data from Finder’s Consumer Sentiment Tracker. That’s up from 35% in January this year.

Richard Whitten said if you haven't reviewed your home loan since the start of the year, you're almost certainly paying too much.

“Now is the time to ask your lender for a better rate – or refinance," Whitten said.

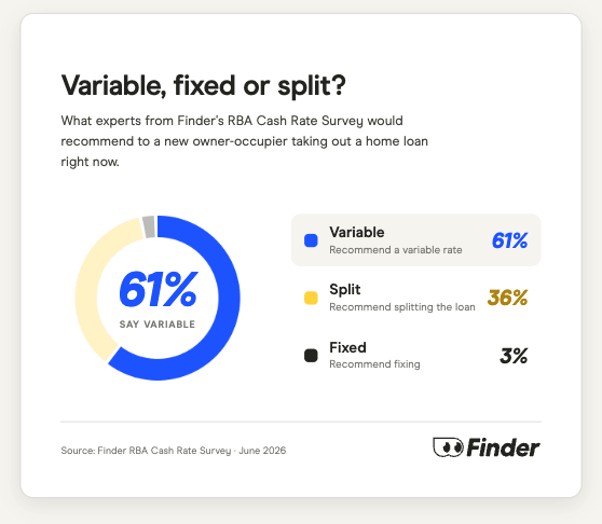

Variable, fixed or split? Experts weigh in

Experts were asked whether they’d recommend a variable, fixed, or split home loan for a new owner-occupier.

More than half (61%, 17/28) of panellists said variable, while 1 in 3 (36%, 10/28) said split.

Just one economist, Jakob Madsen from the University of Western Australia, recommended fixing.

Nicholas Gruen from Lateral Economics said he’d seen variable loans turn out to be cheaper in nearly 80% of cases.

“In other words there's usually a hefty liquidity premium built into the fixed rate," Gruen said.

Graham Cooke from Aussie Insights said he’d recommend splitting.

He said:

“The direction of the next cash rate move remains uncertain, with the decision heavily dependent on inflation metrics tied to the ongoing conflict in the Middle East.

In such an unpredictable economic environment, hedging your bets may be the most prudent strategy."

Here's what a few more experts had to say to the question: If you were advising a family member who'd just purchased an owner-occupier property with a plan to pay it off in 30 years, would you encourage them to go with a variable, fixed or split?

Jakob Madsen, University of Western Australia (Fixed): "It gives more security and a fixed rate loan is convertible, which gives the option to convert to a lower rate loan if interest rates decline. More importantly, world interest rates will not go down because of the aging society."

- Also read:This week’s Australian Property Market Update – Latest Data, State by State June 16th 2026

- Also read:Australian housing market update | June 2026

- Also read:National Vacancy Rate Holds at 1.2%| SQM Research

- Also read:National Weekly Auction Report – June 13th 2026 | Auction Clearance Rates Modest but Reasonably Steady Despite Listings Surge

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

Kyle Rodda, Capital.com (Variable): "Because you're effectively trading against the swaps market. Like any trade, it's only worth taking if you have an edge. Most people don't have the time or ability to outperform the market."

Stella Huangfu, University of Sydney (Variable): "I would recommend a variable rate… the scope for substantial further rate increases is limited. A variable loan also provides greater flexibility and allows borrowers to benefit if interest rates eventually decline."

Mark O'Flynn, Oxlade Financial (Variable): "You can only fix interest rates in Australia for up to 5 years… Fixed rates are already above the variable rate and I don't expect short-term rates to move higher from here."

Matt Turner, GSC Finance (Variable): "Fixed rates are now too elevated to make economic sense compared to where economists are predicting rates to land at the end of the cycle… now some lenders are pushing upwards of 6.75% – it doesn't make sense when the variable rates are still under 6.25%."

Dale Gillham, Wealth Within Group (Split): "With all the economic uncertainty, fixing a part of a loan gives more certainty, whilst allowing for benefits should rates fall. We also need to consider that stock markets will crash this decade."

Shane Oliver, AMP (Split): "The cash rate is getting closer to its cyclical peak (which would argue to be more variable) but will likely still go a bit higher with risk on the upside (which would argue maybe have some fixed)… so it would make sense to have a mix."

Adj Prof Noel Whittaker, QUT (Split): "This is one of those questions which depend entirely on the situation of the couple – including the reliability of their income and how long they intend to keep the house before they sell it."

Here’s what some of the experts had to say about the cash rate:

Tomasz Wozniak, University of Melbourne (Increase): “I believe we’re all set on the RISE! My forecasting system predicts this decision with a record-high 88 per cent probability, reflecting market expectations in light of the latest developments. All models indicate this decision, with the bond-yield curve models suggesting a more hawkish approach, and univariate models of the cash rate target setting on a moderate increase. If this prediction materialises, this would be the highest level of interest rates since October 2011. And there is one person to blame for this state of affairs."

Madeline Dunk, ANZ (Hold): "We think the RBA will keep rates on hold in June. While an August rate hike is a risk, we think the activity side of the economy is slowing and will justify the RBA keeping rates at 4.35%."

Brodie Haupt, WLTH (Hold): "After three rate hikes within the first half of the year, the RBA board could keep the cash rate on hold in June as evidence of an economic slowdown and a cooling job market begins to show. However, the worst may not be over for homeowners as global political tensions could mean uncertainty later in the year."

Matthew Greenwood-Nimmo, University of Melbourne (Hold): "I think the RBA is likely to hold the cash rate constant at the June meeting. This will provide an opportunity to assess the degree to which the economy is softening in the wake of recent rate hikes and global events."

Anthony Waldron, Mortgage Choice (Hold): "It takes time for interest rate changes to be fully understood. I expect the Reserve Bank will keep the cash rate on hold this month, giving the Board time to assess the impact of the three consecutive hikes already delivered this year."

Kyle Rodda, Capital.com (Hold): "Signs of softening growth and a weakening labour market is likely to see the RBA take a 'wait and see' approach to policy as the impact of previous hikes work through the economy."

Dr Andrew Wilson, My Housing Market (Hold): "Although inflation continues to rise above the RBA target range, rising jobless and falling economic growth are now pushing against further rate rises in the shorter term with the Bank likely to now take a wait and see approach on monetary policy as indicated in previous meeting commentary."

Tim Nelson, Griffith University (Hold): "Unemployment has increased – after a series of increases in the cash rate, it would be prudent to hold. Inflation driven by supply shocks beyond Australia's control requires a different policy solution than monetary policy."

Peter Boehm, Pathfinder Consulting (Hold): "Based on current inflation figures the expected reaction from the RBA would be to increase rates. But I don't think this will happen because the highly unpopular recent Federal Budget is contractionary. This coupled with increasing unemployment and general economic malaise will likely see the RBA hold rates for now."

Evgenia Dechter, UNSW (Hold): "Inflation is still above target, but the economy is also showing signs of slowing, with weak GDP growth and rising unemployment rate. Given the three recent cash rate hikes, the RBA may prefer a wait and see approach at the upcoming meeting."

Graham Cooke, Aussie Insights (Hold): "The RBA will likely keep the cash rate on hold in June, allowing the impact of its three recent rate hikes to fully flow through the economy. The Board is likely to maintain its current policy stance and monitor upcoming inflation data before making any further decisions."

Stephen Koukoulas, Market Economics (Hold): "Policy is already tight."

Shane Oliver, AMP (Hold): "The three RBA rate hikes this year have given the RBA some breathing space to wait and gauge the initial impact of the hikes and how the oil supply shock impacts. Recently softer data for consumer spending, jobs and house prices along with mixed inflation data for April add to the case for a pause on rate hikes at the June meeting."

Cameron Kusher, Kusher Consulting (Hold): "After 3 hikes in 3 meetings this year I believe the RBA has now bought themselves some time to see how the economy and inflationary pressures proceed from here."

Leanne Pilkington, Laing+Simmons (Hold): "The recent rises are beginning to bite and at the individual household level, the rising cost of living is a major concern. We may not be at the end of the rise cycle but a reprieve is needed now, which will ideally remain for the rest of the year."

Mathew Tiller, LJ Hooker Group (Hold): "I expect the RBA to hold. Inflation is still too high, but the economy is losing momentum, the labour market is starting to soften and households have pulled back spending. That mix should keep the RBA on pause… For the property market, momentum has cooled. Higher rates are still capping borrowing capacity, and investors are more cautious as the Budget changes get digested. Price growth is moderating."

Nicholas Gruen, Lateral Economics (Hold): "Their previous rise signalled their preparedness to act. But, against the momentum and AI investment tailwinds, there are gathering headwinds making it wise to pause."

Adj Prof Noel Whittaker, QUT (Hold): "I think it's a line ball call. But there is certainly a growing sense of pessimism in Australia. With the reduced activity in the property sector, I think the wealth effect will start to be a factor here. That simply means that when the shares or property drop, people feel poorer and they spend less. Furthermore, the war in Iran is still at a stalemate… I don't think a rate rise is necessary at the moment to subdue demand."

Saul Eslake, Corinna Economic Advisory (Hold): "Monetary policy is now clearly in 'restrictive' territory; headline inflation was a bit lower than expected in April, and the labour market softened a bit more than expected. None of that rules out further rate increases at some point, but it does reduce the need for a 4th consecutive rise. They can now 'wait and see' what the data brings."

Cameron Murray, Fresh Economic Thinking (Hold): "I expect they will pause to see if previous rises have dampened activity and inflation."

Matt Turner, GSC Finance (Hold): "Inflation is still elevated but not accelerating at the rate expected. The increase in the unemployment rate also suggests less need to raise rates this month."

Tim Reardon, HIA (Hold): "After three rate increases, they will pause for more data and clarity around the impact of global factors."